Locksley Resources Limited (ASX: LKY,OTC:LKYRF; OTCQX: LKYRFADR: LKYLY announced high-grade antimony (Sb) assays received from surface exposure grab sampling, with a peak value of 16.90% Sb confirm continuity of high-grade stibnite mineralization along strike and above the historical undergro8und workings at the company’s Desert Antimony Mine located within the Company’s Mojave Project in California.

These samples were collected from earthworks conducted during preparation for the maiden drilling program currently underway. The work identified extensions of stibnite-bearing mineralized veins at surface, further validating the system’s high-grade continuity and strike potential. Additional information can be found here: https://cdn-api.markitdigital.com/apiman-gateway/ASX/asx-research/1.0/file/2924-03063849-6A1314564&v=undefined.

The results continue to reflect the company’s strong technical foundation and focus on high-confidence targets. Ongoing diamond drilling at DAM is expected to further refine geometry and evaluate resource potential.

Locksley Resources (https://www.locksleyresources.com.au) is focused on critical minerals in the U.S. The company is actively advancing the Mojave Project in California, targeting rare earth elements (REEs) and antimony. Locksley is executing a mine-to-market strategy for antimony, aimed at reestablishing domestic supply chains for critical materials, underpinned by strategic downstream technology partnerships with leading U.S. research institutions and industry partners. This targeted approach, combined with resource development with innovative processing and separation technologies, positions Locksley to play a role in advancing U.S. critical materials independence.

View original content:https://www.prnewswire.com/news-releases/locksley-announces-high-grade-antimony-assays-at-desert-antimony-mine-confirm-surface-continuity-302701977.html

March 2nd, 2026 TheNewswire – Muskoka, Ontario Steadright Critical Minerals Inc. (CSE:SCM,OTC:SCMNF) (‘Steadright’ or the ‘Company’) is pleased to announce that it has closed the first tranche of its previously announced non-brokered private placement (the ‘Offering’), pursuant to which the Company sold 4,336,816 Units (the ‘Units’) in the capital of the Company at a price of $0.25 per Unit, for aggregate gross proceeds of $1,084,204.00. The Company intends to use the net proceeds for general working capital and corporate purposes.

Each Unit is comprised of one common share in the capital of the Company (each a ‘Common Share’) and one common share purchase warrant (each, a ‘Warrant’). Each Warrant entitles the holder to acquire one further Common Share at a price of $0.31 per Common Share for a period of twenty-four months from the date of issuance.

In consideration for their services, certain finders received a cash commission (the ‘Commission‘) equal to 8.0% on eligible subscriptions of the gross proceeds of the Offering totalling $56,300.00 and a broker warrant commission equal to 8% on eligible subscriptions of the gross proceeds of the Offering (the ‘Broker Warrants‘), being 225,200 Broker Warrants. The Commission was paid in accordance with the policies of the Canadian Securities Exchange and relevant Canadian securities laws.

The Common Shares, Warrants and Broker Warrants issued pursuant to the Offering will be subject to a regulatory hold period of four months and one day from the date of issuance. The Offering remains subject to final Canadian Securities Exchange acceptance of requisite regulatory filings.

Says Steadright CEO, Matt Lewis, ‘We are quite encouraged by the enthusiasm surrounding the first tranche of our capital raise, and are also working hard progressing our Moroccan assets forward.’

ATRIUM RESEARCH REPORT:

Atrium Research on February 27, 2026 disseminated an Initiation Research Report:

Steadright Critical Minerals – Strategic Moroccan Acquisitions; Fast-Track to Production

Steadright Critical Minerals is a mineral exploration company established in 2019. Steadright has been focused since late spring 2025 on finding exploration and historical mining projects that can be brought into production within the Moroccan critical mineral space. Steadright currently has exposure through a Moroccan entity known as NSM Capital Sarl, with over 192 sq KMs of mineral exploration claims called the TitanBeach Titanium Project, and found in the Southern Provinces of Morocco. Steadright also has signed a Binding MOU for the historic Goundafa Mine within the Kingdom of Morocco, has acquired the Copper Valley historic copper-lead-silver project and has an LOI with SilverLine Mining Sarl.

ON BEHALF OF THE BOARD OF DIRECTORS

For further information, please contact:

Matt Lewis

CEO & Director

Steadright Critical Minerals Inc.

Email: enquires@steadright.ca

Website and Company Presentation: www.steadright.ca

Phone: 1-905-410-0587

Neither the Canadian Securities Exchange (the ‘CSE’) nor its Regulation Services Provider (as that term is defined in the policies of the CSE) accepts responsibility for the adequacy or accuracy of this release.

This news release contains ‘forward-looking information’ within the meaning of applicable Canadian securities legislation. Forward-looking information in this release includes, but is not limited to, statements regarding the completion and size of the Offering, the expected use of proceeds, the potential payment of finder’s fees, the receipt of all necessary regulatory approvals, and the Company’s business plans and exploration objectives. Forward-looking information is subject to known and unknown risks, uncertainties and other factors which may cause the actual results, performance, or achievements of Steadright to be materially different from those expressed or implied by such forward-looking information. Such risks and uncertainties include, but are not limited to: the risk that the Offering may not be completed or may not be completed on the terms described herein; the use of proceeds may differ from management’s current expectations; the risk that regulatory approvals may not be received in a timely manner, or at all; risks related to the junior mining and exploration industry generally; fluctuations in commodity prices; access to financing on acceptable terms; general economic, market and business conditions; and changes in laws and regulations. Although Steadright has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking information, there may be other factors that cause results not to be as anticipated, estimated or intended. Forward-looking information contained herein is based on management’s current expectations, estimates, projections, assumptions and beliefs, and is provided as of the date of this news release. Steadright does not undertake to update any forward-looking information, except as required by applicable securities laws.

This news release does not constitute an offer to sell or a solicitation of an offer to buy any of the securities in the United States. The securities have not been and will not be registered under the United States Securities Act of 1933, as amended (the ‘U.S. Securities Act‘) or any state securities laws and may not be offered or sold within the United States or to, or for the account or benefit of, U.S. Persons unless registered under the U.S. Securities Act and applicable state securities laws, unless an exemption from such registration is available.

Not for distribution to United States Newswire Services or for dissemination in the United States

Copyright (c) 2026 TheNewswire – All rights reserved.

– Copper Intelligence is pleased to announce together with our drilling partner Gemdrill, that the company’s XY–44 drill rig will be transported to the Butembo DRC project site. Transit time is estimated at approximately 2–3 weeks, ensuring the rig is on the ground and ready to support the company’s upcoming Butembo drilling campaign. The company anticipates a travel window of approximately 2–3 weeks to get the XY–44 drill to the DRC border. From that point, unloading will occur at the yard in the town of Kasindi, enabling the triaxle long-range transport truck. A further week is estimated to mobilize all equipment to site. One additional week will be required to establish camp, stabilize the drill setup, organize equipment, and complete all necessary preparations before drilling can commence.

Barring any customs or transit issues enroute, it is anticipated that the drill will be operational mid-April with initial site-based analyses of copper ore core being released at the beginning of May.

The company anticipates a social media and in-person Analyst Day for the attendance of Sell-Side and Institutional Investors to be held and televised from the Democratic Republic of Congo in the mid-May timeframe.

