For most of modern financial history, companies entered public equity markets gradually. Firms grew, matured, and eventually earned their place in major stock indices after demonstrating profitability, competent management, and staying power. Increasingly, though, that sequence has broken down. Companies now remain private far longer, growing quickly enough to accumulate extraordinary valuations behind venture capital and private funding rounds, and then approach public markets already among the world’s largest enterprises. The consequent pressure on stock indices, and the passive investment vehicles tied to them, is forcing a reconsideration of long-standing inclusion rules.

The latest debate centers on firms including SpaceX, Anthropic, and other artificial intelligence leaders that could soon debut publicly at valuations so immense that excluding them from major stock market benchmarks may render the indices unrepresentative of economic reality. Reports that exchanges and index providers are reconsidering special treatment for a handful of unusually large new equity listings echo earlier moments in financial history when market structure evolved faster than benchmark rules.

Such pressures have emerged before. During the late 1990s and early 2000s, firms such as Yahoo!, Google, and later Meta entered public markets with extraordinary investor attention and rapidly expanding market capitalizations. That prompted index providers to reconsider how quickly exceptionally large new listings should be incorporated. Nasdaq responded by creating expedited mechanisms allowing exceptionally large IPOs to enter the Nasdaq-100 more quickly than traditional rebalancing schedules would otherwise permit. The reasoning was practical: when benchmark-tracking funds represent a growing share of capital markets, excluding economically significant companies risks generating a disconnect between passive portfolios and the financial markets they purport to represent.

Another side to the argument deserves more scrutiny than it receives amid enthusiasm for technological innovation and market capitalization milestones. Institutional incentives have changed radically since index inclusion became a major event. And the mechanism by which being a component of a stock index has become important is beyond merely symbolic. The growth of passive investing now triggers billions of dollars in mechanical purchases from index funds and exchange-traded funds benchmarked to major indices. In effect, index decision committees now exercise considerable influence in private capital allocation decisions that were once determined more organically through decentralized management decisions and market processes.

Since the early 2000s, trillions of dollars have migrated into passive vehicles benchmarked to major indices such as the S&P 500 and Nasdaq-100. It’s an innovation that has vastly lowered costs and broadened individual access to equity ownership, but simultaneously elevated the stakes surrounding index membership. Admission can materially alter demand for a stock independent of changing fundamentals. Exclusion can similarly suppress ownership by institutional investors required to follow benchmark mandates.

It raises important economic questions. Markets, at their best, are discovery mechanisms. Prices emerge through dispersed information, entrepreneurial judgment, and risk-taking. Index providers traditionally functioned as passive observers of these processes, codifying outcomes rather than shaping them. But when trillions of dollars in stock purchases hinge on index inclusion — and index committees alter rules to accommodate particular firms — benchmarks begin to look less descriptive and more directive, intentionally or not.

Economically speaking, this creates a feedback loop. Firms now have an incentive to achieve immense scale in private markets; policymakers and investors argue, credibly, that benchmarks cannot ignore them; indices bend their methodologies; tremendous passive capital flows follow; and valuations receive an upward burst from non-discretionary buying pressure. The process begins to resemble administrative allocation rather than competitive market selection.

To be clear, this does not imply that companies such as SpaceX or Anthropic are unworthy of either their current valuations or inclusion in certain indices. Indeed, if publicly listed, those and other firms would almost certainly deserve substantial representation in broad equity benchmarks. Nor is the type of flexibility being employed by indexing firms inherently undesirable. Historical precedent demonstrates that markets periodically require methodological adjustments. Berkshire Hathaway’s unusual capital structure posed problems for index designers decades ago, and both Google and Meta entered benchmarks relatively quickly due to their sheer size, liquidity, and strategic importance. Tesla’s eventual inclusion in the S&P 500 required unusually careful handling owing to concerns surrounding the sheer magnitude of benchmark-driven buying.

But there is a meaningful difference between updating a methodology to reflect structural market changes and habitually creating exceptions for firms deemed “too important to exclude.”

A deeper issue pertains not to index rigidity, but the extraordinary transformation of corporate finance itself. Firms now remain private for longer periods because private capital is extraordinarily abundant, regulatory burdens associated with public listing are increasingly onerous, and founders/early investors increasingly prefer governance structures insulated from public shareholders and the costs associated with investor relations. Today, by the time many firms consider going public, they have already attained scales once associated only with mature public corporations.

If American markets increasingly produce private trillion-dollar companies that seek to undertake initial public offerings, benchmark methodologies will face mounting pressure to evolve. One should remain cautious about how far those adaptations go. Indexes derive legitimacy from transparency and consistency. If rules become excessively discretionary or increasingly, indeed predictably, cater to marquee names, the neutrality that made those benchmarks trusted in the first place will steadily decline. The recurring temptation to bend index rules for giant corporate newcomers is not merely a wonky equity market issue. It reflects a broader economic reality: capital markets are rapidly changing, and infrastructure built for earlier eras is struggling to adapt.

Any effort to modernize the relationship between public issuers, indices, and financial markets must preserve the market discipline and decentralized decision-making that make equity markets and their discounting function valuable in the first place.

“Economists have successfully predicted seven of the last three recessions….”

So goes the humorous, if uncomfortably accurate, adage. Business cycles have been a source of fascination for centuries. Some economists attributed them to sunspots. Others to historical cycles — Kondratiev (45–60 year waves), Juglar (7–11 year waves), and Kitchin (three-to-five year waves). These views belong neither to cranks nor obscure figures; well-known economists from William Stanley Jevons to Joseph Schumpeter championed them.

Tyler Goodspeed’s Recession: The Real Reasons Economies Shrink and What to Do About It belongs on the shelf of anyone tracking business cycles, financial markets, and economic growth. The book delivers a tour de force through US and UK economic history. Meticulously researched, it is full of data, analysis, and engaging stories about financiers, economists, politicians, and the occasional huckster.

I confess this book has done more to challenge my views of the business cycle than just about anything else I’ve read. Goodspeed argues, in fact, that the term “business cycle” is itself a misnomer. Economies do not operate according to predictable patterns or cycles. “Economic expansions don’t die of old age,” he writes, “they are murdered.”

The central claim of the book is that there are no natural or inevitable reasons why modern developed economies must experience recessions. Goodspeed, who served as acting chairman of the Council of Economic Advisers from June 2020 to January 2021 and is now chief economist at ExxonMobil, argues that there are always real shocks behind downturns — not a buildup of malinvestment, not irrational exuberance, not some self-generated collapse. He invokes Tolstoy’s famous maxim that every happy family is happy in the same way, while every unhappy family is unhappy in its own unique way.

So, he suggests, every recession is unique. Sometimes it is a drought, or locusts, or war, or unusual cold, or widespread strikes, or any number of other negative shocks. In fact, Goodspeed argues that recessions are rare precisely because they require several such shocks to occur nearly simultaneously.

Austrian economists like Mises and Hayek, and later Garrison, Rothbard, and Woods, have argued that artificial expansions of credit via central banks distort price signals around investment, its duration and sector, creating malinvestment and an unsustainable boom resulting in an unavoidable bust. Russ Roberts and John Pappola created memorable videos describing the debate between Hayek and Keynes on business cycles. One views recessions as caused by malinvestment, the other by too little spending.

Both are wrong, according to Goodspeed. Most approaches to studying or predicting business cycles — whether overconsumption, overinvestment, malinvestment, distorted price signals, or financial crisis — fall into the trap of oversimplifying historical episodes of economic contraction. These frameworks do not hold up when examining all recessions in the US and UK over the past three centuries.

