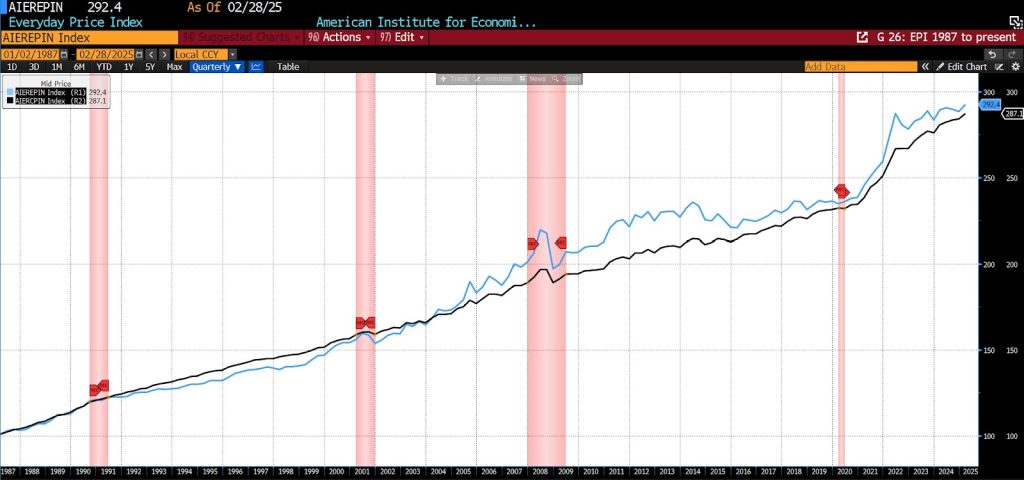

AIER’s proprietary Everyday Price Index (EPI) gained moderately in February 2025, continuing a climb that began in November 2024. The index rose by 0.51 percent to 292.4, its highest level on record.

AIER Everyday Price Index vs. US Consumer Price Index (NSA, 1987 = 100)

Amid the EPI’s twenty-four constituents, 17 rose, two were unchanged, and five declined on a month-over-month basis. Purchase and rental of video, residential telephone services, and cable satellite prices saw the largest gains in price. The largest declines came in postage and delivery services, intracity transportation, and housekeeping supply.

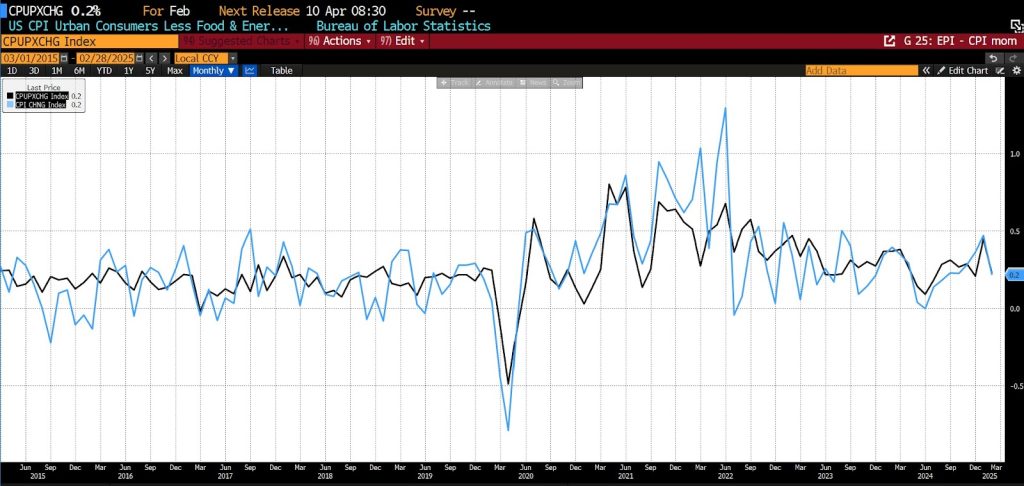

Also on March 12, 2025, the US Bureau of Labor Statistics (BLS) released its February 2025 Consumer Price Index (CPI) data. The month-to-month headline CPI number rose by 0.2 percent, slightly less than the 0.3 increase surveyed. The core month-to-month CPI number saw the same change: up 0.2 percent, higher than the predicted 0.3 percent increase.

In February, the shelter index increased by 0.3 percent, which represented nearly half of the overall rise in the all-items index but was offset by airline fares (down 4.0 percent) and gasoline prices (down 1.0 percent). Despite lower gasoline costs, the broader energy index edged up 0.2 percent owing to increases in electricity (1.0 percent) and natural gas (2.5 percent). Food prices rose 0.2 percent, driven up by an 0.4-percent increase in the cost of dining out, while grocery prices remained flat as declines across most categories were negated by gains in others.

Of particular note, egg prices surged 10.4 percent, pushing the meats, poultry, fish, and eggs index up 1.6 percent, while beef prices surged 2.4 percent. Cereal and bakery product prices rebounded after a January decline, rising 0.4 percent. Restaurant prices continued to trend higher with full-service and limited-service meal costs both up 0.4 percent and 0.3 percent, respectively.

