Quebec Innovative Materials Corp. (CSE: QIMC) (OTCQB: QIMCF) (FSE: 7FJ) (‘QIMC’ or the ‘Company’) today announced the completion of Discovery Hole DDH-26-01 to a depth of 711 metres at its West-Advocate hydrogen project in Nova Scotia. Drilling intersected a persistent hydrogen-bearing system beginning at approximately 505 metres, where visible gas was observed at the drill head and well water returned headspace hydrogen concentrations that exceeded the detection limits of the Company’s GA5000 gas analyser. Hydrogen concentrations remained elevated to the end of the hole, confirming that the system remains open at depth as drilling advances, with Hole 2 targeting structural zones to the north-west.

Borehole DDH-26-01 has returned hydrogen concentrations so elevated that the Company’s field instruments were pushed beyond their maximum detectable range on multiple separate depth intervals. These readings were obtained from wellhead water samples already subject to dilution factors of 100 to 10,000 times, according to independent analysis by Prof. Marc Richer-LaFlèche of the Institut National de la Recherche Scientifique (INRS), Québec. The surface headspace gas measurements, extraordinary in their own right, are a fraction of what the fractured geological formation is holding at depth.

This is not a trace detection. This is not background noise. This is a live, pressurised, hydrogen-generating system, confirmed by instrument, confirmed by water geochemistry, and confirmed visually in the field, whose true magnitude current surface instrumentation cannot fully characterise.

Why This Discovery at Depth Matters

Natural hydrogen, increasingly referred to as ‘gold hydrogen’ by the global energy community, is one of the most transformative emerging resource categories of this decade. It is carbon-free, generated naturally within the Earth’s crust, and requires no energy-intensive manufacturing process. The global race to identify and develop commercially viable natural hydrogen deposits is intensifying rapidly. QIMC’s West-Advocate results, independently validated by one of Canada’s foremost geochemical institutions, position the Company as one of the most scientifically rigorous natural hydrogen exploration programmes in North America.

Hole 2 Drilling Underway

Hole 2 of the West-Advocate 2026 drilling program is currently underway and is targeting structural zones similar to those observed in DDH-26-01 borehole and identified from geophysical and soil-gas hydrogen and radon geochemistry. The hole is oriented to the northwest in order to approach the contact zone between a gravity and magnetic high interpreted as an uplift of the bedrock sub-basement and the carboniferous sedimentary rock basin. Gas monitoring, well water sampling and core logging remain active as drilling progresses.

Sampling Methodology

Water sampling was conducted at the top of borehole DDH-26-01 casing and gas analyses were carried out using standard headspace gas measurements (2-L) at room temperature and pressure and using 1,300 mL of water and 700 mL of air. Sampling for headspace gas, ranged from depths of 368 m to 710 m, and was conducted between February 25 and March 5, 2026.

Hydrogen Results

At 638 metres, gas bubbles were physically observed rising from the drill head – direct visual confirmation of free hydrogen escaping the formation at the moment of intersection. This field observation is among the most unambiguous forms of evidence available to an exploration team: gas under sufficient pressure to physically exsolve and migrate upward through the drill column in real time.

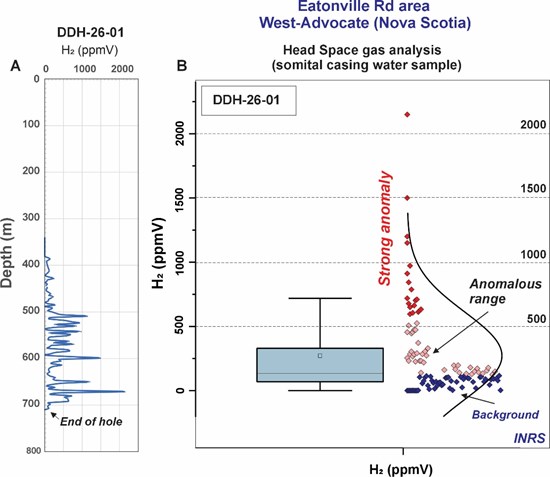

From 505 m to 680 m, a sustained zone of significantly elevated hydrogen concentrations was identified. Within this interval, on multiple separate occasions, hydrogen concentrations exceeded the maximum detectable range of the GA5000 gas analyzer entirely, logged simply as instrument maximum exceedance. Where exceedance was recorded, samples were subsequently reanalysed using a second independent Eagle-2 H₂ gas detector, confirming concentrations of 2,150 ppmV in diluted wellhead water – itself already subject to dilution factors of 100 to 10,000 times relative to true formation concentrations at depth. The 2,150 ppmV is not the peak. It is the confirmed minimum floor of what was measured at surface. The true deep well water concentration above it remains open.

From 683 m to 711 m, the deepest section drilled in hole DDH-26-01, the hydrogen system did not fade. Sustained readings of 525, 612, 623, 633, and 962 ppmV in diluted wellhead water were recorded in successive intervals, confirming that even at the furthest extent of the borehole, the system remains active, consistent, and measurable.