About ‘ Copper Intelligence ‘

On Feb 4, 2026, African Discovery Group (AFDG), the predecessor company to Copper Intelligence, announced the signing of Definitive Sales and Purchase Agreement (SPA) for the Butembo Copper Asset in the Democratic Republic of Congo, in a Reverse Takeover Transaction (RTO), solidifying its status as the first stand-alone DRC company to be publicly traded in the United States. Butembo is a near surface, low strip, Tier one exploration opportunity, located near the Ruwenzori mountain location of Uganda’s biggest copper mine (Kilembe with 4 million tons of verified reserves), located only 50km from the Ugandan border with verified access to rail. The High-grade copper samples thus far have returned 18% Copper assays, which if maintained at production would rank amongst the highest globally. The recent discovery of the Butembo copper deposit has underscored the need for further exploration work in areas peripheral to the Katanga Copper Belt.

Media Contact: www.copperintelligence.com Maxine Gordon mg@africandiscoverygroup.com

View original content:https://www.prnewswire.com/news-releases/afdg—copper-intelligence-announces-transportation-of-drill-rig-to-butembo-302702421.html

What are zoning laws, how do they work, and what are their economic effects?

This explainer is intended to be a guide to the purposes and mechanics of local land-use regulations, including zoning, as well as the economic debates over their effects, especially on the housing market, and how to reform them.

1. What Zoning Is

Zoning is a set of laws that regulate how property owners may use their land, in particular by drawing zones where certain uses are and are not permitted. Most zoning laws are local ordinances adopted by county or municipal governments, but some are state laws adopted by legislatures or executive agencies.

While zoning regulates building, “zoning codes” are different from “building codes.” Building codes are standards for construction meant to address life safety issues, such as fire safety and energy efficiency.

Planners and local governments often treat “zoning” separately from other land-use or development regulations. Regulations affecting the subdivision of land, the layout of site plans, and environmental standards like those having to do with development activities near wetlands or above aquifers are all closely related to zoning. Sometimes these laws are found in zoning ordinances and sometimes in separate ordinances. “Master plans” are typically advisory documents meant to inform zoning changes, but in practice, they often diverge sharply from what zoning ordinances actually allow.

Zoning is a relatively recent phenomenon in the United States. New York City adopted the first comprehensive zoning ordinance in 1916, but cities had implemented piecemeal land-use regulations before this date.[1]

Zoning quickly spread nationwide. Under Secretary of Commerce Herbert Hoover, the federal government adopted a draft “zoning enabling act” in 1924 and promoted its enactment by state legislatures. Most states quickly adopted zoning enabling acts in the 1920s. Excluding the then-territories of Alaska and Hawaii, the last state to adopt a zoning enabling act was Washington (1935).

Before zoning, land use was regulated through private covenants: contracts that limited how landowners could use their property, and that “ran with the land,” meaning they passed to future buyers and renters. Private covenants are still important in the US, but they are now used mainly for two purposes: creating conservation easements that limit development on agricultural land or wilderness, and establishing homeowners’ associations that manage common facilities and regulate development in a single neighborhood.

Why did zoning start in the 1910s and 1920s? One reason may be the rise of the automobile, which allowed workers for the first time to live far from their jobs. As suburban neighborhoods grew, residents sought to keep urban uses at a distance. Zoning was a tool for that separation.

Progressive Era optimism about the ability of experts to use scientific principles to re-engineer daily lives through government also played a role. Within the field of urban planning, the early progressives’ ambitions gave way in the 1940s and 1950s to even grander “high modernist” visions to redesign cities according to abstract principles of beauty and order (Scott 1998). These ideological commitments played a role in the American “urban renewal” projects of the 1950s and 1960s that bulldozed neighborhoods, widened roads, drove highways through the centers of cities, and rezoned land to require large parking lots and front yards.

Some scholars still debate whether racism played a role in the development and spread of zoning. Certainly, some cities tried to use zoning for racial and socioeconomic segregation, even after the Supreme Court struck down explicitly racial zoning in 1917. But there were also prominent black advocates of zoning (Glock 2022). FDR’s Federal Housing Administration (FHA) used redlining — excluding certain neighborhoods from their mortgage guarantee program — to reinforce urban segregation. To this day, many zoning boundaries follow the red lines that the FHA drew suspiciously closely (Rothstein 2017; Trounstine 2020). Urban renewal policies, especially interstate highway construction, damaged urban working-class areas of cities, both predominantly black and ethnic-white (Peterson 2023). Perhaps the most supportable conclusion is that racism sometimes played a role in the purposes to which zoning was put, but the level of racism in society is not a good predictor of the stringency of zoning over time, since especially restrictive forms of zoning first emerged in the 1960s and then spread to fast-growing regions during the period from the 1970s through the 2000s.

In fact, a social trend that tracks better with the rise of especially restrictive zoning is the spread of anti-growth environmental attitudes in the 1960s and 1970s (Fischel 2015). During this era, environmentalism was closely associated with anti-population-growth views, and ultra-low-density zoning seems to have emerged first in places with strong environmental movements. Up to the present day, local Sierra Club chapters have often been key vehicles for anti-housing activism (Elmendorf 2023), despite the fact that low-density zoning in metropolitan areas tends to encourage sprawl.

2. How Zoning Works

The basic role of zoning is to separate potentially annoying or noxious uses from residential neighborhoods. Economist William Fischel calls this “good housekeeping zoning” (Fischel 2015, 325).

Traditional zoning isn’t the only way to regulate nuisances. One former city planner and zoning skeptic notes that, rather than dividing a city into districts with different permitted uses, ordinances could simply specify that obnoxious uses may not locate within a certain distance from an existing home (Gray 2022). Under traditional zoning, a nuisance use can be located close to a home so long as it’s just over the line in a zoning district where that use is allowed.

From early on, zoning went beyond regulating genuine nuisances. The famous Euclid v. Ambler Supreme Court case that upheld the constitutionality of zoning in 1926 was about an ordinance that forbade the building of apartments in one part of the village of Euclid, Ohio. The majority opinion held that restricting apartments was a reasonable use of the government’s police power, since “very often the apartment house is a mere parasite, constructed in order to take advantage of the open spaces and attractive surroundings created by the residential character of the district,” and apartment houses in residential districts “come very near to being nuisances” (272 US 394–95).

Today, almost all zoning ordinances limit residential densities, even in the most densely populated neighborhoods in the country. Setting aside land for detached, single-family housing is also standard. Single-family zoning is virtually unknown outside the US and Canada (Hirt 2014), but limits on residential densities are near universal (Hughes 2025). Limits on densities may, within reason, safeguard the value of residential properties in a neighborhood.

Another application of zoning is to make sure that new development “pays its own way.” If new development requires building roads or expanding schools, zoning regulations can require the development to pay enough in property taxes to cover the marginal cost of providing these services. Requiring that new homes purchase a lot of land with their house, through minimum lot sizes, might be a roundabout way of doing this.

Another, arguably simpler way of ensuring that developments make fiscal sense for the local community is to use narrowly constructed impact fees. Impact fees are payments that property owners have to make in order to build a certain kind of development. These funds can then be used to upgrade infrastructure, hire teachers, or otherwise fulfill the need created by the new development.