Excluding food and energy, core inflation rose 0.2 percent in February, half of the 0.4 percent increase in January. Shelter costs continued their steady climb, with both rent and owners’ equivalent rent rising 0.3 percent; prices of lodging away from home increased by 0.2 percent. Medical care costs nudged up 0.3 percent, driven by a 0.4 percent increase in physician services, while hospital services saw only a marginal 0.1 percent uptick. Prescription drug prices remained unchanged. Prices for used cars and trucks rose 0.9 percent, while household furnishings and recreation posted gains of 0.4 percent and 0.3 percent, respectively. Other categories, including apparel, personal care, and motor vehicle insurance, also saw price increases. In contrast, airline fares fell sharply by 4.0 percent, erasing a January uptick, and new vehicle prices dipped 0.1 percent.

February 2025 US CPI headline & core month-over-month (2015 – present)

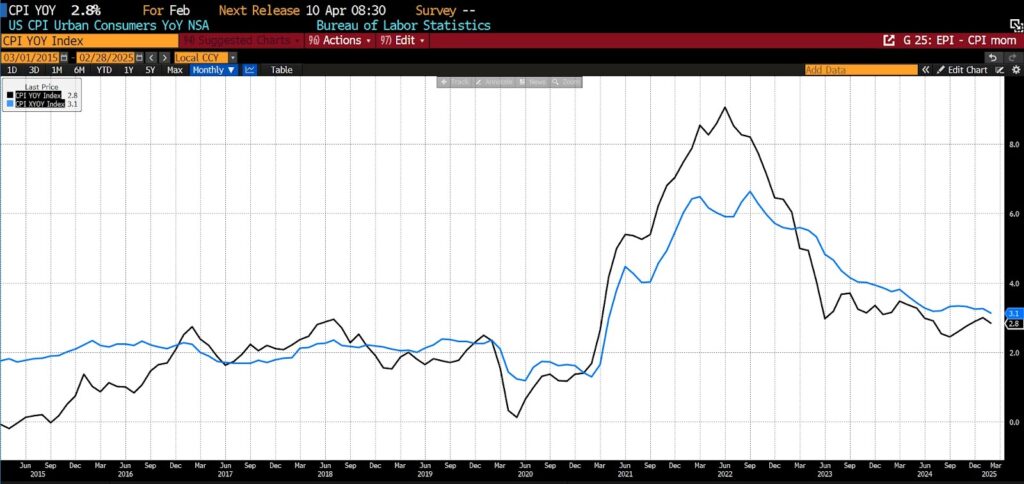

The headline CPI reading came in at 2.9 percent on a year-over-year basis, exceeding expectations of a 2.8 percent rise. Year-over-year core CPI also rose slightly more than forecast as well, with a 3.2 percent rise from February 2024 to February 2025.

February 2025 US CPI headline & core year-over-year (2015 – present)

Over the twelve months the cost of food at home increased by 1.9 percent, with notable variation across the categories. Meat, poultry, fish, and egg prices surged 7.7 percent, driven by a staggering 58.8-percent rise in egg prices owing to the largest avian flu outbreak in recorded history. Nonalcoholic beverages saw a 2.1 percent increase, while dairy and related products rose 0.8 percent. Cereal and bakery product prices climbed up 0.3 percent. Other food at home registered a slight 0.1 percent gain. By contrast, fruit and vegetable prices declined by 0.2 percent.

Dining out became more expensive over the past twelve months, with the food away from home index climbing 3.7 percent year-over-year as full-service and limited-service meal costs rose a similar 3.7 percent and 3.5 percent simultaneously.

Energy prices declined slightly over the past 12 months, with the overall energy index falling 0.2 percent. Gasoline prices dropped 3.1 percent and fuel oil saw a steeper decline of 5.1 percent. Those decreases, anticipated owing to the recent decline in world oil prices, were offset by higher household energy costs: electricity prices rose 2.5 percent and natural gas prices were up 6.0 percent. Shelter costs climbed 4.2 percent, notching its slowest annual increase since December 2021. Other categories posted notable gains since February 2024, including motor vehicle insurance (11.1 percent), education (3.7 percent), medical care (2.9 percent), and recreation (1.8 percent).

February’s CPI report highlights weakening consumer demand for discretionary goods, and disinflation in tariff-sensitive categories (automobiles, home furnishings, and apparel) appears to have stalled – perhaps because of price pressures generated by above-average inventory stocking activity in advance of anticipated levies.

Looking ahead, maintaining downward inflation momentum may prove difficult, particularly in the goods sector. Seasonal factors could push new-car prices higher, and tariffs scheduled for April 2nd — most particularly on auto parts from Canada and Mexico — pose an additional risk. Core services inflation is likely to decelerate further in the second quarter owing to slackening consumer demand, although the impact may be moderated by BLS changes to the weight given to housing in the overall index. At present, by the end of 2025 headline CPI is projected to hover around 2.7 percent, with core inflation slowing to 2.8 percent.

Despite somewhat softer consumer price data, market expectations for Federal Reserve rate cuts have moderated with less than one cut now priced in for June and roughly 68 basis points of cuts anticipated for the full year. While tariffs on Canadian, Mexican, and Chinese imports are likely to result in a one-time upward price adjustment, the potential for reciprocal tariffs to escalate into a pattern of one-upmanship among a broader set of US trading partners could generate inflation-like pressures in various goods. Tariffs are unlikely to be benign, but their impact on the current disinflationary trend — whether as a further drag or a more challenging setback to progress already made — remains to be seen.