With house prices moderating across much of the US, industry professionals and commentators are now beginning to talk about “housing oversupply” in certain markets.

Media outlets and trade groups have offered similar framing.

“[Florida and Texas] not only became red-hot during the pandemic,” Newsweek reported, “but also initiated a construction boom that, once the home-buying frenzy waned, left an oversupply of homes on the market right as the number of those wanting to buy, or able to afford them, was dwindling.”

“The main culprit for slowing price growth?” National Mortgage Professional asked. “An oversupply of homes relative to buyer demand, as affordability challenges and economic uncertainty continue to weigh heavily.”

Maybe these writers are using the term “oversupply” in a way that makes sense in their industries, but what they’re really referring to is a disequilibrium that causes prices to fall. The illogical mistake some people make is to infer from this temporary surplus that we should no longer pursue regulatory reform to increase the supply of housing.

This mistake has found its way into The Washington Post: “Over the next five years, estimates show that demographic shifts and a surge in construction will supply enough units to bring down prices and resolve the housing crisis.” Because of this, the author claims, the Yes in My Back Yard movement’s focus on reforming regulations is unwarranted.

At a conference last month in Florida, I heard the same thing from a pair of real estate professionals: We don’t need more supply; there’s already too much unsold inventory.

What’s wrong with this view is that it confuses a temporary disequilibrium with a shift outward in our production possibilities. When economists think about “supply,” we mean the entire schedule of feasible prices and quantities under existing technology. (Think about “technology” broadly, to include the costs of regulatory compliance.)

What’s happened in most of the Sunbelt is a combination of two things. First, there was a temporary outward shift in supply caused by negative real interest rates in 2021–2023. Builders had a strong incentive to borrow, just as home buyers had a strong incentive to take out big mortgages. They could finance new construction at lower costs. In places where the regulations allowed a lot of new construction, that’s just what we saw, but it took a few years for those homes to reach the market because even under the best of circumstances, it takes a long time to design, permit, build, inspect, and market a bunch of new homes.

Second, the unusual monetary environment during the pandemic also stimulated housing demand. But this was a temporary shift in demand, concentrated in places with high amenities where “work from home” was feasible. As mortgage rates rose again and inflation fell, driving real rates sharply higher, the for-sale housing market locked up. Demand fell, but inventories remain depressed because potential sellers want to avoid trading a low-rate mortgage for a high-rate one.

Thus, much of the Sunbelt region — especially those places where regulations allowed a lot of new building and where demand initially surged the most because of amenities like mild climate and access to beaches or mountains — is now experiencing falling housing demand alongside the tail end of a temporary supply boom. For the market to reach equilibrium, it is necessary for prices to fall.