Like any other government exaction, impact fees can be — and often have been — abused. They only make sense if they cover the net cost of a development to local property taxpayers. Since development typically raises the value of property substantially, it always pays at least part of its own way. The most credible academic research on this question suggests that multifamily housing and small-lot single-family subdivisions tend to pay their own way fully through their added property tax revenues, at least when it comes to school enrollment impacts (Gallagher 2016; 2019). If that’s true, then it wouldn’t make sense to impose school impact fees on these types of developments.

If a property owner wants to do something that is prohibited under zoning, localities offer processes for various exceptions. It’s impossible for a zoning ordinance and a zoning map to anticipate all possible valuable uses for every specific piece of land for all time. The most typical process is to obtain a “variance,” or a waiver of the zoning regulations in a particular instance.

Alternatively, the map itself can be changed through a rezoning — but this process usually makes sense only for large projects. These processes are at least somewhat discretionary; a property owner is never entitled to a variance or a rezoning.

3. Understanding Your Local Zoning

To see what kinds of regulations your area has, you can look up your local zoning or development ordinances and zoning map. Here’s what to look for.

In larger towns that have the assistance of professional staff in drawing up regulations, ordinances will typically have a table of uses and a table of dimensional regulations. The table of uses will tell you what uses are allowed or prohibited in each district, and the table of dimensional regulations will tell you the minimum and maximum requirements for lots and buildings.

Figure 1 shows a portion of a table of uses from Nashua, New Hampshire’s zoning ordinance. Like the vast majority of other zoning ordinances in the US, the Nashua ordinance considers a use prohibited unless it is expressly permitted. Some uses are only permitted if they are “accessory” to specific other uses, that is, they are not the main use of the land. Some uses are neither permitted nor prohibited outright, but require a special permit from a land-use board. These special permits are typically offered on a partially discretionary basis, such that a landowner has to prove that the new use will meet pre-established criteria.

As you can see from Figure 1, the commercial uses that happen to be listed here — different kinds of lodging establishments — are not a permitted use in any of the residential districts, but they are in the downtown and business districts, and they are allowed by a special permit in some of the urban residential districts. This kind of separation of uses is typical.

Home businesses, however, are treated as an accessory use. Most zoning ordinances will allow home-based businesses in at least some neighborhoods, but they typically impose restrictions such as maximum square footage or maximum number of employees, to limit the size and impact of these businesses.

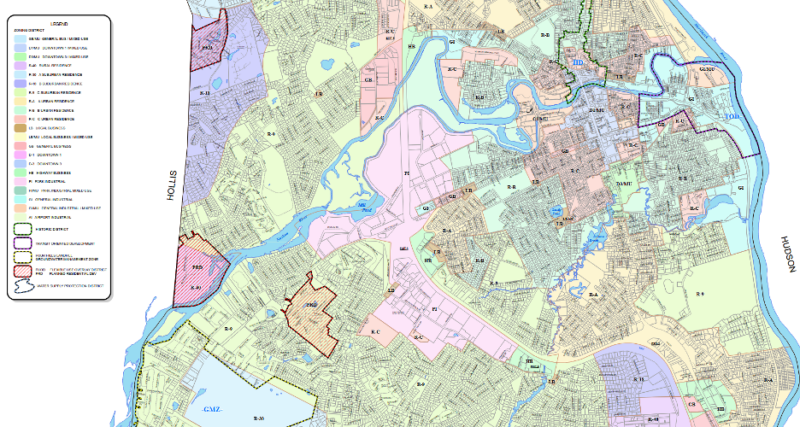

The zoning districts in the columns of Figure 1 are plotted on a zoning map. Figure 2 displays a portion of the zoning map for Nashua. There are two types of zoning districts on this map: base districts and overlays. Base districts correspond to the regulations that apply outside an overlay. An overlay district modifies the regulations in the base district in certain respects (but not others). These modifications could make the regulations stricter or less strict.

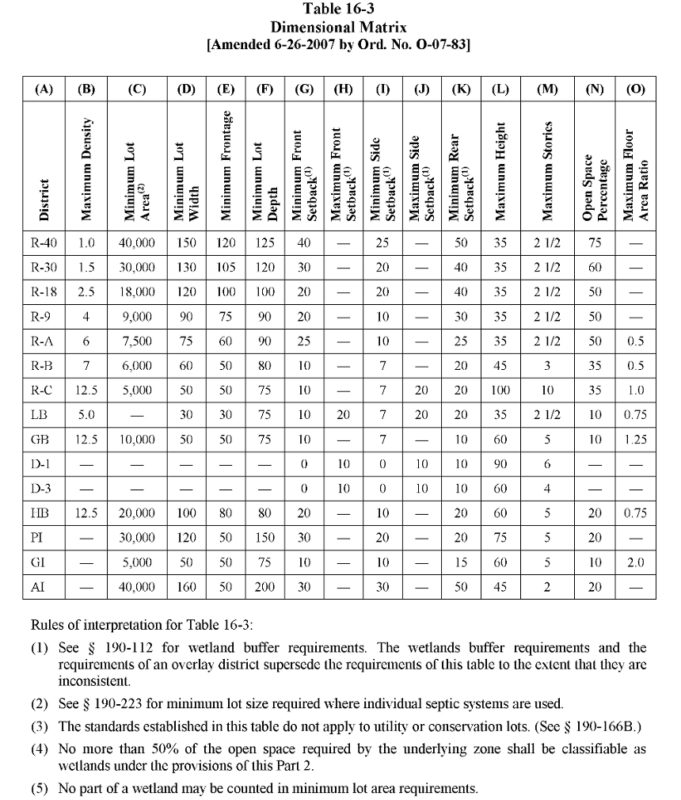

Finally, Figure 3 shows a portion of Nashua’s table of dimensional regulations. These regulations limit how much you can build. Maximum density regulations limit the number of dwelling units you can build per acre. Minimum lot sizes tell you how much land you must have per house. Minimum setbacks tell you how far back the building must sit relative to lot lines. Maximum setbacks are less common but are gaining in popularity as planners lose interest in the high-modernist ideal of low-slung buildings surrounded by seas of grass and asphalt. Floor area ratios limit how much floor space you can build relative to the size of the lot; they’re an especially complex way to limit building space. Finally, minimum open space percentages, sometimes specified as maximum lot coverages, are in theory justified as a flood-prevention measure, making sure there’s enough space for rainwater to permeate the soil. To use them properly for flood prevention, however, they would need to scale with the size of lots and the flood-proneness of the surrounding area. It might be more efficient sometimes just to pay people to keep some land as open space.

Regulating uses and dimensions aren’t all that zoning ordinances do, but they’re among the most consequential. A nationwide project to map and tabulate key zoning ordinances affecting housing development is underway: the National Zoning Atlas. If you’re lucky enough to have your area covered by this atlas, you can dig into the data and see what types of housing are allowed where. The “snapshots” tool lets you compare jurisdictions by the percentage of land area they make available for certain types of housing.

4. The Consequences of Zoning

Economists pay attention to zoning because zoning makes it harder and more costly to build housing. Zoning is also often the only tool residents possess to limit nearby land uses that may lower their own property values without constituting true nuisances.