With some familiarity in economic history and business cycles, I recognized many of the recessions Goodspeed highlights, though he also examines dozens of minor downturns that only specialists in economic history tend to notice. In the major cases of economic contraction and decline, he discusses the monetary policy shifts and financial crises that accompanied them — the same endpoints where many business cycle theorists stop their analysis.

Yet in case after case, significant physical shocks — often involving energy, food, or transportation — precede or accompany financial and monetary distress. Behind “malinvestment” and standard business cycle theories, then, are real, unpredictable shocks.

This aligns closely with the thesis of the New Classical economists, including Robert Lucas, Robert Barro, Thomas Sargent, Finn Kydland, and Edward Prescott. In this view, recessions and economic fluctuations are primarily driven by real physical shocks, with financial and monetary disturbances emerging as secondary effects.

The one theory of economic fluctuations that makes it through Goodspeed’s criticisms relatively unscathed was Milton Friedman’s “Plucking Model.” Friedman argued that recessions are temporary declines in economic growth below a trend line (like plucking an upward-sloping guitar string), that would eventually be reversed during recovery back to the trend line. In this model, recessions are the exception, rather than the rule, of economic dynamics.

In some ways, this makes a lot of sense. Friedman won the Nobel Prize in part due to his work distinguishing real from nominal (monetary) elements of the economy. The nominal variables shouldn’t affect real economic outcomes in the long run because people adjust their expectations and plans to changes in the money supply and the price level.

Friedman’s plucking model flips standard cycle theory. It predicts that a recovery’s speed and magnitude depend entirely on the severity of the bust, not the length of the preceding boom or the volume of artificial credit. This is exactly what Goodspeed finds across dozens of recessions. Recovery is far more predictable than recession. The worse the recession, the greater the subsequent rebound.

Recession delivers a powerful, accessible narrative of economic history, making significant claims about economic growth, contraction, and the nature of modern economies. It’s quite compelling. Still, I am not quite ready to abandon Austrian Business Cycle Theory.

The absence of a predictable pattern or regularity between credit booms and recessions does not mean they play no role. They may still matter as both a transmission mechanism and a source of financial fragility. Goodspeed himself emphasizes the importance of sound institutions, including free-market prices and effective financial risk management and distribution, in mitigating the severity of downturns.

It is no coincidence that many of the stories he tells center on stress, panic, or failure within the financial system. It may be true that “malinvestment” is not the primary driver of business cycle fluctuations, but financial leverage and distorted signals still matter. At the same time, Goodspeed’s warning against the hubris of market forecasting is worth taking seriously.

The economy, it turns out, is not only too complex to plan — it is also too complex to predict.

Last month, at a press conference ahead of an FA Cup semi-final, Pep Guardiola was asked about ticket prices for the 2026 World Cup. His answer was neither tactical nor diplomatic. “A long, long time ago, the World Cup was a celebration of the joy of football,” he said. “Everyone travelled across the world to watch their country. And it was affordable. Now it has become so expensive. Football is for the fans. This business doesn’t work without them.”

FIFA president Gianni Infantino had a different answer. When confronted with reports that World Cup final tickets listed on FIFA’s own official resale platform at nearly $2.3 million each, he laughed it off and promised to personally deliver a hot dog to anyone who paid that price. His substantive defence: “We are in the market in which entertainment is the most developed in the world. So we have to apply market rates.”

Both men are right, in their own way. Guardiola correctly identifies that something has been lost. Infantino correctly identifies the mechanism: market rates now govern a popular celebration. What neither man explains is why those market rates have drifted so far beyond what ordinary wage-earners can afford.

For that, you need to understand what happened to money in 1971.

The Numbers Are Not Subtle

For three decades, inflation-adjusted World Cup final ticket prices barely moved. Available data suggests the tournaments from 1994 through 2022 priced the premium final seat at roughly $1,300 in today’s dollars. Then 2026 broke the pattern entirely: the face-value top ticket for the final at MetLife Stadium is $11,000 — a near-sevenfold real increase in a single cycle. On FIFA’s own official resale market, seats have appeared for above $38,000. General consumer prices rose by roughly 20 percent over the same four years.

The Premier League tells a slower but structurally identical story. In the 1992-93 season, a Liverpool season ticket cost £250. Adjusted for general inflation, that ticket should cost around £534 today. Instead, Arsenal’s cheapest adult season ticket is £1,073 — twice what inflation would predict. The average matchday price has risen from £13.50 in 1992 to £83 today — sixfold, over a period when general consumer prices roughly doubled. Waiting lists for top-club season tickets now stretch 10 to 20 years.

These numbers don’t indicate a market that has gradually become more expensive. They describe a market whose underlying economic logic has been fundamentally transformed.

Why “Market Rates” Is Not an Explanation

Infantino’s defence — we apply market rates — is technically accurate but analytically empty. The interesting question is not whether football now operates at market rates, but why those market rates have suddenly moved so far beyond the reach of the fans who historically sustained the game.

In August 1971, President Nixon ended the dollar’s convertibility to gold, dismantling the Bretton Woods system and inaugurating an era of unconstrained fiat money creation. The eighteenth-century economist Richard Cantillon described the resulting dynamic: newly created money does not enter the economy uniformly. It flows first through the banking system and into financial markets, benefiting asset holders before prices adjust. Wage-earners receive the new money later, after prices have already moved. Over time, this produces a structural transfer of purchasing power from those who sell their labor to those who own assets. Whether intentional or not, it has become a recurring feature of modern monetary expansion.

Since 1971, central banks have repeatedly expanded their balance sheets — particularly after 2008 and again during the pandemic. The result is exactly what Cantillon predicted: asset prices have inflated dramatically faster than wages. Between 2008 and 2025, the US M2 money supply rose by more than 150 per cent, while US real median weekly earnings grew by less than 10 percent over the same period. Those who own financial assets have seen their real purchasing power grow enormously relative to those who depend on wages.

The Club as an Inflation Hedge

Football clubs are assets. Broadcasting rights are assets. The experience of attending a World Cup final — scarce, globally resonant, emotionally irreplaceable — is precisely the kind of good that asset-enriched capital seeks out.

When sovereign wealth funds began acquiring Premier League clubs — Saudi Arabia’s Public Investment Fund at Newcastle football club, Abu Dhabi’s City Football Group at Manchester City — they were not being irrational. In a world of low real interest rates, a globally recognised football club offered brand value, soft power, and a genuine store of value simultaneously. Football, in this light, increasingly behaves less like a public cultural institution and more like a luxury asset market.

Of course, monetary policy is not the only force reshaping football. The Premier League’s globalisation, the explosion of broadcasting revenues, the rise of corporate hospitality, and the emergence of football as a worldwide entertainment product all contributed to rising prices. But these developments themselves unfolded inside a monetary environment that systematically inflated financial assets and expanded the purchasing power of capital relative to wages. The Cantillon mechanism does not replace these explanations — it is the deeper structure within which they all operate.

This is why Infantino’s market-rate defence inadvertently damns itself. Football fans do not set the market rates he invokes. They are set by a global pool of capital systematically enlarged relative to wages over five decades of monetary policy. Dynamic pricing responds less to what supporters can pay than to what global asset holders are willing to pay. Monetary policy created that gap.

Infantino’s defence also fails on its own terms. He argues, not unreasonably, that selling tickets cheaply hands the premium to scalpers — that if FIFA priced the final at $500, touts would resell at $10,000 and pocket the difference. He is correct.

But whether FIFA captures the premium or a scalper does, the ticket ends up in the same hands: those with the greatest purchasing power. Lowering the face-value price does not return the World Cup to its fans. It just changes who profits from their exclusion. Pricing policy is downstream of monetary policy. FIFA can shuffle who captures the surplus. It cannot, by itself, change who has the surplus to spend.

