PERTH, AUSTRALIA AND VANCOUVER, BC / ACCESS Newswire / February 16, 2026 / Sarama Resources Ltd. (‘Sarama‘ or the ‘Company‘) (ASX:SRR)(TSXV:SWA) is pleased to announce it has appointed Davidson & Company LLP (‘Davidson & Co’) as Sarama’s audit firm, effective 13 February 2026.

Davidson & Co was appointed following the receipt by Sarama of the resignation of HLB Mann Judd, effective 10 February 2026. The Audit Committee of the Board of Directors accepted the resignation of HLB Mann Judd and recommended the appointment of Davidson & Co. The Board of Directors of Sarama, on the recommendation of the Audit Committee, appointed Davidson & Co as the new auditor until the next Annual General Meeting of Sarama.

Sarama sent a Notice of Change of Auditor (the ‘Notice‘) to HLB Mann Judd and to Davidson & Co and has received a letter from each, addressed to the securities commissions in each jurisdiction where Sarama is reporting, stating that they agree with the information contained in the Notice. The Notice and letters (the ‘Change of Auditor Package‘) have been reviewed and approved by Sarama’s Audit Committee and the Board of Directors.

The Change of Auditor Package is available under Sarama’s SEDAR+ profile at www.sedarplus.ca.

This announcement was authorised for release to the ASX by the Board of Sarama Resources Ltd.

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Surface Metals Inc. (CSE: SUR,OTC:SURMF) (OTCQB: SURMF) (the ‘Company’, or ‘Surface Metals’) is pleased to announce it has engaged Danayi Capital Corp. (‘Danayi’), a full service marketing firm based out of Vancouver, BC, to provide digital marketing services for a 6-month term commencing on February 16, 2026. Under the terms of the agreement between Surface Metals and Danayi, the Company has agreed to pay Danayi one hundred and fifty thousand USD. No compensation in securities of the Company will be paid to Danayi. Danayi Capital Corp., an arm’s length party, is owned by Mehran Bagherzadeh. Based at 550 – 800 West Pender Street, Vancouver, BC, V6C 2V6 (e-mail: mehran@danayi.co; tel: 604-767-2983), Danayi specializes in marketing, advertising and public awareness within the mining and metals sector. To the knowledge of the Company, Danayi does not own any securities of the Company.

About Surface Metals Inc.

Surface Metals Inc. (CSE: SUR,OTC:SURMF) (OTCQB: SURMF) is a North American mineral exploration company focused on advancing a diversified portfolio of gold and lithium projects in Nevada, USA. The Company’s Cimarron Gold Project is located in Nye County, Nevada, in a historically productive gold district. Surface’s Clayton Valley Lithium Brine Project hosts an inferred resource of approximately 302,900 tonnes LCE adjacent to Albemarle’s Silver Peak Mine. Surface Metals is also advancing a sedimentary claystone lithium project in Fish Lake Valley, Nevada.

For more information, please visit: www.surfacemetals.com

On behalf of the Board of Directors Steve Hanson Chief Executive Officer, President, and Director Telephone: (604) 564-9045 info@surfacemetals.com

Neither the CSE nor its regulations service providers accept responsibility for the adequacy or accuracy of this news release. This news release contains certain statements which may constitute forward-looking information within the meaning of applicable securities laws (‘forward-looking statements’). These include statements regarding the amount of funds to be raised under the Offering, and the use of such funds. There is no guarantee the Offering will be completed on the terms outlined above, or at all. Use of funds is subject to the discretion of the Company’s board of directors, and as such may be used for purposes other than as set out above. Any forward-looking statement speaks only as of the date it is made and, except as may be required by applicable securities laws, the Company disclaims any intent or obligation to update any forward-looking statement, whether as a result of new information, future events or results or otherwise.

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/283975

U.S. Secretary of State Marco Rubio signed a civil nuclear cooperation agreement involving the U.S. and Hungary on Monday.

During remarks at the signing ceremony, Rubio indicated that the U.S.-Hungary relationship, and the relationship between President Donald Trump and Hungarian Prime Minister Viktor Orbán, is very close.

The American diplomat described the relationship between the two nations as being ‘as close as I can possibly imagine it being.’

Rubio, during remarks delivered alongside Orbán, asserted, ‘Your success is our success.’

He noted that if Hungary ever faces financial problems, impediments to growth or threats to national stability, he knows ‘President Trump will be very interested’ in ‘finding ways’ to help.

Trump has praised Orbán and backed him for re-election.

