LaFleur Minerals Inc. (CSE: LFLR,OTC:LFLRF) (OTCQB: LFLRF) (FSE: 3WK0) (‘LaFleur Minerals’ or the ‘Company’) is pleased to provide an update on the advancement of its Beacon Gold Mill restart plans, further to the Company’s press release dated January 26, 2026, which outlined its near-term production strategy and the ongoing advancement of its comprehensive Preliminary Economic Assessment (‘PEA’). The Company’s assets, the Swanson Gold Deposit and Beacon Gold Mill, lie in the heart of the Val-d’Or, Québec mining camp, on the prolific Abitibi Greenstone Belt, Canada’s largest gold producing region.

Valley of Gold, Val-d’Or, Québec

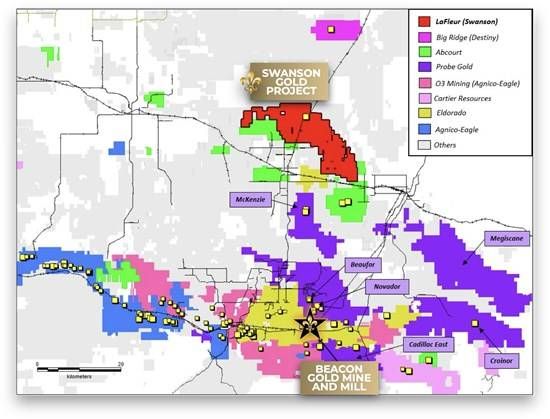

The Val-d’Or/Rouyn-Noranda mining camp is a premier gold mining hub within the Abitibi Greenstone Belt of Québec with over 73 million ounces of gold produced from 1926 to 2019 (source: DigiGeoData). The Val-d’Or mining district, known as the ‘Valley of Gold,’ is characterized by Archean greenstone-hosted orogenic gold deposits typically found in quartz-tourmaline-carbonate veins. The Lamaque Complex is located in Val-d’Or and operated by Eldorado Gold Inc. Commercial production was declared at the Triangle mine on March 31, 2019, and has since produced over 1 Moz of gold (source: Eldorado Gold website). The Lamaque Complex deposits are located within the prolific Val-d’Or district that hosts the historical Lamaque and Sigma Mines. Collectively, these mines produced nearly 9.5 million ounces of gold between 1937 and 2012 (source: Cowen, E.J, 2020. Miner Deposita 55, p217-240). The region is host to numerous other gold deposits or exploration stage projects that surround LaFleur Minerals’ 100%-owned Beacon Gold Mill (Figure 1). Please note that mineralization on these adjacent properties is not necessarily indicative of mineralization on the Company’s properties.

Figure 1: Regional View of LaFleur’s Beacon Gold Mill and Swanson Gold Project

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/6526/284272_8c1565e204f76b48_001full.jpg

LaFleur Minerals: Restarting Gold Production at 100%-Owned Mill in the Valley of Gold

LaFleur’s Minerals Beacon Gold Mill, Swanson Gold Deposit, and Beacon Tailings Pond are situated centrally within the prolific southern Abitibi Greenstone Belt. The Beacon Gold Mill, located in the heart of this mining camp, underwent more than $20 million in recent upgrades and modernization prior to its most recent gold production in 2022, when gold prices were approximately $2,000 per ounce. Today, with gold prices significantly higher, breaking above $4,900 per ounce, the Company believes that the strategic value of owning the fully permitted Beacon Gold Mill, Tailings Pond, and related infrastructure within such a prolific gold district provides a compelling foundation for near-term gold production and long-term district-scale growth.

Beacon Mill Restart Progress

Refurbishment and site upgrade activities are progressing well. As of today, work continues to advance steadily across critical plant systems, with several major components now refurbished or nearing operational readiness.

Electrical upgrades and winterization improvements have largely been completed, helping ensure reliable year-round operations. On the mechanical side, numerous pumps, material handling systems, and key processing components have been inspected, repaired, and prepared for restart. Structural integrity inspections have confirmed the plant remains in good condition. Modern safety upgrades, including hydroelectric, fire protection, and enhanced security surveillance, are now in place.

To date, approximately 30% of the total budget has been spent on the project, which remains firmly under cost control, with substantial physical progress achieved while maintaining strong financial flexibility.

These initiatives represent important milestones as the Company prepares for re-commissioning and the mill’s restart, anchored by a vertically-integrated mine-to-mill portfolio that includes the Company’s Swanson Gold Deposit, just 60 kilometres from the Beacon Gold Mill, the Beacon Gold Mill and Tailings Pond. LaFleur Minerals’ strategy focuses on combining resource development at the Swanson Gold Deposit with the permitted Beacon Gold Mill to accelerate the pathway to production.

Figure 2: LaFleur’s Beacon Gold Mill

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/6526/284272_8c1565e204f76b48_002full.jpg

Figure 3: Inside LaFleur’s Beacon Gold Mill

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/6526/284272_8c1565e204f76b48_003full.jpg

Figure 4: Inside LaFleur’s Beacon Gold Mill

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/6526/284272_8c1565e204f76b48_004full.jpg

Figure 5: Inside LaFleur’s Beacon Gold Mill, Agitator

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/6526/284272_8c1565e204f76b48_005full.jpg

Swanson Gold Continues to Deliver Results

Swanson Gold Deposit’s recent drill campaign has validated strong gold continuity, long mineralized intercepts including a standout intercept of 2.05 g/t Au over 158.25 metres (Hole SW-25-066), narrow high-grade results including 121.0 g/t Au over 1.1 metres and new shallow discoveries beyond the current Swanson Deposit footprint, reinforcing Swanson’s potential as a scalable, district-scale gold asset and long-term source of mill feed for the Company’s nearby Beacon Gold Mill (refer to press release dated February 4, 2026).