What Guardiola Understands That Infantino Doesn’t

Guardiola’s remark — “this business doesn’t work without them” — is an economic observation, not a sentimental one. The atmosphere that makes a World Cup final worth broadcasting, the intensity that prices broadcast rights in the billions, the following that makes sponsorships valuable — all of it originates in the cheap seats. It was generated by working-class fans who built the sport’s culture over a century. The premium product that global capital now bids for is inseparable from that culture. And that culture is being priced out of its own creation. Football is one of the clearest examples of a cultural institution built by labor and increasingly consumed by capital.

Football Supporters Europe filed a formal complaint with the European Commission in March 2026, calling FIFA’s pricing structure “extortionate” and a “monumental betrayal.” The England Supporters Travel Club estimated that following England to the final would cost a fan more than $7,000 in tickets and basic expenses alone, before flights or accommodation — roughly two months of take-home pay on a median British wage.

Behind the statistics are real people. Anne-Marie Carr, a 54-year-old from York, told BBC Sport: “I have diligently attended England matches to earn the caps to get tickets for major tournaments, only to find that I, as so many others, am being priced out. WC 26 will be for the few, the sponsors and the glory hunters who’ve got the money.” From Ghana, Jojo Quansah told BBC World Service that supporters who had spent three years saving for their first World Cup experience were being forced to abandon those plans. “It’s been overshadowed,” he said, “by pricing those same fans out of a chance to watch their country play.”

Football Isn’t the Exception. It’s the Rule.

Football is a vivid case of a pattern running through the entire post-1971 economy. Housing in desirable cities, university education, and quality healthcare — all have inflated far faster than wages over this period. The goods with the deepest social meaning are often the first that asset-price inflation prices beyond wages. Official consumer price indices capture the falling cost of televisions and sneakers. They do not capture the rising cost of being present at the things that matter.

This is the structural logic of the Cantillon effect operating across generations. No one sat in a boardroom and decided to price the working class out of football. No conspiracy was required. The monetary architecture of the modern world advantages asset owners over wage earners — steadily, automatically, and without malice — and football, being an asset, followed the system’s logic. The sport built by the working class has become a luxury product through the slow, compounding arithmetic of who gets new money first.

Pennsylvania and Virginia recently passed legislation to increase their minimum wage to $15 per hour, closing the gap with Oregon ($15.55 as of July 1) and California ($17.90 in some places). In all, 34 states mandate a minimum wage higher than the federal minimum wage of $7.25 per hour. The potential economic detriments of a minimum wage — namely, job losses — are well known. But the trend toward higher and higher minimum wages ought to prompt us to reconsider their purpose.

The standard assumption about progressivism is that it’s intrinsically good — after all, who would oppose progress? Progressivism in the twentieth-century, though, had a much more squirrely history. Many progressives were proponents of eugenics, opponents of classical liberalism, and advocates of scientific racism. And the origins of the federal minimum wage emerged from these attitudes.

Compared to today’s progressives, early twentieth-century progressive economists were at least honest and understood the impact of a minimum wage — they knew that it would cause job losses. But they believed the job losses caused by the minimum wage were a social benefit, not a detriment.

As the historian Thomas Leonard summarized it:

Sidney and Beatrice Webb put it plainly: ‘With regard to certain sections of the population [the ‘unemployable’], this unemployment is not a mark of social disease, but actually of social health.’

‘[O]f all ways of dealing with these unfortunate parasites,’ Sidney Webb opined in the Journal of Political Economy, ‘the most ruinous to the community is to allow them to unrestrainedly compete as wage earners.’ …A minimum wage was seen to operate eugenically through two channels: by deterring prospective immigrants and also by removing from employment the ‘unemployable,’ who, thus identified, could be, for example, segregated in rural communities or sterilized.

In other words, for progressives, race determined the standard of living and the standard of living determined the wage. Edward Ross, the American sociologist and progressive, put it more bluntly: “owing to its high Malthusian birth rate the Orient is the land of ‘cheap men,’ the coolie, though he cannot outdo the American, can underlive him.” Woodrow Wilson, echoing the same sentiment, said that Chinese immigrants could “live upon a handful of rice for a pittance.”

Women didn’t escape the implications of a minimum wage either. Many progressives held that the proper social order required women to be excluded from the workforce. A minimum wage served to push women back into the home where they belonged. For progressives, this had the added benefit of encouraging larger families among Anglo-Saxons, preventing the country from being overtaken by groups they deemed inferior.

The progressive theory of the minimum wage therefore went as follows: a minimum wage creates a barrier to entry in the labor market, which in turn freezes out the “undesirables” from the labor market who previously could compete for work by taking lower wages. To that end, a legal minimum wage, the progressives thought, would freeze out racially undesirable immigrants, the mentally and physically disabled, and women — all while handing a raise to deserving white Anglo-Saxon men.

Now, the sordid origins of the minimum wage are not, in themselves, an argument against it. A person’s moral character does not inevitably taint the policies they enact (the genetic fallacy). But the arguments twentieth-century progressives made in favor of the minimum wage give us insight into its actual impacts.

Progressives today are more inclusive and view job losses as a social cost, not a benefit. Yet they continue to support a minimum wage. They would argue their predecessors misunderstood its effects, and that modern support rests on different reasoning. They would say minimum wages benefit the least-fortunate Americans.

But that claim is worth questioning. While earlier progressives held abhorrent views on race and gender, they seem more accurately to have understood economic effects: a sufficiently high minimum wage prices low-wage workers out of the market. Today’s progressives, despite their intentions, risk producing similar outcomes.

Extensive research shows that a minimum wage not only tends to raise unemployment, but that its effects also tend to fall disproportionately on the most disadvantaged workers, including the disabled, youth, lower-skilled workers, immigrants, and ethnic minorities. Another study found that job losses from minimum wage increases were much more prevalent among black workers than among white workers.

Nobel laureate economist Milton Friedman argued that the “real tragedy of minimum wage laws is that they are supported by well-meaning groups who want to reduce poverty. But the people who are hurt most by higher minimums are the most poverty-stricken.”

While the intentions of today’s minimum wage proponents are certainly better than their historical roots, how different are they from the original progressives if the effects remain the same? Intentions certainly matter, but results matter more. In effect, the minimum wage continues to disadvantage the most marginalized in our society.

There’s something very ironic about extolling mercantilism at the Reagan Library. Scott Bessent did just that last week, arguing that America had been wrong to trust markets, wrong to value efficiency, and wrong to believe that “the invisible hand would correct vulnerabilities.”

Jamieson Greer followed this up with a piece in the International Monetary Fund’s F&D Magazine, where he declared that tariffs and import regulations had been unfairly cast aside by an “elite consensus” and that “the return of tariffs and import regulations creates an opportunity to update old assumptions and dated models with the hard evidence of real-world data and experience.”

These are not new arguments. For anyone who understands the history of economic thought, they are also easily rebuked. The argument against mercantilism is not new, and it is not difficult to understand. It is, however, very inconvenient for the current occupants of 1600 Pennsylvania Ave.

What is Mercantilism?

Briefly, mercantilism is the idea that a nation, not unlike a household, is wealthiest when it has large reserves of money. This was the animating idea behind economic policy up until nearly the end of the eighteenth century. Nations focused their attention on acquiring large sums of gold. To do this, they used policy to encourage exports and discourage imports. Exports were considered “good” because it meant that the nation acquired gold in an exchange. Imports were “bad” because they required giving up gold. Thus, the focus of a mercantilist system is on production, not on consumption.