‘Highly Respected Prime Minister of Hungary, Viktor Orbán, is a truly strong and powerful Leader, with a proven track record of delivering phenomenal results. He fights tirelessly for, and loves, his Great Country and People, just like I do for the United States of America. Viktor works hard to Protect Hungary, Grow the Economy, Create Jobs, Promote Trade, Stop Illegal Immigration, and Ensure LAW AND ORDER!’ Trump declared on Truth Social this month.

‘Relations between Hungary and the United States have reached new heights of cooperation and spectacular achievement under my Administration, thanks largely to Prime Minister Orbán. I look forward to continuing working closely with him so that both of our Countries can further advance this tremendous path to SUCCESS and cooperation. I was proud to ENDORSE Viktor for Re-Election in 2022, and am honored to do so again. Viktor Orbán is a true friend, fighter, and WINNER, and has my Complete and Total Endorsement for Re-Election as Prime Minister of Hungary — HE WILL NEVER LET THE GREAT PEOPLE OF HUNGARY DOWN!’ Trump added.

Americans aren’t happy with their economy. In October, Pew Research reported that “26 percent now say economic conditions are excellent or good, while 74 percent say they are only fair or poor.” This weighs heavily on their minds. In December, Gallup reported 35 percent of Americans “naming any economic issue” as “the most important problem facing this country today,” up from 24 percent in October.

Together, this is a significant headwind for Republicans entering an election year. But, for whatever it’s worth, it could be worse. Indeed, the average American’s economic conditions would be worse in most of the developed world.

“I Once Thought Europeans Lived as Well as Americans,” economist Tyler Cowen wrote in the Free Press last year; “Not Anymore.”

“I went to live in Germany as a student in 1984, and I marveled at how many things were better there than in the United States,” Cowen writes. “Now, 40 years later, I’ve massively revised my original judgments. I go to Europe at least twice a year, and have been to almost every country there. More and more I look to it for its history — not for its living standards.”

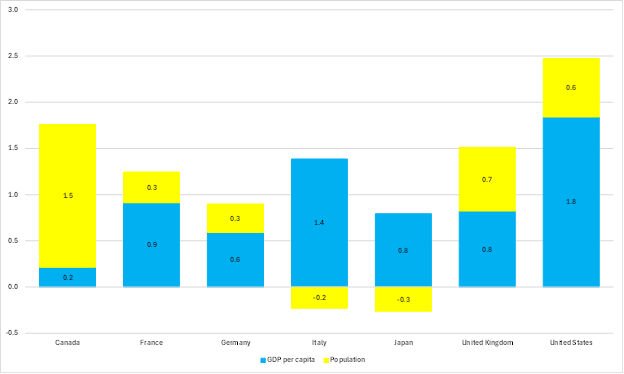

Total vs Per Capita GDP Growth

“In terms of per capita income,” Cowen notes, “America has opened up a big and apparently growing lead over West Europe.”

Indeed, over the last ten years, real Gross Domestic Product (GDP) growth has averaged 2.5 percent annually in the United States. This is the best performance among the G7 nations, ranking well ahead of Canada, in second place, with 1.8 percent, and Italy in third, with 1.2 percent, less than half the US rate (Figure 1).

Figure 1: Average annual real GDP growth, 2014-2015 to 2023-2024 (PPP, constant 2021 international $)

World Bank World Development Indicators

But when discussing economic growth, one should always be clear whether they are discussing total GDP, given above, or per capita GDP, as Cowen is, which is what matters most for living standards. If we subtract the average annual growth rate of the population from the average annual growth rate of real total GDP, we are left with the average annual growth rate of real GDP per capita (Figure 2).

The numbers for per capita GDP growth tell a very different story. The United States is still top of the G7 with an average real per capita GDP growth rate of 1.8 percent annually. But Canada slumps from second to bottom. Fully 1.5 percentage points — 88 percent — of its 1.8 percent average annual growth in total GDP can be attributed to increases in the population. Despite impressive total GDP growth, the average Canadian has become little better off. Italy, by contrast, rises from third to second. While its population declined at an average annual rate of 0.2 percent — the second worst performance — its per capita GDP grew at an average rate of 1.4 percent annually.

Figure 2: Components of annual real GDP growth, 2014-2015 to 2023-2024, percentage points

World Bank World Development Indicators

Immigration and Economic Growth

There is no strong relationship here between population growth and real per capita GDP growth. Indeed, many of those who propose increased immigration as the path to faster GDP growth are talking about faster total GDP growth — the dismal Canadian model — rather than faster per capita GDP growth. When it is not clear whether someone is opining on total GDP or per capita GDP, they should be pressed for clarification.