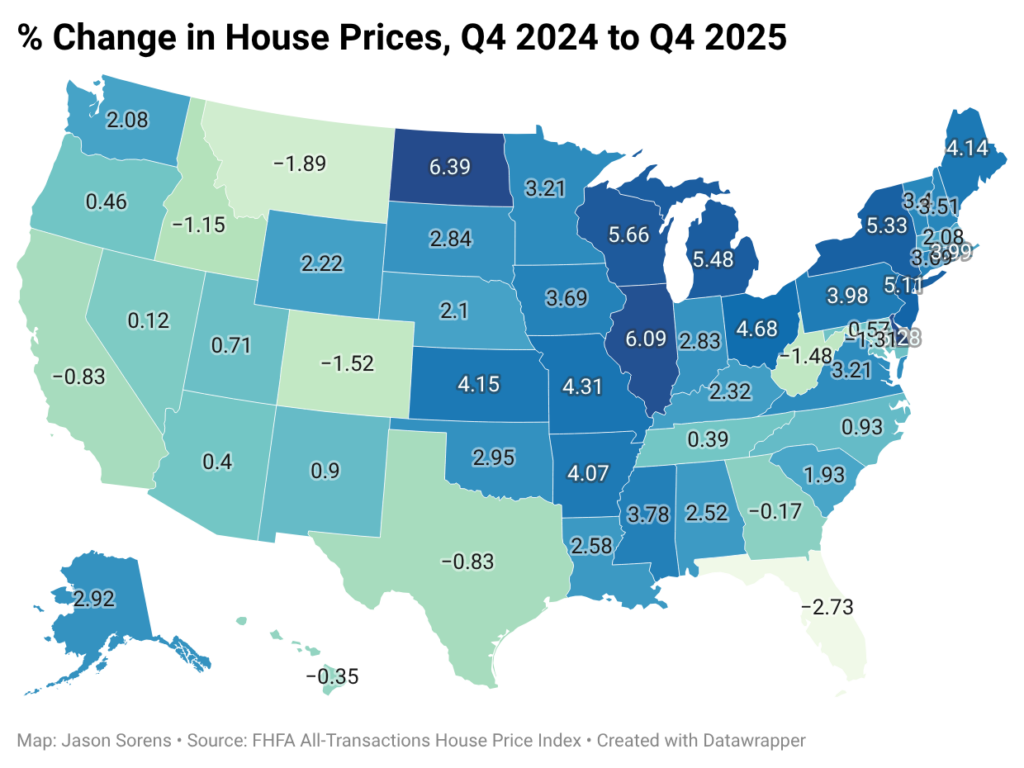

And that’s just what we see. Figure 1 shows the percentage change in single-family house prices by state between the fourth quarter of 2024 and the fourth quarter of 2025.

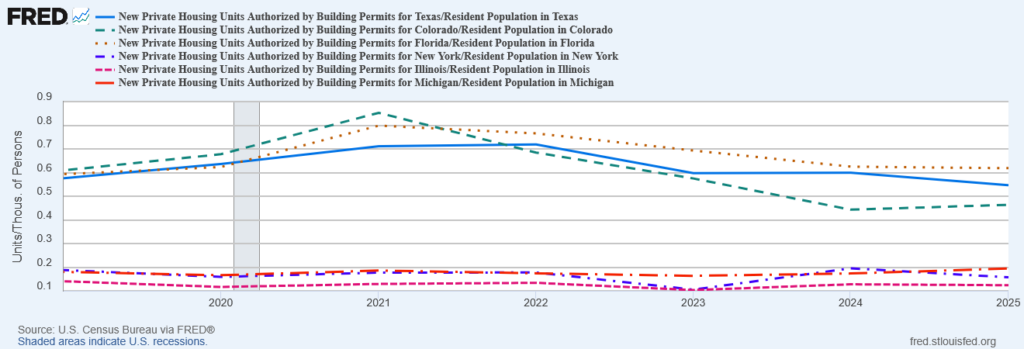

Florida had the biggest price decline in the entire US. Most of the West has seen sluggish price growth or outright declines. At the other end of the spectrum, some traditionally low-demand states, like New York, Illinois, and Michigan, have seen strong house price growth. They never saw the pandemic building surge that the Sunbelt did. Figure 2 shows building permits per capita for Florida, Texas, Colorado, Illinois, New York, and Michigan from 2019 to 2025.

The three fast-growing states have permitted anywhere from two to six times as many homes per capita as the three slow-growing states. The pandemic permitting boom is barely discernible, if at all, in the data from New York, Illinois, and Michigan. With no supply hangover to work through, it is unsurprising that house prices have risen there in the last year.

We shouldn’t overinterpret these short-term figures. House prices in California are not going to fall to the level of Michigan’s, or anywhere close. But more importantly, we should not overinterpret the cyclical data to reject policy solutions for housing abundance that involve permanently shifting out the supply curve. When we require less land and parking per unit of housing, less time to get permits and inspections, and lower risks of getting tangled up in court, we make housing development more productive: we get more housing for the labor and materials we dedicate to building it.

The case for YIMBY reforms never depended on the pandemic house price cycle. If we can reform regulations to reduce what it costs to build new homes of equivalent quality, we can have more housing and lower housing costs for the long term, not just the trough of a momentary cycle. The case for more housing abundance is just as strong in states where prices are falling as it is in states where prices are rising. Some of the states where prices are falling might be closer to housing abundance than others, because their regulations did less to choke off new supply during the pandemic to begin with, but no one has gotten the policy regime precisely right.

The promise of regulatory reform is that when we allow the market to deliver the right types of housing in the right places at sustainable costs, we’ll all be better off.