This began to change in the late eighteenth century when Adam Smith published his treatise, An Inquiry into the Nature and Causes of the Wealth of Nations. The full title is worth spelling out here because what Smith does in this volume is not “defend free market capitalism,” but Inquire about The Nature of Wealth. Specifically, he asks, “what is wealth?” and his answer is quite simple: wealth is measured in what you can purchase. Tom Hanks in Cast Away still would have had to knock his own tooth out with an ice skate if he’d washed ashore with a trillion-dollar coin in his pocket. And therein lies the lesson: while you do need money in a modern economy, what matters is what you can actually do with that money, not how much money you have.

Neo-mercantilists accept this, but want to argue that national security concerns override this logic and that economists have somehow missed this. They call for updating economic models to be more in line with “tariffs, industrial policy, and the costs of globalization.”

They are wrong on both counts. Economists have not missed the national security argument. While there may be legitimate cases for protectionism in the name of national security, those cases are extremely limited and certainly do not justify tariffs on the entire world and the imposition of managed trade. The actual threats to American national security are not the product of being “too open” or “too dependent.” The risks we face today have been greatly overstated and are actually the fault of excessive government.

The Economists Were Wrong?

Greer opens his F&D piece with a riff on a Chesterton quote: for the past thirty years, “tariffs were not tried and found wanting but rejected by au courant economic models and left untried.” This is quite simply revisionist history. Every single president for the last thirty years has tried tariffs, and those tariffs were found wanting. Bill Clinton imposed tariffs on imported steel, automobiles, and bananas. George W. Bush imposed tariffs on steel. Then, President Obama imposed tariffs on Chinese tires because of alleged dumping. That then brings us to President Trump, who famously used tariffs during his first term, President Biden who expanded Trump’s tariffs (something the current Trump administration hasn’t shied away from pointing out), and now the second Trump presidency, which has obviously seen tariffs being used.

Far from being bastions of success, these were not just “found wanting,” they were disastrous and in most cases, lifted because of their pernicious effects. This wasn’t surprising. Economists warned about exactly this at the time. They were correct then, and they’re correct now.

Greer complains that trade models assume full employment and frictionless worker transitions. It’s a fair point; the models that economists use do contain simplifying assumptions. But the question we have to ask is whether these assumptions meaningfully affect the results of the analysis to the point of needing to be jettisoned. And the answer is a resounding “no.” Pointing out a model’s imperfections does not mean we jettison its underlying insights.

Washington Gave China the Edge, Not the Other Way Around

The Bessent-Greer framework would have us believe that American manufacturers have been competing in a game rigged by Chinese state subsidies and that we are “losing.” That American communities have been hollowed out by cheap imports and the offshoring of jobs and that American manufacturing is in decline. And they blame economists for naively supporting free trade when, in the words of Scott Bessent, “the warning lights were glaring all around us.”

As the old saying goes, when you point a finger at one person, you’ve got three more pointing back at yourself. And those three fingers are doing a lot of work, here.

American manufacturing is not in decline because of free trade. In fact, it could hardly be described as “in decline” to begin with. The truth is that manufacturing output in the US is quite high.

One would have to be very selective in choosing which data to examine to conclude that manufacturing is in decline, and even then, an honest accounting would include several paragraphs of caveats.

What is in decline is manufacturing employment. But this, again, is not because of “free trade” resulting in companies shipping jobs overseas or the so-called “China Shock” that occurred after China joined the World Trade Organization. It’s because of tremendous gains in productivity by the American worker — largely thanks to automation, advanced machinery, and improved production processes — combined with onerous regulatory burdens that made building new factories in America far too costly. The solution to this is not to make manufacturing at home more expensive through tariffs and other trade restrictions; it’s to make it easier for America’s manufacturing workers to acquire the materials they need to produce their output.

The truth of the matter is that the US has, on a per-capita basis, the most productive manufacturing sector on the planet. Not even the “mighty” China comes close. The US employs about 12.6 million manufacturing workers. China, by comparison, employs some 212 million. With nearly 200 million more manufacturing workers, China only outproduces us by about 60 percent.

What About National Security?

Here, we must concede that there is a shred of truth to the protectionist logic. If there is a genuine national security concern and if domestic production were the only way to mitigate these concerns, then protectionism might have a leg to stand on. But note the repeated use of qualifiers in that sentence. Each one deserves examination before we jump to, “therefore: use protectionism.”

The truth of the matter here, and one that protectionists simply do not acknowledge, is that what matters for national security concerns is ensuring domestic access. Domestic production is certainly one way of doing this, but it is far from the only way.

Consider the case of steel, clearly a critical material for national defense purposes. How dependent on foreign steel are we? The American Iron and Steel Institute reports that only 23 percent of finished steel in the US was imported. The Association for Iron & Steel finds that the US is the third largest producer of steel in the world. Where do we get the rest of our steel? According to the US International Trade Association, we get the rest of our steel from, in order: Canada, Brazil, Mexico, South Korea, Vietnam, Japan, Germany, Taiwan, the Netherlands, China, and 68 other countries. This is not a dependency. This is resiliency, as long as we do not push away our allies.

The exception to this would be a monopoly supplier of a critical material. China’s dominance of so-called rare earths provides a potential example. But here again, the question we should be asking is, “why is China the dominant supplier of these materials?” and the answer is staring us right in the face: excessive environmental and labor regulations. Once again, it’s not “free trade” that caused a vulnerability to China. It’s too much government standing in the way. The solution is not to fight government ineptitude with more ineptitude. It’s to get the government out of the way so that markets, not politicians, can actually solve the problems.

What Would Actually Work

The irony that Scott Bessent championed mercantilist justifications for protectionism by invoking Reagan’s name at the Reagan Library to an audience that presumably understands Reagan’s position is palpable. That Jamieson Greer did the same in the International Monetary Fund’s magazine is equally ironic. Restricting trade does not make a nation wealthier or safer, and it never has. Mercantilism has been wrong for the past 500 years, and it will be wrong for the next 500 years, too.

Instead, American interests, both economic and security alike, are best served through free trade and globalization. Trade between nations brings us closer together and vastly reduces the likelihood of war between trading partners. Globalization ensures that if war were to break out, access to critical materials for the war effort can remain uninterrupted. The real risks to America’s supply chains have been created by excessive regulation, not openness.

It’s time to end the experiment with tariffs once and for all. We need to be tearing down barriers to trade, not erecting new ones. Doing so would unleash the American worker on the rest of the world. Doing so will not only make us wealthier, it’ll make us safer, too.