Throughout the entire sampled interval from 368 m to 710 m, methane (CH₄) was recorded at concentrations below the limit of detection of the GA5000 instrument in 97.3% of all samples. The statistical correlation between H₂ and CH₄ concentrations across the full dataset is R² = 0.06, confirming that hydrogen and methane are uncorrelated and that the gas system is purely hydrogen-dominant with no thermogenic hydrocarbon association.

Hydrogen concentrations are equally uncorrelated with CO₂ (R² = 0.009), with 97.3% of samples showing CO₂ at only 0.1% by volume. The combined absence of methane, the extremely low CO₂ levels, and the dominance of H₂ across both drilling and previously conducted soil-gas surveys confirm a pure inorganic hydrogen source – not a petroleum leakage, not a biodegradation plume, and not a thermogenic system of any kind.

The Dilution Factor

Investors and analysts reviewing the surface measurements should understand the hydrodynamic context that makes them truly extraordinary. Due to the operational constraints of diamond drilling, water samples are collected at the wellhead outlet, not at depth. For example, for borehole DDH-26-01 at 725 m depth, the internal water volume is approximately 717 imperial gallons. With a surface pumping rate of 13.5 gallons per minute, the residence time of water within the borehole is on the order of 54 minutes, resulting in substantial dilution of any gases present in the formation before samples reach surface.

Furthermore, as Prof. Richer-LaFlèche’s analysis establishes, if a gas leak occurs along a porous interval within a deep fracture zone approximately 2 metres thick, the contact time between circulating water and the fractured zone is only approximately 9 seconds. Under such highly hydrodynamic conditions, hydrogen concentrations measured in headspace samples collected at the wellhead are expected to be strongly diluted compared with samples obtained directly at depth under static or near-static conditions.

The result, as independently established by INRS, is that dilution factors of 10² to 10⁴ – that is, 100 to 10,000 times – are expected at this borehole. The confirmed 2,150 ppmV in diluted headspace water measurement represents a very diluted fraction of the true hydrogen concentrations coming out of faulted zones at depth.

Applying the lower bound of Prof. Richer-LaFlèche’s dilution range alone, true in-situ deep well concentrations in the fault zone could exceed 215,000 ppmV which is near 21.5%V H2 (headspace gas measurements). At dilution ratios approaching 465×, the theoretical formation concentration would approach hydrogen saturation (~100% by volume). This modelling illustrates the magnitude of dilution occurring during circulation drilling and why surface measurements represent only a fraction of the hydrogen present at depth.

Why the Dilution Model Matters

Surface hydrogen measurements collected during active drilling represent only a diluted fraction of the hydrogen entering the borehole from hydrogen-bearing fracture zones at depth. During diamond drilling, circulating drilling fluids and subsurface fluids move continuously through the borehole before reaching surface sampling points. This process introduces significant hydrodynamic mixing and dilution within a large water column prior to measurement.

For borehole DDH-26-01, the internal borehole water volume and circulation rates indicate that hydrogen measured at the wellhead is subject to dilution factors estimated by INRS to range from approximately 10² to 10⁴ (100× to 10,000×). As a result, surface headspace measurements represent only a small portion of the hydrogen actually entering the borehole from fractured zones at depth.

Applying the lower bound of this dilution range to the confirmed 2,150 ppmV surface measurement implies potential in-situ formation concentrations exceeding approximately 215,000 ppmV (≈21.5% hydrogen by volume). Higher dilution ratios would imply proportionally higher formation concentrations. These calculations illustrate the scale of dilution occurring within the circulating borehole system and demonstrate why surface measurements cannot directly represent the full hydrogen concentration present in the subsurface.

Equally important, hydrogen remained repeatedly measurable at surface despite this dilution, borehole circulation, and transport to surface. The persistence of hydrogen readings across a broad depth interval therefore supports the interpretation that DDH-26-01 intersected an active hydrogen-bearing fracture system rather than a small isolated gas occurrence.

‘I want to be precise with the market about what we have found and what the instruments told us,’ stated John Karagiannidis, CEO of QIMC. ‘On multiple separate depth intervals, our GA5000 field instruments were pushed past their maximum detection ceiling entirely – the instruments had no higher reading to give us. When we reanalysed those samples with a second independent Eagle-2 detector, we confirmed concentrations exceeding instrument detection thresholds in diluted wellhead water – water that Prof. Richer-LaFlèche has established carries a dilution factor of 100 to 10,000 times relative to what the formation holds at depth. Every single methane reading across the entire hole came back zero. This is a hydrogen system whose true magnitude our instruments could not fully measure at surface. The data from DDH-26-01 has not set a ceiling for this project. It has set a floor. Hole 2 is underway and we are going deeper.’

INRS Analysis by Prof. Marc Richer-LaFlèche

The complete gas geochemistry dataset (headspace analysis of well water samples) and drill core from DDH-26-01 have been submitted to and independently analysed by Prof. Marc Richer-LaFlèche of the Institut National de la Recherche Scientifique (INRS), Québec. Prof. Richer-LaFlèche worked on the Reactivated Rift and Graben Geostructure (R2G2) exploration model that underpins QIMC’s targeting methodology, and is serving as independent third-party scientific analyst for the West-Advocate 2026 programme.