Everyone agrees zoning raises the cost of housing, but debate continues over whether it does so primarily by restricting supply, or also by increasing demand. If zoning is a wise tool for regulating nuisances and making neighborhoods more pleasant, it should boost housing demand as well as constrain supply.

Zoning limits housing supply in two ways: raising monetary costs and raising time costs. We have already seen the first of these. Zoning often requires more land to be used to build than a property owner might prefer to buy. Zoning can also raise the monetary cost of building by requiring particular building features, such as parking spaces.

Zoning also raises the time cost of building housing. Getting approvals, especially for special permits or variances, takes time — often an uncertain amount of time.

Zoning raises the cost of housing in a way that more closely resembles a fixed, per-unit tax than a tax that scales with the value of the property (“ad valorem”). Developers have an incentive to develop higher-priced properties, so that the fixed “land use tax” represents a smaller proportion of the ultimate sale price. For this reason, we should be cautious about attributing rising housing costs solely to larger and higher-quality homes. Houses are probably inefficiently large and high-quality, especially in more regulated regions. Lots of Americans want starter homes but are unable to find them, because even a small house is costly to build in a manner consistent with zoning.

Some economists have found that zoning can raise the demand for housing and make neighborhoods nicer to live in, compared to the alternative of completely unregulated land use (Speyrer 1989; Lin 2024; Gyourko and McCulloch 2024).

Quite a few studies have found that stricter zoning makes housing development more costly and less efficient, and may even account for the otherwise hard-to-explain decline in construction productivity in the United States (Siegan 1972; Glaeser et al. 2005; Hsieh and Moretti 2019; Molloy 2020; D’Amico et al. 2024).

One of the most startling examples of this phenomenon comes from Palo Alto, California, home to Stanford University and the headquarters of HP and the former headquarters of Tesla. Even at the very center of the global tech economy, most of the housing in Palo Alto is restricted to low-slung, single-family neighborhoods because of zoning laws. The only part of town where housing is legal to build at significant density is far away from corporate headquarters, next to San Francisco Bay and industrial port facilities. Still, it receives all the major residential construction (Ellickson 2022).

On the one hand, it’s understandable that homeowners in Palo Alto are nervous about allowing big apartment buildings down the block. On the other hand, the economic costs of freezing their neighborhoods in amber are gigantic. In principle, you could make Palo Alto homeowners better off by allowing high-density construction in their neighborhoods and giving them a big chunk of the increase in land value that results.[2] But traditional zoning doesn’t have mechanisms to authorize side payments of this kind.

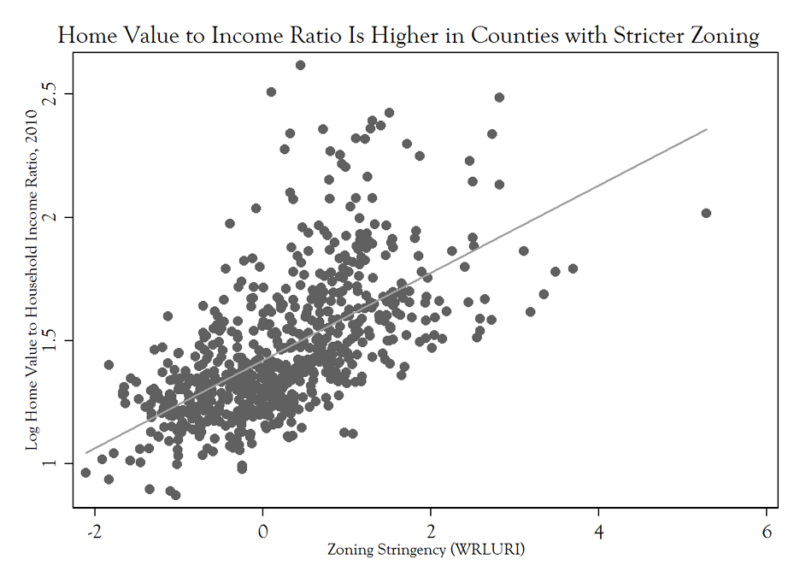

The national evidence that zoning stringency and housing costs correlate is quite strong. For example, Figure 4 shows that in counties with stricter zoning, the ratio of median home value to median household income is higher.

Now, the causality might go both ways. Places that are nicer to live in or boast faster wage growth will have higher housing demand and therefore higher prices and population growth. That population growth might prompt these places to tighten their zoning regulations, yielding a partly spurious correlation between regulatory stringency and housing costs.

But if that alternative causal channel were the main explanation, it would be surprising to see more strictly regulated areas experiencing slower population growth. That argument depends on zoning being the result of rapid growth, rather than the cause of high costs and slow growth. If more strictly regulated places show high costs and slow growth, that should fortify our conclusion that the high costs are a consequence of strict zoning.

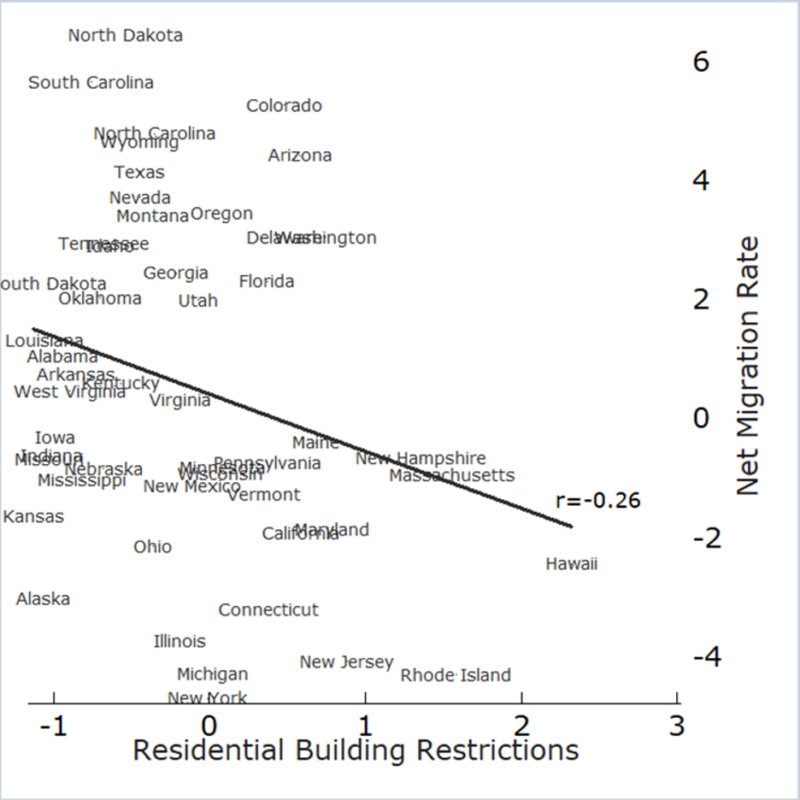

And that’s exactly what we do see. Figure 5 shows the relationship between zoning stringency and net migration rates at the state level. States with stricter zoning are losing people to states with looser zoning. This chart likely understates the negative causal effect of zoning on net migration, since states with historically high migration were more likely to tighten zoning in the first place.