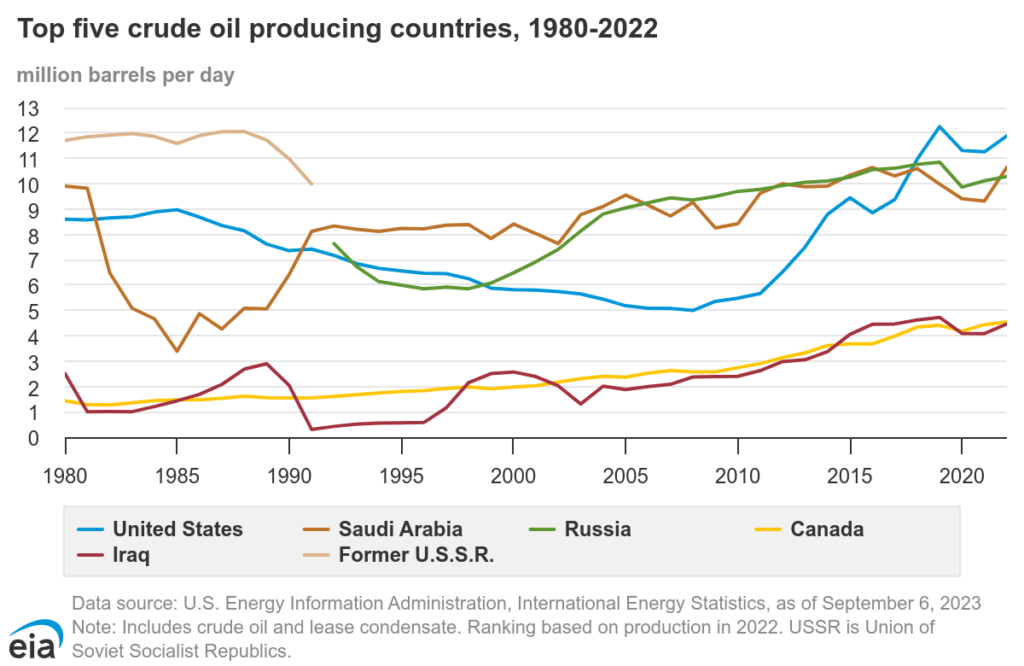

For decades, a small group of oil-producing states has exercised extraordinary influence over the global economy—not through innovation or competition, but through coordinated supply restriction. The Organization of the Petroleum Exporting Countries (OPEC) has long operated as one of the world’s most powerful cartels, managing oil supply to sustain higher prices and shape global energy markets. In a competitive market, producers expand output, compete, and innovate. Cartels do the opposite: they restrict supply, distort prices, and impede the natural functioning of markets.

That system is now beginning to crack. On May 1, 2026, the United Arab Emirates, one of OPEC’s largest and most strategically important producers and a member since 1967, withdrew from the organization, citing “national interests” and a desire for an independent energy policy, thereby removing 10 to 15 percent of the cartel’s production capacity.

This departure is part of a broader trend: Qatar and Ecuador left in 2019, Angola followed in 2024, and countries such as Gabon and Indonesia have also stepped away. What once appeared to be a cohesive bloc is increasingly fragmenting, a sign that the cartel model itself is becoming harder to sustain.

The Economic Case Against OPEC

OPEC, founded in 1960, remains one of the clearest examples of cartel behavior in the modern global economy. Controlling roughly 40 percent of global oil production and around 80 percent of proven reserves, its members coordinate production quotas to restrict supply and sustain higher prices rather than allowing markets to adjust through competition.

Since the 1970s, the United States has frequently viewed OPEC as both an economic and geopolitical challenge, with presidents from Richard Nixon to Joe Biden criticizing the cartel for driving up energy costs and fueling inflation. President Donald Trump openly described OPEC as a monopoly, while Congress has repeatedly considered antitrust measures against the cartel.

One of the clearest examples of OPEC’s market distortion is its deliberate supply restriction despite soaring global demand. Between the end of World War II and 1973, oil production in future OPEC countries rose from roughly 3 million to 30 million barrels per day, supporting one of the strongest periods of economic growth in modern history. Yet despite global oil demand rising after the 1973 oil crisis to nearly 90 million by 2012, OPEC repeatedly kept its production ceiling near 1973 levels, around 30 million barrels per day, to sustain higher prices. It is therefore unsurprising that economic research generally concludes that oil prices would likely be lower in the absence of OPEC’s coordinated supply restrictions.

The effects of this policy extend far beyond the oil sector. Because oil is essential to transportation, manufacturing, agriculture, and global trade, OPEC’s supply restrictions raise costs across the entire economy. According to IMF estimates, each sustained 10 percent increase in oil prices can raise global inflation by about 0.4 percent while reducing global economic output by around 0.1–0.2 percent.

Higher energy prices fuel inflation, weaken purchasing power, and disproportionately harm lower-income households and energy-importing developing countries. In 2022, for example, Pakistan’s oil import bill more than doubled, contributing to a severe foreign exchange crisis that required IMF intervention.

Beyond these immediate effects, academic research has also highlighted the cartel’s broader structural inefficiencies. A major study by researchers at Duke University, the University of California, Los Angeles, and KU Leuven found that OPEC’s production restrictions increased global oil production costs by roughly $160 billion and shifted investment toward more expensive extraction methods such as offshore drilling and fracking. By limiting low-cost production, the cartel distorted investment decisions, reduced market efficiency, and imposed substantial costs on the global economy.

Why OPEC Is Becoming Increasingly Unsustainable

Despite its historical influence, OPEC has always faced a fundamental problem: cartels are inherently unstable. Maintaining coordinated production cuts requires discipline, yet each member has an incentive to quietly exceed quotas and capture additional profit. As a result, quota violations, hidden discounts, and overproduction have been recurring features of OPEC since its founding, exposing the internal contradictions of a system built on collusion rather than competition.

At the same time, external competition has steadily weakened the cartel’s power. The rise of non-OPEC producers — especially the United States shale industry — dramatically increased global supply and reduced OPEC’s ability to control prices. Between 2008 and 2025, US shale production surged from roughly 5 million barrels per day to 13.7 million barrels per day, helping turn the US into the world’s largest oil producer. This wave of competitive production contributed to the sharp collapse in oil prices in 2014–2016 and significantly reduced OPEC’s market share and pricing power.

Ironically, OPEC’s own strategy helped create the forces weakening it. Years of artificially high oil prices incentivized investment in technologies such as hydraulic fracturing and horizontal drilling, fueling the US shale revolution. By 2014, OPEC was forced to abandon its price-support strategy and flood the market in an unsuccessful attempt to crush US shale producers. Yet technological innovation, growing competition, and expanding investment in alternative energy continue to erode the cartel’s long-term power, demonstrating a broader economic reality: when markets are free to respond to price signals, competition and innovation eventually unravel cartel power.

This shift is increasingly visible even within OPEC itself. The United Arab Emirates’ departure reflects a growing recognition that competing freely may be more sustainable than remaining bound to restrictive quotas. As competition, innovation, and new energy sources continue to weaken cartel power, global energy markets are moving toward more open, market-driven production.

OPEC may still influence prices in the short term, but the broader trend is clear: market forces are gradually overtaking coordinated restriction.

The Trump Administration has proposed coercive new tariffs that would not only raise costs during a national affordability crisis, but would also set a dangerous precedent for executive power.

The new tariffs of 10 percent to 12.5 percent would be imposed on Americans who import goods from countries that allegedly fail to take adequate action against the use of forced labor. It has been illegal to import goods made with forced labor since 1930, as USTR acknowledges. The new tariffs, which would apply to countries that provide 99.4 percent of US imports, would be based on whether other countries maintain and enforce similar measures.

The proposed tariffs, imposed under Section 301 of the Trade Act of 1974, are remarkably similar in scope to the Trump Administration’s illegal 10.8 percent International Emergency Economic Powers Act (IEEPA) tariffs and its illegal 10 percent Section 122 tariffs.

IEEPA tariffs were imposed because the United States allegedly faces a national economic emergency. Section 122 tariffs were imposed because the United States allegedly faces fundamental international payments problems. Section 301 tariffs have been proposed in response to foreign policies regarding forced labor that are allegedly unreasonable and burden US commerce.

Despite the three different justifications, the ultimate tariff actions are nearly identical. But the newly proposed Section 301 tariffs are particularly dangerous.

Section 301 actions can be either mandatory or discretionary. Mandatory actions include measures designed to address foreign actions that are unjustifiable or that violate our trade agreements. These measures must be roughly proportional to the foreign restriction imposed on the United States.

Discretionary actions include measures designed to respond to foreign actions that are unreasonable or discriminatory and that burden or restrict US commerce. There is no explicit requirement for these measures to be commensurate with the burden imposed by foreign actions.