Whether or not immigration boosts per capita GDP growth depends on two things. First, are the immigrants, on average, more or less likely than the population currently resident to be employed? Second, are the immigrants, on average, more or less skilled than the population currently resident? Consider that GDP per capita is just GDP / Population.

If the answer to both of these questions is “more,” then the immigrants add more to the numerator (GDP) than the denominator (population), and GDP per capita increases. If the answer to both is “less,” then the opposite happens, and per capita GDP falls. The honest answer to whether immigration boosts per capita GDP growth is “it depends.” On the whole, skilled workers will increase per capita GDP, and the Trump administration’s attempts to restrict the entry of skilled workers are misguided.

Cowen argues that the United States has been more fortunate with its immigrants, in economic terms, than Europe.

“The problem, to put it bluntly,” he writes, “is that many of Europe’s immigrants are from quite different non-Western cultures. Furthermore, Europe is not always drawing in the top achievers from those cultures, whereas in America, Indian and Pakistani immigrants are quite successful…”

Immigrants drawn to American opportunity add more to the numerator than to the denominator.

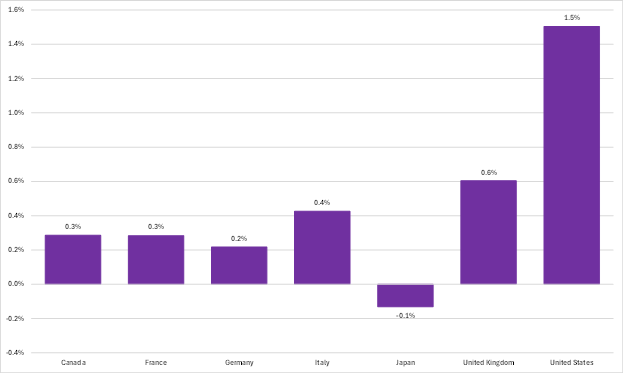

Productivity and Economic Growth

This explains part of the faster growth in GDP perworker in the United States, which, in turn, explains part of the faster growth in GDP per capita. In terms of GDP per person employed, the average annual real growth rate in the United States over the past 10 years was 1.5 percent, more than twice that of the second-placed United Kingdom, with 0.6 percent (Figure 3).

Figure 3: Average annual real GDP per worker growth, 2014-2015 to 2023-2024 (US dollars, PPP converted, Billions, Chain linked volume (rebased), 2020)

OECD Data Explorer

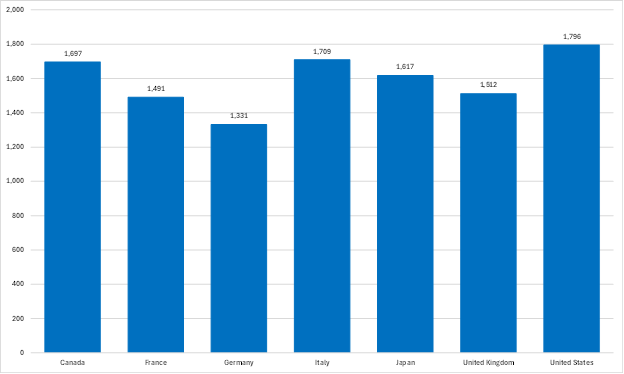

But Cowen notes that “Paul Krugman frequently put forward the argument that American and West European living standards are roughly the same, with Americans earning more but working longer hours.” And there is truth in this. American workers, on average, work longer hours than their G7 counterparts (Figure 4).

Figure 4: Average hours worked per year per person, 2024

OECD Data Explorer

But this is a level, and we have been investigating rates of growth.

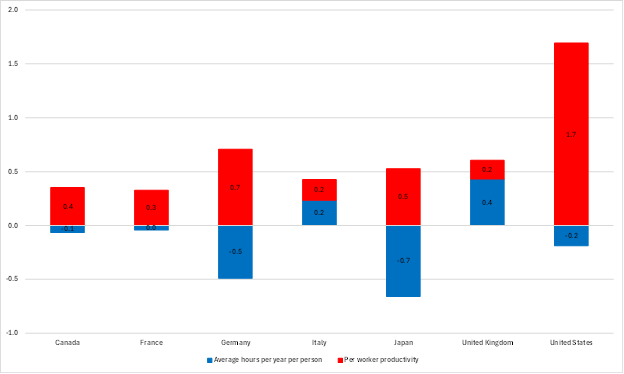

Growth in GDP per worker can be broken down into that share which comes from a worker working more hours and that which comes from a worker becoming more productive. When we break down the rates of per worker GDP growth shown above, we see, again, a different story. The United States saw a faster rate of per worker productivity growth between 2015 and 2024 than any other G7 country, more than twice the rate of Germany, in second place (Figure 5).