These charts are suggestive and easy to understand, but from economists’ perspective, the only gold-standard evidence of causal effects comes from interventions that are more plausibly random. Careful studies of zoning regulations changes generally find that when regulations are loosened, housing production goes up, and housing costs go down, relative to the counterfactual — but the effect on costs depends on the geographic scale of the change (Cheung et al. 2023; Greenaway-McGrevy 2023; Büchler and Lutz 2024). Localized changes have almost no effect on local housing costs, while a regional change has a substantial effect on regional housing costs.

Zoning should also make commercial and industrial development more difficult and costly. In many cases, however, communities are more willing to allow commercial development than residential, since it shifts some of the property tax burden away from residential owners. This remains an area of future research, and state policymakers have been exploring ways to relax zoning rules for home-based commercial uses, such as childcare.

5. Options for Reform

Policymakers have looked to zoning reform in recent years as a way to bring down housing costs. This is a partial list of reforms that states and cities have been trying.

5.1. Institutional and Process Reforms

Process-level zoning reforms currently being tried include:

Providing a quick appeals process or appeals board for zoning denials to reduce the time cost of development.

Tightening who has standing or may challenge housing-friendly rezonings.

Compensating owners for regulatory takings. Under current jurisprudence, the federal Constitution only requires compensation for regulatory takings that eliminate economically viable uses of land, necessitating state-level reforms.[3][4]

Raising voter turnout by aligning local election calendars to state elections, as a motivated minority of anti-building homeowners have outsized pull in off-cycle elections (Einstein et al. 2020).

Using “shot clocks” to limit the time local boards can delay permit applications.

Allowing builders to use certified third-party inspectors and other private agencies.

Centralizing zoning, allowing state government to define all the possible zoning districts that its local governments can use, allowing local governments to then map these districts as they like. This approach raises the risk that anti-housing groups will focus on state-level influence.

Decentralizing zoning by allowing neighborhoods or even single streets to opt out of local zoning, if they recognize the financial benefit in allowing more housing to be built.

Making covenants more attractive, including authorizing city governments to use their own resources to enforce private covenants (Gray 2022).

5.2. Zoning Preemption

State governments could simply preempt local zoning in some areas, giving landowners defined rights to develop certain kinds of housing.

Build starter homes. In 2025, Texas enacted the first limit on minimum lot sizes in cities, making it easier to build subdivisions of small-lot homes.

Promote “missing middle” reforms. Some states have ended single-family zoning in larger cities or in areas that have access to water and sewer infrastructure, allowing developers to build out the “missing middle” typologies: duplexes, triplexes, and fourplexes.

Reduce parking minimums. Parking minimums are one of the most irrational land-use controls, and more than 100 cities have limited or abolished them.

Legalize accessory dwelling units. Quite a few states have now passed laws giving single-family homeowners the right to build a small apartment or tiny home on their lot.

Legalize manufactured housing. States are increasingly requiring local governments to allow manufactured housing wherever they allow single-family housing.

Legalize single-room occupancies, allowing dorm-like arrangements with shared kitchens or bathrooms, which function as the lowest rung on the housing ladder and may do the most to reduce homelessness.

5.3. Financial Incentives

Many states now offer some financial incentives or technical assistance to local governments that want to reform zoning in a housing-friendly direction. Some states now give additional infrastructure dollars to local governments that permit more housing. New Hampshire’s Housing Champions program is an example. The ROAD to Housing Act that recently passed the US Senate would do the same with some federal funds.

Financial incentives work best when localities must demonstrate a real increase in permitting, not just a legal change, as a condition of continuing to receive the incentive. Localities have innumerable ways to block or discourage projects they don’t want, so actual permitting data reveal a community’s regulatory stance more accurately than the text of its zoning ordinances.

6. Advantages and Alternatives to Zoning

Many Americans believe that zoning serves useful functions in protecting their quality of life and property values. In established neighborhoods, private covenants are difficult to create, making zoning the primary way to govern land use. Economics helps clarify the tradeoffs of zoning and how it can be reformed to serve its essential functions at lower cost.

For more on the politics and economics of zoning and how to reform it, see my AIER white paper, “Unbundling Zoning.”

References

Bernstein, David E. 1999. “Lochner, Parity, and the Chinese Laundry Cases.” Wm. & Mary L. Rev. 41: 211.

Büchler, Simon, and Elena Lutz. 2024. “Making Housing Affordable? The Local Effects of Relaxing Land-Use Regulation.” Journal of Urban Economics 143: 103689.

Cheung, Ka Shing, Paavo Monkkonen, and Chung Yim Yiu. 2023. “The Heterogeneous Impacts of Widespread Upzoning: Lessons from Auckland, New Zealand.” Urban Studies 61 (5): 943–67.

Coase, R.H. 1960. “The Problem of Social Cost.” Journal of Law and Economics 3 (1): 1–44.

D’Amico, Leonardo, Edward L Glaeser, Joseph Gyourko, William R Kerr, and Giacomo AM Ponzetto. 2024. Why Has Construction Productivity Stagnated? The Role of Land-Use Regulation. No. 33188. National Bureau of Economic Research.

Einstein, Katherine Levine, David M. Glick, and Maxwell Palmer. 2020. Neighborhood Defenders: Participatory Politics and America’s Housing Crisis. Cambridge University Press.

Ellickson, Robert C. 2022. America’s Frozen Neighborhoods: The Abuse of Zoning. Yale University Press.

Elmendorf, Chris. 2023. “How Major Environmental Groups Ended Up on the Wrong Side of California’s Housing Crisis.” Mother Jones, November 17. https://www.motherjones.com/environment/2023/11/green-groups-housing-crisis-ceqa-environmental-density-nimby/.

Fischel, William A. 2015. Zoning Rules!: The Economics of Land Use Regulation. Lincoln Institute of Land Policy.

Gallagher, Ryan M. 2016. “The Fiscal Externality of Multifamily Housing and Its Impact on the Property Tax: Evidence from Cities and Schools, 1980-2010.” Regional Science and Urban Economics 60: 249–59.

Gallagher, Ryan M. 2019. “Restrictive Zoning’s Deleterious Impact on the Local Education Property Tax Base: Evidence from Zoning District Boundaries and Municipal Finances.” National Tax Journal 72: 11–44.

Glaeser, Edward L., Joseph Gyourko, and Raven Saks. 2005. “Why Is Manhattan So Expensive?: Regulation and the Rise in Housing Prices.” Journal of Law and Economics 48 (2): 331–69.

Glock, Judge. 2022. “Two Cheers for Zoning.” American Affairs 6: 36–52.

Gray, M. Nolan. 2022. Arbitrary Lines: How Zoning Broke the American City and How to Fix It. Island.

Greenaway-McGrevy, Ryan. 2023. “Can Zoning Reform Reduce Housing Costs? Evidence from Rents in Auckland.” Working Paper No. 16. Preprint, University of Auckland Economic Policy Centre.

Gyourko, Joseph, and Sean E. McCulloch. 2024. “The Distaste for Housing Density.” NBER Working Paper 33078.

Hirt, Sonia. 2014. Zoned in the USA: The Origins and Implications of American Land-Use Regulation. Cornell University Press.