Either way, Section 301 tariffs are intended to secure the removal of foreign barriers, not to impose long-term tariff increases on Americans. President Trump and former US Trade Representative (USTR) Robert Lighthizer imposed the biggest Section 301 tariffs in history to encourage China to modify its investment and intellectual property policies during President Trump’s first term. Unfortunately, those tariffs failed to achieve their stated goals. The tariffs were supposed to expire after four years, but the Biden Administration took the unprecedented action of extending them, and the Trump Administration is now considering whether to extend them again.

Because these proposed Section 301 tariffs are discretionary, not mandatory, current USTR Jamieson Greer arguably has the authority to pluck tariff levels out of thin air.

According to Greer, “The failure of our most important trading partners to address the importation of goods made with forced labor is unacceptable. This creates a dynamic where American workers are forced to compete globally on an unlevel playing field.”

His statement may appear to be relatively innocuous. In reality, it represents a massive power grab designed to give USTR unlimited control over imports.

If allowed to stand, the new template for future tariffs will be:

Announce: “The failure of our most important trading partners to ______ is unacceptable. This creates an unlevel playing field.”

Fill in the blank with anything that can be dreamed up.

Assert the stated foreign action is unreasonable and burdens US commerce.

Section 301 then gives USTR blanket authority to impose duties, limitations, or even import prohibitions, unless the courts or Congress intervene. Future USTRs, regardless of political party, may inherit essentially unlimited tariff power.

A reasonable response would be for Congress to change our trade laws to require a vote on Section 301 tariffs. After all, in 1776, the American colonists declared their independence in part to escape the authority of a King who cut off our trade with all parts of the world.

Two-hundred and fifty years later, Congress should embrace our heritage by passing legislation like the No Taxation Without Representation Act, introduced by Sen. Rand Paul (R-KY). His bill and similar proposals requiring Congress to vote on tariffs are needed to fend off new threats to our freedom to trade, including the unprecedented expansion of Section 301 tariffs.

One of the most misleading ideas in American politics is that the United States has a large, fixed class of permanently poor people stuck at the bottom year after year, while everyone else moves on without them.

That story is emotionally powerful. It also happens to be a poor guide for serious policy.

Poverty is real. Hardship is real. Some people do remain trapped for long periods, and that deserves serious attention. But the popular picture of a vast, permanent underclass does not describe most Americans who show up in the bottom income quintile in any given year. As economist Anthony Davies has put it, many are there because of “retirement, homework, and diaper rash.” That line works because it captures something basic: a snapshot of income is not the same thing as a life story.

Students often have very low current earnings. So do many retirees living on savings or Social Security instead of wages. So do young parents working fewer hours, people between jobs, and entrepreneurs in low-cash-flow years. Treating all of them as members of a permanent poor class is not compassion. It is a category mistake.

The data back that up. The Federal Reserve’s Survey of Consumer Finances distinguishes between “actual” and “usual” income precisely because current-year income can be temporarily depressed. In 2010, about a quarter of families reported that their actual income was unusually low relative to normal. That matters because it means many households classified as poor in a given year are experiencing a temporary dip, not living permanently at the bottom.

In fact, the same survey found that a large share of households in the lowest quintile by actual income ranked higher when measured by usual income instead.

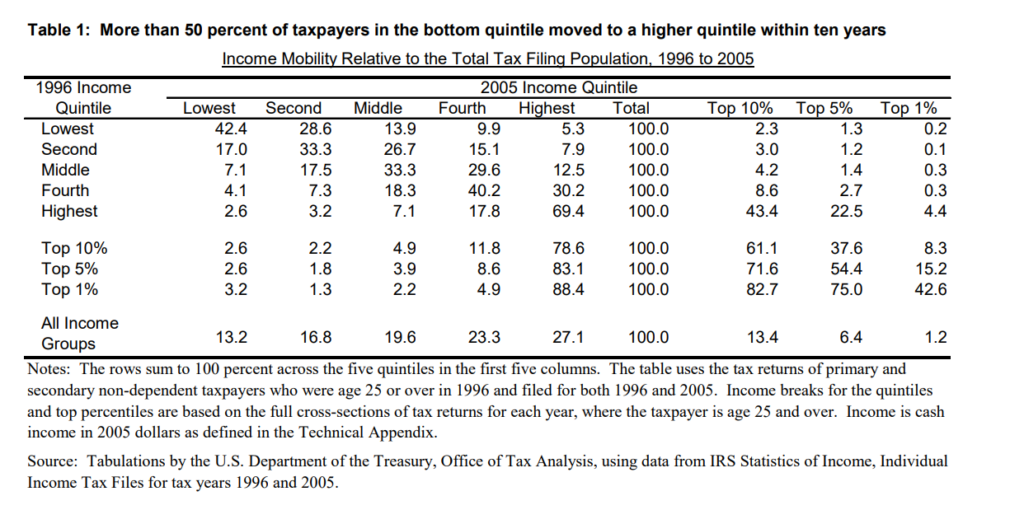

The tax data tell the same story. A Treasury study tracking taxpayers from 1996 to 2005 found that about 56 percent moved to a different income quintile over the decade. More important, roughly half of those in the bottom quintile moved up by 2005, depending on the measure used. About 29 percent moved up one quintile, another 29 percent moved up at least two quintiles, and roughly five percent moved all the way from the bottom quintile to the top quintile. That is not what a rigid caste system looks like. It is a dynamic picture in which many people pass through low-income years rather than remain stuck there permanently.

This is where so much bad policy begins. Politicians see a one-year income snapshot and talk as if they are looking at a permanent social class. They are not. They are often looking at transition.

This does not mean every measure of mobility is strong. A lot of the confusion comes from mixing together two different questions. The first is short-run income mobility: do people move up or down within their own lives? On that question, the evidence clearly shows substantial movement. The second is intergenerational mobility: do children rise above the economic position of their parents? That is a different question, and the answer there is more mixed.

The newer Census mobility data show that income mobility varies significantly by geography, age, race, and sex. And other work has shown that absolute mobility has weakened relative to earlier generations. Those are serious concerns. But uneven mobility is not the same as a large, fixed, poor class.

The latest Archbridge Institute report on social mobility in the 50 states broadens the analysis beyond annual income. Archbridge evaluates mobility through four pillars: entrepreneurship and growth, institutions and the rule of law, education and skills development, and social capital. It also distinguishes between natural barriers such as family instability or social networks and artificial barriers created by policy, such as excessive occupational licensing, weak school choice, or heavy regulation. That is a much better framework than casually conflating poverty, inequality, and mobility.

The state rankings tell an important story. In Archbridge’s 2025 report, Utah ranked first, followed by Vermont, Montana, Wyoming, and Idaho. At the bottom were Louisiana, Mississippi, Alabama, New York, and Arkansas. That does not prove one policy explains everything. It does show that institutions matter.

Mobility is shaped by the rules, incentives, and social conditions people live under. The poor are not static, but the barriers they face can be.

This is where the free-market case becomes especially important. If you care about mobility, you should care about growth. The AEI “Land of Opportunity” project and its essay on the greatness of growth and the American Dream make the point clearly: growth is not a side issue. Growth is the oxygen of mobility.

A faster-growing economy creates more businesses, more jobs, more opportunity, more room for incomes to rise, and more chances for people to accumulate wealth over time. A slower-growing economy makes class lines harder and mobility weaker.

That is why policies that burden growth hurt the poor most over time. Heavy regulation, bad schools, housing shortages, excessive licensing, and weak property rights do not just reduce efficiency in the abstract. They reduce mobility in practice.

A recent article highlights how land-use rules and housing constraints quietly kill mobility by making it harder for families to move to places with better labor-market opportunities. Another essay points to research showing that economic freedom, especially lighter regulation and stronger property rights, is associated with greater intergenerational mobility.

That is the key insight the static-poor narrative misses. If policymakers really want more upward mobility, the answer is not to freeze people into permanent income categories and redistribute more aggressively. The answer is to remove the barriers that keep people from climbing.