Figure 5: Average annual growth rates, 2014-2015 to 2023-2024

OECD Data Explorer

Cowen says that “as history unfolds, [Krugman’s] view seems increasingly untenable,” and he is likely correct.

American labor productivity growth does stand out among comparably rich countries and explains a good deal of why it’s per capita GDP growth stands out. Paul Krugman is wrong again.

The partial government shutdown stretched into another week after negotiators failed to reach a deal to fund the Department of Homeland Security (DHS) over the weekend.

Congress is on a weeklong recess and is not scheduled to return to Washington, D.C., until next week, leaving the shutdown’s end in limbo as both parties remain far apart on key provisions.

Senate Democrats are demanding a series of reforms to Immigration and Customs Enforcement (ICE), a position they have maintained since the fatal shootings of Alex Pretti and Renee Nicole Good during ICE operations in Minnesota.

Senate Minority Leader Chuck Schumer, D-N.Y., and his caucus are standing by a list of 10 proposed reforms, including requiring ICE agents to obtain judicial warrants and limiting the use of face coverings — proposals Republicans have described as red lines.

‘Americans are tired of masked agents conducting warrantless operations in their communities — secret police,’ Schumer said. ‘They’re tired of chaos, secrecy and zero accountability. That is not what law and order looks like, and Republicans simply cannot pretend that this outrage does not exist.’

However, ICE received additional funding under previously passed legislation, and core enforcement operations are expected to continue. Other DHS agencies, including the Transportation Security Administration (TSA), the Federal Emergency Management Agency (FEMA) and the Coast Guard, remain affected by the shutdown.

The White House has led negotiations for Senate Republicans and offered Senate Democrats a proposal that they have rejected. Details of that proposal have not been made public.

‘This is a Democrat-driven shutdown caused by their intransigence and desire to use government funding for services all Americans rely on as a hostage in order to achieve an unrelated political goal,’ a senior White House official said.

Senate Majority Leader John Thune, R-S.D., said lawmakers would receive 24 hours’ notice to return if a deal is reached.

‘I think all those reasonable efforts and requests have been overshadowed by the fact that the Democrats don’t seem to want to play ball,’ Thune said.

On the House side, Speaker Mike Johnson, R-La., told lawmakers they would receive 48 hours’ notice to return if the Senate passes a bill. The House is also in recess until Feb. 23.

Johnson and other Republicans have expressed support for the original DHS funding bill crafted by House and Senate appropriators, but the speaker said he does not want further delays in DHS funding to be attributed to the House.

House Minority Leader Hakeem Jeffries, D-N.Y., has said Democrats will not accept a funding bill that does not include significant reforms to ICE.

A new report from the far-left Human Rights Campaign shows a remarkable shift: a 65% drop in Fortune 500 companies publicly communicating commitments to diversity and inclusion initiatives. Just a few years ago, corporations raced to outdo one another with ever-expanding DEI pledges. Today, many are quietly stepping back.

This is not a retreat from fairness. It is a return to sanity.

For years, corporate America embraced an ideological experiment that blurred the line between equal opportunity and preferential treatment. What began as a push for broader inclusion morphed into quota-driven mandates, demographic scorecards and internal political signaling exercises that often had little to do with business performance.

Now, the legal system — and increasingly federal regulators — are pushing back.

Consider the recent lawsuit against Starbucks, where Missouri’s attorney general alleged ‘systemic discrimination’ in hiring and promotion practices tied to DEI goals. While a federal judge dismissed the case on procedural grounds, the filing itself signaled growing scrutiny over whether corporate diversity initiatives cross into unlawful discrimination.

Nike is currently facing a federal investigation by the Equal Employment Opportunity Commission over allegations that certain DEI-related employment practices may have resulted in race-based discrimination against White employees. Whether the agency ultimately finds wrongdoing or not, the investigation underscores a new reality: DEI programs are no longer insulated from legal challenge.

And JPMorgan Chase has been sued over allegations of ‘systemic’ race bias, including claims that the bank conducted ‘fake interviews’ to satisfy internal diversity targets. That allegation — that a company might go through the motions of interviewing candidates solely to hit demographic benchmarks — illustrates how performative compliance can undermine both fairness and trust.