Hsieh, Chang-Tai, and Enrico Moretti. 2019. “Housing Constraints and Spatial Misallocation.” American Economic Journal: Macroeconomics 11 (2): 1–39.

Hughes, Samuel. 2025. “The Great Downzoning.” Works in Progress, November 24. https://worksinprogress.co/issue/the-great-downzoning.

Lin, Chuanhao. 2024. “Do Households Value Lower Density: Theory, Evidence, and Implications from Washington, DC.” Regional Science and Urban Economics 108: 104023.

Molloy, Raven. 2020. “The Effect of Housing Supply Regulation on Housing Affordability: A Review.” Regional Science and Urban Economics 80 (C): 1–5.

Peterson, Sarah Jo. 2023. “The Myth and the Truth About Interstate Highways.” In Justice and the Interstates: The Racist Truth About Urban Highways, edited by Ryan Reft, Amanda K. Phillips de Lucas, and Rebecca C. Retzlaff. Island.

Power, Garrett. 1983. “Apartheid Baltimore Style: The Residential Segregation Ordinances of 1910-1913.” Maryland Law Review 42 (2): 289–328.

Rothstein, R. 2017. The Color of Law: A Forgotten History of How Our Government Segregated America. Liveright. https://books.google.com/books?id=SdtDDQAAQBAJ.

Scott, James C. 1998. Seeing like a State: How Certain Schemes to Improve the Human Condition Have Failed. Yale University Press.

Siegan, Bernard H. 1972. Land Use Without Zoning. Rowman & Littlefield.

Sorens, Jason. 2018. “The Effects of Housing Supply Restrictions on Partisan Geography.” Political Geography 66 (September): 44–56.

Sorens, Jason. 2021. Residential Land Use Regulations in New Hampshire: Causes and Consequences. Josiah Bartlett Center for Public Policy.

Speyrer, Janet Furman. 1989. “The Effect of Land-Use Restrictions on Market Values of Single-Family Homes in Houston.” Journal of Real Estate Finance and Economics 2 (1): 117–30.

Trounstine, Jessica. 2020. “The Geography of Inequality: How Land Use Regulation Produces Segregation.” American Political Science Review 114: 443–55.

Endnotes

[1] For example, in 1915 San Francisco adopted an ordinance forbidding laundries in certain neighborhoods. Because these laundries were overwhelmingly Chinese-owned, this was a way of trying to keep Chinese workers out of wealthier neighborhoods (Bernstein 1999). Between 1911 and 1917, Baltimore, Louisville, and other cities adopted ordinances forbidding blacks and whites from living in neighborhoods majority occupied by members of the other race, ordinances struck down by the US Supreme Court in Buchanan v. Warley (1917) (Power 1983).

[2] This kind of deal is what economists call a “Coasean bargain” (Coase 1960). It makes no sense for regulations to prohibit people from making m utually beneficial exchanges.

[3] Arizona and Florida have laws requiring local governments to compensate landowners if they take away much of the value of their property through new zoning laws. Oregon had such a law, but it was radically scaled back.

[4] Penn Central Transportation Co. v. New York City, 438 US 104 (1978). 3): 454-466.

WACO, TEXAS — Two of this primary season’s fiercest rivals have one thing in common: unflinching support for President Donald Trump’s decision to strike Iran.

Texas Attorney General Ken Paxton and Sen. John Cornyn, R-Texas, are both leaning into their relationship with Trump and their record of support over the years as they vie for the Republican nomination in Texas’ contentious Senate primary. While it’s a crowded primary, including Rep. Wesley Hunt, R-Texas, all eyes are on Paxton and Cornyn.

And as they push for Trump’s coveted endorsement in the final stretch of their intense campaign, their support of the president has remained unwavering.

Paxton told Fox News Digital outside his final campaign event ahead of the March 3 primary that he believed Trump ‘did the right thing’ with Operation Epic Fury. When asked what voters were saying, he said, ‘No one wants foreign wars.’

‘But the reality is, when you’ve got a country that’s trying to build nuclear weapons, that is willing to use them, and that has demonstrated terrorist activity for decades, 40 or 50 years, you’ve got to deal with that, or eventually it comes to you,’ Paxton said.

Cornyn had a front-row view of Trump’s decision.

Chairman of the Joint Chiefs of Staff Gen. Dan ‘Raizin’ Caine said Tuesday during a press conference at the Pentagon that Trump gave the go-ahead to launch Operation Epic Fury while en route to Corpus Christi, Texas, to promote his energy agenda.

Cornyn and others from the Texas delegation were on Air Force One when Trump gave the order. When asked by Fox News Digital whether he was aware of the plan while traveling with the president, Cornyn said Trump was ‘a very cool customer.’

‘He asked us whether we supported a strike on Iran,’ Cornyn recalled. ‘The members of Congress who were there in the cabin of Air Force One all raised our hands and said we did support that, recognizing the gravity of the decision and that only the president, as commander in chief, could make it.’

In Washington, D.C., lawmakers are grappling with the decision, with members of both parties calling for a vote to limit Trump’s war powers in the region. Both Paxton and Cornyn said they are open to debate on the matter.

Cornyn argued it comes down to a simple choice.

‘I want to know who’s standing on the side of American peace and security, and who’s standing on the side of a nuclear-armed Iran,’ Cornyn said. ‘I think that’s the choice.’

How long the country remains involved in the operation remains an open question. Trump said in a video address that the U.S. would continue operations ‘until all of our objectives are achieved,’ but later suggested it could take ‘four weeks or less.’

Some Senate Democrats, including Sen. Andy Kim, D-N.J., argued the strike was ‘the same dangerous and foolish decision’ former President George W. Bush, a fellow Texan, made more than two decades ago in the Middle East.

‘I think the president is doing his best to get in and out. Bush was into nation-building, a very different approach to things. I do not think that’s Trump’s idea here or his endeavor,’ Paxton said. ‘I’m very confident that he’s going to do whatever he can to take them out, and he’s encouraging the people in Iran to take their country back.’

‘He’s not encouraging us to move in and help them do that,’ Paxton added. ‘We’re just taking out the bad guys, and then it’s up to them to build their country in a way that they see fit.’

Related Article

Bipartisan revolt targets Trump’s war powers after massive Iran strikes

A clip of former U.S. House Speaker Nancy Pelosi, D-Calif., has resurfaced online where she flatly defended the then-Obama administration’s decision to strike Libya — without the congressional authorization she believes President Donald Trump should have secured before conducting his own strikes over the weekend.

‘You’re saying that the president did not need authorization initially and still does not need any authorization from Congress on Libya?’ a reporter asked Pelosi at a press event back in 2011.

‘Yes,’ Pelosi answered plainly.

The unambiguous answer contrasts sharply with Pelosi’s view of Trump’s strikes against Iran on Saturday.

In a joint effort targeting Iranian military leadership, the U.S. and Israel killed Iranian Supreme Leader Ayatollah Ali Khamenei on Saturday, citing an imperative to halt Iran’s pursuit of developing a nuclear weapon.

Pelosi swiftly condemned the operation.

‘President Trump’s decision to initiate military hostilities into Iran starts another unnecessary war which endangers our servicemembers and destabilizes an already fragile region,’ Pelosi said in a post to X.