That means stronger growth, more entrepreneurship, more housing, better schools, more school choice, lower regulatory burdens, and institutions that reward work, saving, investment, and family stability. It also means respecting people’s freedom to vote with their feet toward states, cities, and communities with better opportunity. Mobility is not just something economists measure after the fact. It is something people actively pursue when they are free to move toward better institutions and opportunities.

The myth of the static poor survives because it is politically useful. It turns a moving picture into a still frame. It makes the government look like the only answer. But it misses the reality that most Americans who are poor at one point in time do not stay there forever, that incomes often rise over time, and that wealth accumulation frequently follows when people are free to work, save, invest, and build.

The real task is not to manage a permanently poor class. It is to build a freer society where more people can rise.

The newest Medal of Honor recipient, the late Master Sergeant Roddie Edmonds, was honored because he said no.

So much goodness in our lives, including the defense of liberty, begins with saying no.

It was January 1945. The war was months from ending, and Edmonds was the highest-ranking soldier among 1,292 American prisoners at a German stalag. The camp commandant ordered all Jewish soldiers — around 200 men — to fall out the next morning. Anyone who disobeyed would be shot.

Through a sleepless night, Edmonds instructed his men: “We’re not doing that.” Everyone would fall out — the sick, the infirm, all of them. They would tell the Germans they were all Jews. There would be no breaks in their ranks.

The next morning, the commandant was enraged when all 1,292 soldiers fell out. With a luger pressed to his head, Edmonds told the commandant, “We are all Jews here.” The commandant backed down. Two hundred lives were saved by a no.

In Edmonds’s case, his inspired courage was rooted in his deeply held Christian beliefs and commitment to the Golden Rule. The natural pull towards self-preservation gave way to a higher moral law.

Cicero instructed, “We are all servants of the laws, for the very purpose of being able to be freemen.”

In his classic book Flow, psychologist Mihaly Csikszentmihalyi drew on Cicero’s insight that “accepting limitations is liberating.” He used the example of monogamous marriage, arguing that commitment frees people from the exhausting task of constantly maximizing emotional returns.

The benefit of saying no to seemingly infinite possibilities, Csikszentmihalyi argued, is that “a great deal of energy gets freed up for living, instead of being spent on wondering about how to live.”

Edmonds did not have to wonder what the right thing to do was. His chosen constraints had already made the decision. His job was to show up and be the vehicle for a historic no.

Oliver Burkeman generalizes Csikszentmihalyi’s lesson in his book, Four Thousand Weeks. He urges readers to resist “the seductive temptation to ‘keep your options open’” in favor of “big, daunting, irreversible commitments.”

Doing so requires standing firm against FOMO — the fear of missing out — and recognizing that missing out on most things is inevitable. As Burkeman notes, “‘Missing out’ is what makes our choices meaningful in the first place.”

Understanding the necessity of constraints in our personal lives prepares us to defend liberty in public life. The person who never practices saying no to himself is poorly equipped to say no to those who would govern him.

A free society depends on our willingness to reject the claims of would-be masterminds who believe they can redesign complex social orders from above.

In his essay “Individualism: True and False,” Friedrich Hayek warned against the belief that society can be successfully directed by designing minds. True individualism, he argued, requires “an acute consciousness of the limitations of the individual mind.” False individualism, by contrast, rests on an “exaggerated belief in the powers of individual reason.”

True individualism fosters humility toward “the impersonal and anonymous social processes by which individuals help to create things greater than they know.” False individualism produces contempt for anything “which has not been consciously designed.”

In other words, false individualists are unwilling to restrain their own designs for society.

Hayek also rejected the myth of the good ruler. A free society, he argued, should not depend on finding wise or virtuous people to run it. Because individual knowledge is limited, any social order capable of sustaining broad human cooperation requires “strict limitation of all coercive or exclusive power.”

While free people say no to masterminds, they say yes to evolved rules, norms, and traditions — including the rule of law — that preserve liberty even when their origins and full effects cannot be fully understood. As Hayek observed, “Our submission to general principles is necessary because we cannot be guided in our practical action by full knowledge and evaluation of all the consequences.”

Hayek would also have us reject political expediency disguised as “the interests of society.” Why object to deciding every case on its merits? Because in practice, expediency untethers society from principle. The belief that wise leaders can improvise solutions case-by-case may be among the greatest threats to liberty.

Still, why do good-hearted people continue accepting these mistaken ideas? Economic and historical illiteracy explain part of it. But the Stoic philosophers asked a deeper question: Why do we say yes when we should say no?

The Stoics believed people surrender their inner freedom by accepting false impressions — mistaken judgments about reality. My manager criticized my work, so I’m going to be fired. That driver cut me off, so my anger is justified. The political version is the most dangerous of all: This emergency is different. This leader can be trusted. This time the designing mind will succeed.

Because people rarely practice withholding assent from their impressions, they accept them at face value. Epictetus urged his students: “Take up the practice right now of telling every disagreeable impression, ‘You’re an impression, and not at all what you appear to be.’” (Handbook, 1.5)

Unchecked habits weaken our ability to think clearly and act deliberately. As Epictetus warned, every angry reaction strengthens the habit of anger itself. (Discourses, 2.18) False impressions do not announce themselves as false. The discipline is learning to pause and ask: Is this really what it appears to be?

In Letter 95 of his Letters on Ethics, Seneca argued that principles are indispensable because judgments otherwise become captive to whatever emotion or circumstance is most vivid in the moment. “It is principles,” he wrote, “that can fortify us, maintain us in safety and tranquility.”

Because people often “don’t know what it is they want, except in the very moment when they want it,” as Seneca observed elsewhere, examining our impulses helps reveal the fears, desires, and false judgments that distort our thinking.

That wintry day in the stalag, Edmonds did not deliberate. His principles, not his impressions, had already made the decision. The only question was whether he would act on them.

That is the same question each of us faces — thankfully not in a German prison camp, but here and now. Will we stand firmly enough on principle to say no to the mistaken beliefs that threaten liberty?

When it comes to economic analysis, price indices are almost everywhere. In fact, the American Institute for Economic Research publishes its own Everyday Price Index. Keeping track of each one would be a full-time job in and of itself. Some, like the Consumer Price Index or the Producer Price Index, receive tremendous coverage and discussion. Others, like the Import Price Index, often go largely unreported and underappreciated.

This Explainer seeks to correct this. Once understood, the Import Price Index, with its ability to summarize the changes in the price of imported goods, is one of the most important tools of economic analysis available. It can help businesses and consumers understand what is happening in the world, how it affects their bottom line, and what steps (if any) they can take to mitigate those effects. It also helps those interested in policy understand where problems may lie and what the effects of various policies have been on the world stage.

Like all statistics, understanding how it is constructed and how to use it in conjunction with other data can provide a rich understanding of the global economy. This also helps us understand where the evidentiary reach of the Import Price Index ends. This matters for trade policy in particular, as changes in the Index are often cited as evidence that one party is paying the cost of tariffs and other duties.

This Explainer proceeds in four parts. First, it provides a brief history of the origins of the Import Price Index and the problems that its creation solved. Second, it describes what the index is — what it is not. Third, it explains what the Import Price Index can tell us about tariffs and their incidence. Finally, it considers the limits of the index and how it can be misinterpreted.

What Is the Import Price Index?

The Import Price Index (IPI) is an official monthly measure of how the prices of goods entering the United States change over time. It is produced by the Bureau of Labor Statistics (BLS) as a part of its International Price Program.