But the scrutiny does not stop at employment law.

In recent weeks, the Federal Trade Commission reportedly sent letters to 42 of the largest and most profitable law firms in the United States, warning that racially discriminatory hiring practices — even if adopted under the banner of DEI — could constitute unfair or anti-competitive conduct. According to reporting, the firms were participating in a program overseen by the Diversity Lab that required at least 30% of leadership candidates to come from underrepresented groups.

That kind of industry-wide coordination raises serious questions.

First, there is the obvious Civil Rights Act concern: employment decisions cannot be made on the basis of race, period. But there is also a broader antitrust dimension. When competitors collectively adopt demographic quotas or coordinated hiring mandates, they may be engaging in collusive conduct — effectively setting industry standards through cooperation rather than competing freely for the best talent.

This theory is not new. Federal antitrust authorities have previously warned climate and ESG coalitions that there is no ‘ESG exception’ to the antitrust laws. As former FTC Chair Lina Khan stated plainly: competitors are not permitted to coordinate with one another simply because the coordination is framed as socially beneficial. The same logic applies here. There is no DEI exception to the Sherman Antitrust Act.

For years, corporate America embraced an ideological experiment that blurred the line between equal opportunity and preferential treatment.

The implications are enormous.

Retailers such as Nordstrom, Macy’s, Bloomingdale’s, Ulta and Sephora signed the ‘Fifteen Percent Pledge,’ committing to reserve 15% of shelf space exclusively for Black-owned brands. More than seventy major corporations — including competitors like Nike, Levi Strauss, Ralph Lauren and American Eagle — signed the ‘Count Us In’ pledge, coordinating around policies that include funding transgender surgeries for employees and engaging in shared lobbying efforts.

The legal question is no longer just whether these initiatives are politically popular. It is whether they create exposure under antitrust law by reducing competition or creating coordinated market standards among competitors.

Corporate America is beginning to recognize the risk.

Public companies exist to create shareholder value — not to serve as enforcement arms for shifting social movements. When executives adopted DEI mandates that required race-based hiring targets, demographic quotas, or coordinated pledges with competitors, they exposed their companies to multi-front liability: discrimination claims from employees, regulatory investigations, shareholder lawsuits and now potential antitrust scrutiny.

The 65% drop in DEI messaging suggests something important: boards and CEOs are recalibrating.

That recalibration is healthy.

There is nothing wrong with expanding opportunity, recruiting broadly, or fostering a respectful workplace culture. But the law demands equal treatment — not equal outcomes engineered through quotas or industry collusion. When companies forget that distinction, they risk violating both civil rights statutes and competition laws designed to protect markets.

Markets function best when companies compete — for customers, for innovation, and, yes, for talent. The moment competitors coordinate around hiring mandates or collective pledges, they drift away from competition and toward centralized standard-setting. That is precisely what antitrust law exists to prevent.

The pendulum is swinging back toward merit.

Employees want to know they were hired because of their ability. Shareholders want disciplined capital allocation. Customers want quality products at fair prices. None of those priorities require demographic quotas or public virtue declarations.

The retrenchment we are witnessing is not an attack on diversity. It is a rejection of coercion and coordination masquerading as virtue. It is a reminder that equal opportunity under the law applies to everyone — White, Black, male, female — and that industry competitors are not allowed to suspend antitrust principles simply because the goal sounds noble.

Corporate America is finally rediscovering a simple truth: treat people equally, compete vigorously, and let merit determine outcomes.

That is not only legally sound. It is economically sound. And it is long overdue.

Taiwan’s foreign minister says China has ‘clearly become a troublemaker that is maliciously attempting to disrupt the cross-strait status quo and intimidate peaceful countries.’

In exclusive comments to Fox News Digital, Foreign Minister Lin Chia-lung said China’s intensifying ‘authoritarian expansionism not only directly threatens Taiwan’s security and democratic system but also poses significant challenges to peace and stability in the Indo-Pacific region and around the world.’

‘Last June,’ Lin said, ‘[Chinese] aircraft carriers Liaoning and Shandong maneuvered beyond the second island chain, marking China’s first simultaneous, dual-carrier deployment into the Western Pacific. These developments demonstrate that Beijing’s expansionist ambitions extend far beyond Taiwan and pose an increasingly serious threat to the security and stability of the Indo-Pacific region and the world.’