‘The Constitution is clear: decisions that lead our nation into war must be authorized by Congress.’

Pelosi, alongside other Democrats, is pursuing a war powers resolution that would limit Trump from taking further military action against Iran without express congressional approval.

Trump’s strikes bear similarity to President Barack Obama’s decision to strike Libya in 2011 under Operation Odyssey Dawn.

In that operation, Obama ordered a series of strikes against Libya in March 2011, looking to deter Muammar Gaddafi from attacking civilian protesters.

Gaddafi, known as the ‘Mad Dog of the Middle East,’ was the ruler of Libya from 1969 to 2011. He had a long and complicated relationship with the U.S. — at times aligning with national objectives and, at others, governing in a manner the U.S. couldn’t ignore.

The final straw came in the Libyan revolt of 2011, when demonstrations broke out in Benghazi and other cities. Like recent uprisings in Iran, Gaddafi met the threat to his rule with crushing force, marching his forces toward several Libyan cities that had resisted his power.

In what he described as attempts to uphold international law, Obama said the U.S., in partnership with the North Atlantic Treaty Organization (NATO), had taken the strikes to protect Libya’s civilians to protect Libya’s civilians.

‘We struck regime forces approaching Benghazi to save that city and the people within it,’ Obama said in remarks after the attacks.

The strikes did not kill Gaddafi.

Gaddafi was killed later that year at the hands of revolutionaries in October.

While Obama said he had consulted a bipartisan group of congressional lawmakers, he did not pursue a declaration of war before carrying out his strikes.

‘So, for those who doubted our capacity to carry out this operation, I want to be clear: The United States of America has done what we said we would do,’ Obama said.

Pelosi’s office did not respond to a request for comment on whether she saw any key differences between the attacks carried out by Obama and those now ordered by Trump.

Related Article

Massie-led push to handcuff Trump on Iran gets Jeffries’ backing

The U.S. Embassy in Riyadh was hit by two drones from Iran on Monday as Americans in Saudi Arabia were instructed to shelter in place. The embassy was empty at the time of the hits and no injuries were reported as a result of the attack.

On Tuesday, the embassy issued a security alert saying that the shelter in place order for Jeddah, Riyadh and Dhahran remained in effect, and it added that U.S. citizens throughout Saudi Arabia were advised to remain indoors. It also advised U.S. citizens to ‘avoid the embassy until further notice’ due to the attack.

‘We advise all U.S. citizens to maintain a personal safety plan. Crises can happen unexpectedly while traveling or living abroad, and a good plan helps you think through potential scenarios and determine in advance the best course of action,’ the embassy’s Tuesday alert read.

In the security alert, the embassy urged U.S. citizens to shelter in place, monitor its website for updates, enroll in the State Department’s Smart Traveler Enrollment Program (STEP), ensure their passports are valid for potential short-notice travel, remain aware of their surroundings, avoid demonstrations and large gatherings, follow local authorities’ instructions and monitor official information sources for the latest updates.

Secretary of State Marco Rubio in a video posted on X urged Americans in the Middle East to register with STEP, saying that it would allow them to see the latest safety and security guidance amid the ‘cowardly attacks’ from Iran.

Saudi Arabia’s Foreign Ministry released a statement condemning the attack, saying ‘the repetition of this cowardly and unjustified attack blatantly violates all international norms and laws, including the 1949 Geneva Convention and the 1961 Vienna Convention on Diplomatic Relations.’

‘The Kingdom emphasizes that the repetition of this flagrant Iranian behavior, which comes despite the Iranian authorities’ knowledge that the Kingdom has affirmed it will not allow its airspace or territory to be used to target Iran, will push the region toward further escalation,’ the foreign ministry’s statement read.

Iran has launched attacks in the region against Israel and several countries that have U.S. interests in retaliation for the U.S. and Israel’s joint military offensive known as Operation Epic Fury. Saudi Arabia condemned the retaliation on Feb. 28.

‘The Kingdom of Saudi Arabia expresses its rejection and condemnation in the strongest terms of the blatant and cowardly Iranian attacks that targeted the Riyadh Region and the Eastern Province, which were successfully intercepted,’ the Saudi Foreign Ministry’s Feb. 28 statement read. ‘These attacks cannot be justified under any pretext or in any way whatsoever, and they came despite the Iranian authorities’ knowledge that the Kingdom had affirmed it would not allow its airspace or territory to be used to target Iran.’

Amid the retaliatory strikes, the State Department has ordered the evacuation of non-emergency personnel and their families from Kuwait, Bahrain, Iraq, Qatar, Jordan and the United Arab Emirates.

Related Article

US casualties rise to 6 following Iranian retaliation for massive strikes

The State Department on Monday urged Americans to depart immediately from more than a dozen countries across the Middle East, warning of ‘serious safety risks’ as the Iran war intensifies.

Assistant Secretary of State for Consular Affairs Mora Namdar said U.S. citizens should leave from Bahrain, Egypt, Iran, Iraq, Israel, the West Bank and Gaza, Jordan, Kuwait, Lebanon, Oman, Qatar, Saudi Arabia, Syria, the United Arab Emirates and Yemen.

The department said Americans who need help arranging departure via commercial means can contact the State Department 24/7 at +1-202-501-4444 from abroad or +1-888-407-4747 from the U.S. and Canada.

The travel push was amplified by the State Department’s official travel account, which urged Americans abroad to enroll in the Smart Traveler Enrollment Program, or STEP, at step.state.gov to receive the latest security updates from their nearest U.S. embassy or consulate.

Officials have warned that conditions in the region remain volatile, and that security situations can change quickly as fighting tied to the Iran conflict continues.

The warnings come days after the United States launched Operation Epic Fury, striking command-and-control centers, Iranian air defense capabilities, missile and drone launch sites.

In a Feb. 28 Worldwide Caution security alert, the State Department said Americans worldwide, and especially those in the Middle East, should exercise increased caution, monitor local security alerts and expect potential travel disruptions, including periodic airspace closures.

The evacuation push follows a cascade of security alerts issued by U.S. embassies across the region since Saturday, many ordering or recommending Americans to shelter in place.

At least nine U.S. missions, including Bahrain, Iran, Kuwait, the United Arab Emirates, Saudi Arabia, Iraq, Jordan, Qatar and Israel, have issued repeated shelter-in-place directives or advisories over the past several days.

In multiple cases, embassy personnel and their families were ordered to remain at home, with Americans urged to stay in secure structures away from windows and be prepared for incoming missiles or drones.

In Saudi Arabia, the embassy in Riyadh closed Tuesday after two Iranian drones struck the building, prompting expanded shelter-in-place orders for Jeddah, Riyadh and Dhahran. No injuries were reported.

Related Article

Iran’s security chief accuses Trump of ‘Israel First’ policy, ‘delusional fantasies’ in region

New satellite images offer a stark look at the devastation inside Iran after U.S.-Israeli strikes, while also revealing the damage left behind by Tehran’s retaliatory attacks across the region.

According to U.S. Central Command, which oversees American military operations across the Middle East, U.S. forces struck more than 1,250 targets during the first two days of Operation Epic Fury.