Paul Ténière, Chief Executive Officer of LaFleur Minerals Inc., commented, ‘LaFleur Minerals has assembled what we believe is a technically differentiated and strategically rare asset base for a company at our stage of development. After only ~18 months of listing on the CSE, we control a district-scale exploration project at the Swanson Gold Deposit as potential primary feed source, the Beacon Tailings Pond, and fully permitted processing infrastructure, the Beacon Gold Mill. It is highly uncommon for emerging resource companies to simultaneously hold a large-scale exploration land package and access to owned milling infrastructure, particularly this early in their corporate lifecycle. LaFleur Minerals is advancing its PEA in parallel with the refurbishment of an existing processing facility, materially compressing the timeline between resource delineation and potential production. As our PEA approaches completion, targeted for March 2026, and as we prepare for pre-operational tests and system checks at the Beacon Gold Mill in the coming months, we are transitioning from pure exploration and development to gold production execution, positioning LaFleur Minerals as a near-term production story supported by tangible infrastructure and a district-scale growth platform.’

The Company’s impending PEA will provide updated economic metrics and a development roadmap aligned with its near-term production objectives. Concurrently, mill refurbishment activities remain on schedule, positioning LaFleur for operational readiness as market conditions remain favourable. With gold prices now exceeding $4,900 per ounce, the strategic value of controlling both feed and processing capacity becomes even more significant. LaFleur Minerals’ integrated asset portfolio provides optionality, capital efficiency, and operational leverage to gold price appreciation.

Further updates will be provided as key milestones are achieved.

Figure 6: LaFleur’s Swanson Gold Project, Drilling

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/6526/284272_8c1565e204f76b48_006full.jpg

QUALIFIED PERSON STATEMENT AND DATA VERIFICATION

All scientific and technical information in this news release has been prepared and approved by Louis Martin, P.Geo. (OGQ), Exploration Manager and Technical Advisor of the Company and considered a Qualified Person (QP) for the purposes of NI 43-101.

About LaFleur Minerals Inc.

LaFleur Minerals Inc. (CSE: LFLR,OTC:LFLRF) (OTCQB: LFLRF) (FSE: 3WK0) is focused on the development of district-scale gold projects in the Abitibi Gold Belt near Val-d’Or, Québec. The Company’s mission is to advance mining projects with a laser focus on our resource-stage Swanson Gold Project and the Beacon Gold Mill, which have significant potential to deliver long-term value. The Swanson Gold Project is approximately 18,304 hectares (183 km2) in size and includes several prospects rich in gold and critical metals previously held by Monarch Mining, Abcourt Mines, and Globex Mining. LaFleur has recently consolidated a large land package along a major structural break that hosts the Swanson, Bartec, and Jolin gold deposits and several other showings which make up the Swanson Gold Project. The Swanson Gold Project is easily accessible by road allowing direct access to several nearby gold mills, further enhancing its development potential. LaFleur Minerals’ fully-permitted and refurbished Beacon Gold Mill is capable of processing over 750 tonnes per day and is being considered for processing mineralized material from Swanson and for custom milling operations for other nearby gold projects.

ON BEHALF OF LaFleur Minerals INC.

Paul Ténière, M.Sc., P.Geo.

Chief Executive Officer

E: info@lafleurminerals.com

LaFleur Minerals Inc.

1500-1055 West Georgia Street

Vancouver, BC V6E 4N7

Website: www.lafleurminerals.com | LinkedIn | Twitter/X | Instagram

Neither the Canadian Securities Exchange nor its Regulation Services Provider accepts responsibility for the adequacy or accuracy of this news release.

Cautionary Statement Regarding ‘Forward-Looking’ Information

This news release includes certain statements that may be deemed ‘forward-looking statements’. All statements in this new release, other than statements of historical facts, that address events or developments that the Company expects to occur, are forward-looking statements. Forward-looking statements are statements that are not historical facts and are generally, but not always, identified by the words ‘expects’, ‘plans’, ‘anticipates’, ‘believes’, ‘intends’, ‘estimates’, ‘projects’, ‘potential’ and similar expressions, or that events or conditions ‘will’, ‘would’, ‘may’, ‘could’ or ‘should’ occur. Forward-looking statements in this news release include, without limitation, statements related to the use of proceeds from the Offering. Although the Company believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results may differ materially from those in the forward-looking statements. Factors that could cause the actual results to differ materially from those in forward-looking statements include market prices, continued availability of capital and financing, and general economic, market or business conditions. Investors are cautioned that any such statements are not guarantees of future performance and actual results or developments may differ materially from those projected in the forward-looking statements. Forward-looking statements are based on the beliefs, estimates and opinions of the Company’s management on the date the statements are made. Except as required by applicable securities laws, the Company undertakes no obligation to update these forward-looking statements in the event that management’s beliefs, estimates or opinions, or other factors, should change.

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/284272