Communist China was founded in 1949 and has not ruled Taiwan for a single day. Officially known as the Republic of China (ROC), Taiwan is currently recognized by eleven small countries, plus the Holy See. Beijing nonetheless rejects the reality of nearly 80 years of separate rule, describing Taiwan as a ‘sacred and inseparable part of China’s territory.’

China’s posture toward independently ruled Taiwan has hardened in recent years as President Xi Jinping removed term limits and consolidated near-total power. While earlier Chinese statements included talk of ‘peaceful unification,’ Beijing now openly threatens to use force.

In 2024, Xi directed the Chinese military to complete preparations for a Taiwan operation by 2027. Most defense analysts agree that an invasion would be costly, bloody and highly risky for China, Taiwan and any countries that come to Taiwan’s aid, such as the United States or Japan.

Lin echoed those warnings that a conflict in the Taiwan Strait would reverberate worldwide. ‘Peace and stability across the Taiwan Strait are vital to global security and prosperity,’ Lin said, noting that approximately 90% of the world’s most advanced semiconductors are produced in Taiwan and that roughly 50% of global commercial shipping passes through the strait. He added that Taiwan is grateful to the United States and other partners for resisting China’s efforts to unilaterally alter the status quo.

The foreign minister said Taiwan’s central role in geopolitics, technology and supply chains ensures that Washington places a high priority on cross-strait stability. He said U.S. policymakers understand that Taiwan’s semiconductor industry and related supply chains are critical to American economic security.

‘There is clear strategic continuity between the policies of President Trump’s first and second terms,’ said Lin, adding that Taiwan’s government will seek ways to coordinate with the United States ‘through values-based, alliance and economic diplomacy.’

Commenting on Washington’s Indo-Pacific strategy, Lin said, ‘The Trump administration and U.S. Congress continue to demonstrate a steadfast commitment to safeguarding peace and security across the Indo-Pacific region,’ Lin said, ‘which was emphasized in the 2025 National Security Strategy (NSS).’ The foreign minister also noted that ‘the recent NSS released by the Trump administration underscored Taiwan’s geopolitical importance as a link between the Northeast and Southeast Asian theaters.’

Lin said Taiwan is working to rebalance trade with the United States while strengthening strategic cooperation on AI. ‘The Trump administration’s AI Action Plan,’ he said, ‘underscores the importance of innovation, infrastructure and international cooperation for AI development.’

He also touted Taiwan’s growing investments in the U.S., including a $165 billion commitment by Taiwan Semiconductor Manufacturing Company (TSMC) in Arizona, and said Taipei is working to make it easier for Taiwanese companies trying to invest in the U.S.. ‘Against the backdrop of U.S.-China strategic competition and the restructuring of global supply chains,’ said Lin, ‘Taiwan’s enterprises understand the remarkable potential of investing in the United States.’

The foreign minister said Taiwan appreciates increasing American military support, highlighting that ‘Last December, the United States approved an arms sales package to Taiwan totaling $11 billion as well as signing the Taiwan Assurance Implementation Act and the National Defense Authorization Act for Fiscal Year 2026. These measures underscore the firm bipartisan support for Taiwan in the U.S. government.’

But he stressed that Taiwan is accelerating its own defense investments. ‘Last year, [Taiwan] President Lai Ching-te announced that Taiwan’s defense budget would increase to over 3% of GDP by 2026 and rise to 5% by 2030,’ he said. While parts of that plan have faced resistance in the opposition-led legislature, both major parties have publicly backed closer security cooperation with the United States and a stronger deterrence posture.

One year after fires tore through the Los Angeles region, devastation remains etched into the landscape, not only in the thousands of empty lots, but also in the near absence of rebuilding. More than 13,000 homes were destroyed across Los Angeles County; 12 months later, just 28 have been rebuilt.

What should have been a story of recovery instead reveals deeper institutional failure. Despite political urgency, partial regulatory reforms, and repeated promises of speed, reconstruction has stalled under the weight of a collapsing insurance market, regulatory overreach, labor shortages, and soaring construction costs. This slowdown has laid bare the fundamental limitations in California’s institutional capacity to respond effectively to large-scale crises.

County records offer a sobering picture of post-fire reconstruction. As of February 5, 2026, 13,142 parcels had been damaged or destroyed, representing 14,834 housing units. Los Angeles County received 6,116 rebuild applications and issued 2,894 permits, roughly 47 percent of applications. Construction is underway on about 1,420 projects, yet only 16 buildings have reached completion.