Planet Labs satellite imagery captured burning ships and damaged facilities at the Konarak base in southern Iran, as well as significant destruction at Iran’s naval headquarters in Bandar Abbas on the Persian Gulf, reflecting the scale of the strikes on military infrastructure.

Imagery from Vantor shows the Choqa Balk drone facility in western Iran was hit, along with damage to other key military and strategic sites targeted in the U.S.–Israeli strike campaign.

Radar systems at the Zahedan air base in eastern Iran — near the country’s borders with Pakistan and Afghanistan — were also struck.

The two facilities are about 800 to 900 miles apart, underscoring the broad reach of the coordinated strikes.

Additionally, satellite imagery from Planet Labs shows thick smoke plumes rising above Tehran, signaling explosions and fires inside the Iranian capital.

The smoke underscores how the conflict has moved beyond isolated military sites and into the heart of Iran’s political center.

Iran responded with missile and drone strikes of its own, expanding the conflict across the region. Satellite images reveal damage to the port city of Sharjah in the United Arab Emirates. The city of Sharjah is the third most populous after Dubai and Abu Dhabi.

The Jebel Ali Port, the region’s largest maritime hub, was also targeted, underscoring how the retaliation extended beyond military sites to key infrastructure.

The U.S. has warned that further retaliation could follow, as both sides signal they are prepared for additional rounds of strikes. Pentagon officials said U.S. forces in the region remain on high alert and have publicly cautioned that any new attacks on U.S. citizens would prompt a forceful response.

With damage now visible from western Iran to the Persian Gulf, the coming days could determine whether the confrontation stabilizes — or spirals into a wider regional war.

Related Article

Fires rage at Iran’s Bandar Abbas naval headquarters, Strait of Hormuz traffic stalled

Blackrock Silver Corp. (TSXV: BRC,OTC:BKRRF) (OTCQX: BKRRF) (FSE: AHZ0) (‘Blackrock’ or the ‘Company’) is pleased to announce the issuance by the Nevada Department of Environmental Protection (NDEP), through the Bureau of Air Pollution Control, the Class II Air Quality and Surface Disturbance Permit (the ‘Permit’) for the Company’s Tonopah West mineral project (‘Tonopah West’) located along the Walker Lane Trend in Nye and Esmeralda Counties, Nevada, USA.

The Permit allows for the disturbance of up to 150 acres (60.7 Hectares) at Tonopah West with appropriate dust control measures and an ongoing program using the best practical methods to prevent particulate matter from becoming airborne. The term of the Permit is five (5) years, which can be extended and modified as Tonopah West moves toward permitting and construction of its proposed exploration decline, test mining and bulk sample extraction programs.

Data collection continues for the hydrogeological and geochemical programs that will form the basis for the Water Pollution Control Permit. Five humidity cells are in process to review acid generating potential of the waste and mineralized lithologies that will be encountered and transported to the surface during the tunneling and construction of the exploration decline including stockpiles for mineralized material mined as part of the bulk sample program.

The hydrogeological program is designed to understand the groundwater dynamics focused on potential flow and volumes to support required management and disposal as needed during the test mining and bulk sample phase of the program. Waste dump, stockpiles and portal entry engineering designs are on schedule and will be completed and used to calculate surface disturbance that will be the cornerstone for the Modification to the Nevada Reclamation Permit. The permitting process is on schedule with all permits anticipated by mid-2027. Once all permits are in hand, the Company will decide when to commence with the exploration decline, test mining and bulk sample extraction programs at Tonopah West.

Qualified Persons

Blackrock’s exploration activities at Tonopah West are conducted and supervised by Mr. William Howald, Executive Chairman of Blackrock. Mr. William Howald, AIPG Certified Professional Geologist #11041, is a Qualified Person as defined under National Instrument 43-101 – Standards of Disclosure for Mineral Projects. He has reviewed and approved the contents of this news release.

About Blackrock Silver Corp.

Blackrock Silver Corp. is an American-focused emerging primary silver developer systematically advancing the high-grade Tonopah West Project, situated in the historic ‘Queen of the Silver Camps’ in a jurisdiction consistently ranked as one of the top mining regions globally. The Company is backstopped by a veteran board and technical team with a proven track record of discovering, financing, and building major precious metal mines in Nevada and globally. Blackrock is committed to establishing a secure, high-margin, domestic supply of silver and gold.

Additional information on Blackrock Silver Corp. can be found on its website at www.blackrocksilver.com and by reviewing its profile on SEDAR+ at www.sedarplus.ca.

Cautionary Note Regarding Forward-Looking Statements and Information

This news release contains ‘forward-looking statements’ and ‘forward-looking information’ (collectively, ‘forward-looking statements‘) within the meaning of Canadian and United States securities legislation, including the United States Private Securities Litigation Reform Act of 1995. All statements, other than statements of historical fact, are forward-looking statements. Forward-looking statements in this news release relate to, among other things: the Company’s strategic plans; the Company’s permitting initiatives at Tonopah West, including the anticipated receipt of all permits by mid-2027; the proposed commencement of an exploration decline, test mining and bulk sample extraction programs at Tonopah West; the Company’s de-risking initiatives at Tonopah West; estimates of mineral resource quantities and qualities; estimates of mineralization from drilling; geological information projected from sampling results; and the potential quantities and grades of the target zones.

These forward-looking statements reflect the Company’s current views with respect to future events and are necessarily based upon a number of assumptions that, while considered reasonable by the Company, are inherently subject to significant operational, business, economic and regulatory uncertainties and contingencies. These assumptions include, among other things: conditions in general economic and financial markets; accuracy of assay results; geological interpretations from drilling results, timing and amount of capital expenditures; performance of available laboratory and other related services; future operating costs; the historical basis for current estimates of potential quantities and grades of target zones; the availability of skilled labour and no labour related disruptions at any of the Company’s operations; no unplanned delays or interruptions in scheduled activities; all necessary permits, licenses and regulatory approvals for operations are received in a timely manner; the ability to secure and maintain title and ownership to properties and the surface rights necessary for operations; and the Company’s ability to comply with environmental, health and safety laws. The foregoing list of assumptions is not exhaustive.

The Company cautions the reader that forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause actual results and developments to differ materially from those expressed or implied by such forward-looking statements contained in this news release and the Company has made assumptions and estimates based on or related to many of these factors. Such factors include, without limitation: the timing and content of work programs; results of exploration activities and development of mineral properties; the interpretation and uncertainties of drilling results and other geological data; receipt, maintenance and security of permits and mineral property titles; environmental and other regulatory risks; project costs overruns or unanticipated costs and expenses; availability of funds; failure to delineate potential quantities and grades of the target zones based on historical data; general market and industry conditions; and those factors identified under the caption ‘Risks Factors’ in the Company’s most recent Annual Information Form.

Forward-looking statements are based on the expectations and opinions of the Company’s management on the date the statements are made. The assumptions used in the preparation of such statements, although considered reasonable at the time of preparation, may prove to be imprecise and, as such, readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date the statements were made. The Company undertakes no obligation to update or revise any forward-looking statements included in this news release if these beliefs, estimates and opinions or other circumstances should change, except as otherwise required by applicable law.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

For Further Information, Contact:

Andrew Pollard President and Chief Executive Officer (604) 817-6044 info@blackrocksilver.com

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/286059