In his assessment, Prof. Richer-LaFlèche states:

*’Drilling DDH-26-01 represents a major milestone for natural hydrogen exploration in Nova Scotia, and particularly for the greater Advocate (Cumberland) area. Analytical results from this borehole clearly demonstrate that secondary faults act as conduits for natural hydrogen circulation and its transfer toward the subsurface. These findings validate the exploration model applied by QIMC and its collaborators for targeting natural hydrogen along the Cobequid-Minas Fault Zone (CMFZ) deformation corridor.’*

Prof. Richer-LaFlèche further notes that the near-absence of methane across all sampled intervals:

*’…is a pattern consistent with our working hypothesis that hydrogen production in the area is primarily related to radiolytic processes and/or water-rock reactions involving iron-rich geological materials. This observation is significant because methane was also absent from the soil-gas surveys conducted in the West-Advocate area. The convergence of these two independent datasets reinforces the interpretation that hydrogen circulating within the local rock mass may accumulate locally, offering the potential for clean hydrogen resources without the co-production of methane or other greenhouse gases.’*

Figure 1. Diagrams illustrating the variations in measured hydrogen concentrations (ppmV) in head-space gas samples obtained from water exiting the DDH-26-01 borehole casing. A) Vertical distribution of hydrogen concentrations as a function of depth along the 55°-inclined borehole. B) Statistical variability of the dataset and identification of background noise, anomalous samples, and strongly anomalous samples based on a normal probability plot derived from the head-space gas analyses performed on water samples from DDH-26-01.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/7968/287951_4f6b9922a4bb5a1b_001full.jpg

Technical Interpretation – What These Results Suggest

The persistence of hydrogen concentrations toward the bottom of the borehole, combined with visible gas observations and instrument exceedances, suggests the drill hole intersected an active hydrogen migration corridor rather than an isolated gas occurrence.

The Data – Interval by Interval

Multiple intervals between approximately 500 m and 680 m returned hydrogen readings exceeding the GA5000 instrument detection limits. Independent verification using an Eagle-2 detector confirmed hydrogen concentrations exceeding 2,150 ppmV in diluted wellhead samples. Sustained hydrogen readings continued from 683 m to 711 m depth.

Geology Confirms the System

Drill cores recovered from approximately 570 m to 680 m depth present a lithological character that is both visually compelling and geologically coherent with the gas data. Dark carbonaceous and graphitic black rock alternates with lighter siltstones. The abundant fracturing and veining observed throughout the core indicates active structural pathways through which hydrogen-bearing fluids migrate and accumulate.

The geology did not change. The drill did not stop. The system did not weaken.

Next Steps

Drilling continues with Hole 2 targeting deeper portions of the interpreted structural system. Additional borehole sampling, gas geochemistry analysis and isotopic studies are ongoing in collaboration with researchers from INRS.

For More Information, Please Contact:

REGULATORY DISCLAIMER

Neither the Canadian Securities Exchange nor its Regulation Services Provider accepts responsibility for the adequacy or accuracy of this release. This press release contains forward-looking statements based on current expectations, field observations, and preliminary data. Actual results may differ materially. All gas readings and geological interpretations are preliminary and subject to further independent verification and analysis. Instrument maximum exceedance readings indicate hydrogen concentrations beyond the GA5000’s upper detection threshold; the confirmed surface measurement of 2,150 ppmV was independently verified using an Eagle-2 H₂ gas detector from diluted wellhead water samples. Dilution factor estimates of 10² to 10⁴ are based on borehole hydrodynamic modelling by Prof. Richer-Lafleche of INRS and represent a range of expected values; true in-situ formation concentrations are undetermined pending further analysis. Projected in-situ concentration ranges derived from dilution factor modelling are illustrative estimates only and do not represent confirmed or measured formation concentrations. This release does not constitute an offer of securities or investment advice. Investors are urged to conduct their own due diligence.

Forward-Looking Statements

This press release contains ‘forward-looking statements’ and ‘forward-looking information’ within the meaning of applicable Canadian securities legislation. These statements are based on expectations, estimates, and projections as of the date of this press release and involve known and unknown risks, uncertainties, and other factors that may cause actual results, performance, or achievements of the Company to differ materially from those expressed or implied.

Forward-looking statements are generally identified by words such as ‘expects,’ ‘anticipates,’ ‘believes,’ ‘intends,’ ‘estimates,’ ‘projects,’ ‘potential,’ and similar expressions, or by statements that events or conditions ‘will,’ ‘may,’ ‘could,’ or ‘should’ occur.

Although the Company believes that the forward-looking information contained herein is reasonable as of the date of this press release, such information is subject to change and no assurance can be given that future results will be achieved. The Company undertakes no obligation to update forward-looking statements except as required by applicable law.

Source

This post appeared first on investingnews.com