Permitting has, to be fair, moved faster in fire zones than elsewhere in California. The average permitting timeline in Los Angeles County’s fire zones is roughly 100 days — far faster than the up to 24 months for comparable projects in the Pacific Palisades outside designated fire areas, and quicker than the roughly eight months typically required in Altadena. Even so, this expedited fire-zone process remains well above the national norm, where permits are issued in about 64 days even absent disaster-related pressures.

California’s past performance offers little comfort that rebuilding will accelerate. In Malibu, only about 40 percent of the 488 homes destroyed in the 2018 Woolsey Fire have been rebuilt, suggesting that time alone does not resolve the state’s underlying constraints.

Under public pressure, lawmakers moved to partially reform the California Environmental Quality Act, a statute that subjects most construction in California to lengthy and expensive environmental review. On June 30, 2025, Governor Gavin Newsom approved Assembly Bill 130 and Senate Bill 131, which capped public hearings, shortened agency review timelines, expanded the Permit Streamlining Act, and introduced a “near-miss” review process. While officials touted these changes as a turning point, their effects remain unclear. Permitting may be faster in fire zones, but high construction costs, persistent administrative friction, and minimal completed rebuilding suggest that procedural reforms have left deeper economic and regulatory barriers largely intact.

The most immediate constraint is insurance — or, more precisely, the lack of it. Many homeowners simply cannot afford to rebuild because they are uninsured or severely underinsured. This is not a mystery, nor is it the result of homeowner negligence alone. For decades, California’s insurance market has been distorted by Proposition 103, passed by voters in 1988. The measure requires insurers to obtain state approval before raising rates and restricts them to using historical data when pricing risk. Insurers are prohibited from accounting for current or future fire risk, climate conditions, or even their own reinsurance costs.

As wildfire damages mounted, particularly after the catastrophic 2017 and 2018 fire seasons, insurers concluded they could no longer operate profitably in the state. The response was predictable. In 2023, seven of California’s twelve largest insurers paused or restricted new policies. In late 2024, months before the fires, companies including State Farm and Allstate canceled thousands of policies or exited high-risk areas altogether, disproportionately affecting communities like the Pacific Palisades and Altadena.

The result is a cruel paradox. The state insists on rebuilding in fire-prone regions while simultaneously preventing insurers from pricing risk honestly. Homeowners are left exposed, reconstruction stalls, and at least 600 property owners have already chosen to sell what remains of their land rather than rebuild.

Even for those with financing, California’s regulatory environment imposes steep costs. The state is estimated to have more than 400,000 regulations, and its building codes are among the strictest in the nation. California’s building regulations routinely exceed national model codes, mandating advanced energy efficiency standards, solar requirements, and green building measures years before they are adopted elsewhere. Much of California falls into high seismic design categories, requiring structural reinforcements that substantially raise construction costs. Accessibility rules under Chapter 11B often go beyond federal ADA standards, increasing design complexity and expense. Layered atop onerous land-use controls and costly environmental review requirements, these rules make rebuilding slower, more expensive, and less accessible, especially for small contractors and middle-income homeowners.

Labor and materials further compound the problem. The US construction sector needs to add an estimated 723,000 workers annually through 2028 just to keep up with existing demand. California’s construction labor market is particularly constrained. Construction employment is heavily regulated through prevailing wage mandates, skilled-and-trained workforce requirements, apprenticeship rules, and stringent Cal/OSHA standards. Combined with immigration restrictions and independent contractor reclassification rules, these policies raise hiring costs and reduce labor supply.

Building material costs have increased across the country, driven by multiple factors and compounded by current trade policy. Roughly seven percent of residential construction inputs are imported. Softwood lumber, the primary material used in homebuilding, is an illustrative example. Canada supplies approximately 85 percent of US softwood lumber imports and nearly a quarter of total domestic supply. Current tariffs of 34.5 percent are up from 14.5 percent last year, pushing costs even higher for builders already stretched thin. As a result, rebuilding in fire-damaged communities becomes not only slower but increasingly unaffordable.

A full year removed from the fires, Los Angeles has learned an uncomfortable lesson: disaster response is only as effective as the institutions that support it. Streamlined hearings and expedited permits cannot overcome a broken insurance market, regulatory overload, labor constraints, and punitive cost structures. Until California confronts these structural barriers head-on, rebuilding will remain slow, expensive, and unequal, and the next fire will likely replay the same grim story.

Iran claims it is open to compromise with the U.S. on a nuclear deal if the administration is willing to discuss lifting sanctions, a senior Iranian official said Sunday.

Majid Takht-Ravanchi, Iran’s deputy foreign minister, also said in an interview that the ball was ‘in America’s court to prove that they want to do a deal,’ adding: ‘If they are sincere, I’m sure we will be on the road to an agreement.’

‘We are ready to discuss this and other issues related to our program if they are ready to talk about sanctions,’ Takht-Ravanchi told the BBC.

Takht-Ravanchi’s comments came as Iran’s top diplomat traveled to Geneva for a second round of indirect talks with the U.S. delegation.

Abbas Araghchi left for the Swiss city following an initial round of negotiations last week with Oman again mediating the next round of talks, according to Iranian state media and the Associated Press.

U.S. officials, however, have emphasized that Iran — not the U.S. — is holding up progress in negotiations.

Secretary of State Marco Rubio said Feb. 14 that President Donald Trump would prefer to reach an agreement but warned it was ‘very hard to do’ one with Iran.

Past diplomatic efforts had collapsed in 2025 after Israel launched what became a 12-day war with Iran and U.S. strikes on Iranian nuclear sites.

But on Sunday, Takht-Ravanchi pointed to Tehran’s offer to dilute its stockpile of uranium enriched to 60% purity as evidence of its willingness to compromise, the BBC reported.

Asked whether Iran would ship its stockpile of more than 400 kilograms of highly enriched uranium abroad, as it did under the 2015 deal, Takht-Ravanchi said it was ‘too early to say what will happen in the course of negotiations.’

One of Iran’s main demands is that talks focus on the nuclear issue. ‘Our understanding is that they have come to the conclusion that if you want to have a deal you have to focus on the nuclear issue,’ Takht-Ravanchi said.

Takht-Ravanchi also said the ‘issue of zero enrichment is not an issue anymore and as far as Iran is concerned, it is not on the table anymore.’

Trump has since threatened further military action if a deal to curb Iran’s nuclear program cannot be reached.

The U.S. has also reinforced its military presence in the region amid heightened tensions and after spiraling protests across the country in December left thousands reportedly dead at the hands of the clerical regime.

The Trump administration is weighing involvement in the case of a protester who was fined for burning a Quran outside the Turkish Consulate in London, as U.K. prosecutors look to reinstate his overturned conviction, according to reports.

Officials are said to be discussing granting 51-year-old Hamit Coskun refugee status if the Crown Prosecution Service (CPS) wins its appeal, with a senior U.S. administration official telling The Telegraph the case is one of several ‘the administration has made note of.’

Coskun, of Armenian-Kurdish descent, had initially sought asylum in the U.K. from Turkey, where he says Islamic extremists ‘destroyed’ his family’s life and where he was jailed for protesting Islamist governance.

On Feb. 13, 2025, he traveled to the Turkish Consulate in London and set fire to a copy of the Quran while shouting slogans including ‘Islam is [the] religion of terrorism’ and ‘f— Islam.’

There he was attacked by Moussa Kadri, a passerby who chased him with a knife, kicked him and spat on him.

Kadri later received a suspended prison sentence after being convicted of assault and having a bladed article in a public place.

Initially charged with harassing the ‘religious institution of Islam,’ Coskun’s case drew intervention from the National Secular Society and the Free Speech Union, who argued prosecutors were effectively reviving blasphemy laws already abolished in 2008.

Coskun was convicted of a religiously aggravated public order offense and fined in June 2025.

That October, Coskun’s conviction was overturned when a judge ruled that while burning a Quran was ‘desperately upsetting and offensive’ to many Muslims, the right to free expression ‘must include the right to express views that offend, shock or disturb.’

The CPS is now seeking to reverse that decision at London’s High Court, with Coskun telling The Telegraph that if the appeal goes against him, he may be forced ‘to flee’ the country.

‘For me, as the victim of Islamic terrorism, I cannot remain silent. I may be forced to flee the UK and move to the USA, where President Trump has stood for free speech and against Islamic extremism,’ he told the outlet.

‘If I have to do so, then, to me, the UK will have effectively fallen to Islamism and the speech codes that it wishes to impose on the non-Muslim world,’ he added.

President Donald Trump and the U.S. administration have already criticized the U.K. and European governments over increased restrictions on expression.

In 2025, Trump slammed the U.K.’s laws around online speech, saying ‘strange things are happening’ there and that it was ‘not a good thing.’

At the Munich Security Conference in 2025, Vice President JD Vance also said, ‘In Britain and across Europe, free speech, I fear, is in retreat.’

Fox News Digital has reached out to the Department of State for comment.