The idea of an import price index was most forcefully proposed by Irving Kravis and Robert Lipsey in their 1971 book Price Competitiveness in the World. Prior to this, economists had typically studied international trade by deriving prices based on reports of total spending and quantities imported — an indirect method that produced what are called “unit values.” By design, unit values are averages, and averages can be misleading. For example, when a child is born, the unit value of household income per person falls, but it would be foolish to treat that as a loss of income. Kravis and Lipsey found that the unit-value measures produced indices that were more volatile and systematically biased than those based on direct price measurement.

The IPI answers a simple question: “Are we paying more or less than we used to for the things that we buy from abroad?”

What Is and Is Not Included in the IPI?

To answer this question, the IPI measures the average change in the price level for a “representative basket” of US imports. To construct this, the BLS looks at the actual prices paid by importers in the US for the goods they import. Survey staff at the BLS collect this information directly from importers through their participant program.

What Is Included

For example, imagine a simple economy that imports steel, aluminum, and bananas. We could record the amounts purchased and prices paid in Year 1 in a table such as this:

Good

Quantity

Price Per Ton

Total Spent

Steel

1.5 million tons

$1,000

$1.5 billion

Aluminum

2 million tons

$3,000

$6 billion

Bananas

4 million tons

$1,250

$5 billion

All told, this simple economy imported $12.5 billion worth of imports.

The following year (Year 2), suppose that the import data is this:

Good

Quantity

Price Per Ton

Total Spent

Steel

1.8 million tons

$1,200

$2.16 billion

Aluminum

2.1 million tons

$2,800

$5.88 billion

Bananas

3.5 million tons

$1,500

$5.25 billion

This time, the economy imported $13.29 billion worth of goods. But what happened to import prices overall? The price of steel and bananas increased, while aluminum became cheaper. The quantities also changed.

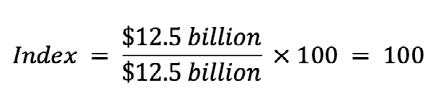

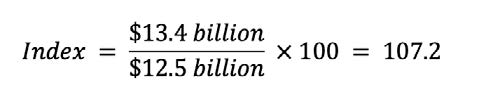

To isolate what is happening to import prices, we need to compare the cost of the same basket of goods over time. That requires establishing a representative basket of these goods. For simplicity, let’s use Year 1’s quantities. The key question, then, is: how much would Year 1’s basket cost at Year 2’s prices? The answer: $13.4 billion.

With this, we can construct an index. Year 1 serves as the base year — the year to which all others are compared. The index for Year 1 is calculated as follows:

Since Year 1 is the base year, this works out to be:

For Year 2, it would be:

From this, we can say the price of the representative basket of imported goods increased by 7.2 percent from Year 1 to Year 2.

This example is obviously contrived and simplified. For starters, economies do not import just steel, aluminum, and bananas but tens of thousands of goods. They also import goods from many countries under different conditions, and for a variety of purposes. Some, like bananas, are imported for final consumption by consumers. Others, like steel and aluminum, are used in domestic manufacturing. The BLS tracks all of this.

Within their monthly figures, they also break imports down by type of good, country of origin, and stage of processing — that is, whether a good is a raw material, an intermediate good, or a final good. This degree of granularity gives the IPI significant strength. If we want to know how the price of, say, household appliances imported from China has changed over time, we can find the answer.

To do all of this, the BLS collects data by surveying thousands of companies, asking them to voluntarily report the actual price of a specific item they imported that month. To construct an accurate index, the goods in question must be fixed across multiple dimensions. In an ideal world, the goods would have identical specifications, come from the same trading partner, and be shipped the same way over time.

Unfortunately for the BLS, almost none of this holds in a world that is constantly innovating. Products evolve, sometimes in fits and spurts and other times by leaps and bounds. Consider the iPhone over just the past ten years. Phones have gotten thinner, more powerful, and, since 2022, no longer include a charger in the box. This latter change means that not only has the product changed, but it’s also shipped differently than before, owing to smaller boxes that allow for more iPhones to be packed in a shipping container.

The BLS tracks all of this, too, adjusting prices as necessary to reflect changes in quality. To do this, it must decide how much of a price change reflects an actual price movement and how much reflects buyers receiving a different product than before. These decisions matter greatly — different choices can produce meaningfully different measurements of price changes.

What Is Not Included

The Import Price Index covers changes in the price of imported goods, but not imported services. But even saying that it covers only goods requires further clarification. For example, any costs incurred after the goods arrive at the port are not included in the IPI. These would include costs associated with warehousing, distribution, wholesaling, and any retail markups. The IPI only considers the price the importers pay at the water’s edge. All other costs for the imported goods come later.

This matters for trade policy because, as the BLS notes, “the prices for the items used to calculate the Import/Export Price Indexes exclude duties.” In this context, duties are taxes or tariffs placed on imported goods. This makes sense because the legal incidence — who actually pays the US Treasury — falls on Americans. As a result, import duties are applied after goods arrive at the port.

Additionally, because the IPI is measured in US dollars, exchange rate movements are automatically baked into the index. When the dollar strengthens, American buyers will pay fewer dollars for foreign goods even if prices abroad do not change. Conversely, when the dollar weakens, import prices in dollars tend to rise. This matters because when there is significant exchange rate movement, the currency effect on the IPI can be large enough to impact the index. Anyone using the IPI to make claims about trade policy must account for exchange rate movements.

Who Pays the Tariff?

At its core, a tariff is a tax on the importation of goods. When the US imposes a tariff on, for example, steel, that tax raises the cost of bringing steel into the domestic market. Like any tax, there is a distinction between the legal incidence (who writes the check) and the economic incidence (who bears the cost). The question of who bears the economic incidence of a tariff is of genuine interest to policymakers when assessing the impacts of trade policy.

In practice, there are three parties that can absorb a tariff, and any combination of them can bear some of the total burden:

The foreign exporter can absorb the tariff. In this case, the exporter lowers its pre-tariff price and sells the goods to the US market at a discount. After the tariff is applied, the final price paid by the importer remains roughly unchanged, inclusive of the tariff.

The importer or domestic business can absorb the tariff. Should this happen, the foreign exporter keeps prices steady, and the American importer pays the tariff on top of that price. The cost is then absorbed somewhere in a supply chain, such as reduced profits for domestic manufacturers, wholesalers, or retailers.

The US consumer can absorb the tariff. Under this scenario, the cost of the tariff is passed through to the end consumer in the form of higher retail prices.

Using the IPI to study the incidence of the tariff is relatively straightforward. If foreign exporters lower their dollar prices in response to US tariffs, we would see the IPI fall in the affected product categories after the tariff takes effect.

If, however, foreign exporters keep their prices the same, the IPI would remain relatively flat, or even rise. This would indicate that the full cost of the tariff is being paid by the US importers, who must then decide how much of the added cost to pass on to domestic manufacturers and consumers.

Researchers have used this exact logic, especially in the last ten years, to analyze the effects of the Trump tariffs imposed in 2018 and 2019, and are now doing so for tariffs in 2025. The results have been fairly consistent: once exchange rate movements are taken into account, foreign exporters largely kept their prices steady.

This is an important finding in its own right. It indicates that, rather than foreign entities paying these tariffs, Americans faced nearly the full burden — either through reduced profitability in downstream industries due to higher material costs or higher prices paid by households.

What the IPI Cannot Tell Us

For all its usefulness, the IPI alone cannot tell us everything we might want to know about the effects of trade policy.

Because it measures prices at the water’s edge, it does not tell us what happens to prices at the cash register. Tracing the full pass-through from import prices to consumer prices requires combining the IPI with the Producer Price Index and the Consumer Price Index. It also requires a model of how supply chains respond to these cost pressures — specifically, which costs are passed along and which are absorbed. The IPI is the beginning of this chain of analysis, not the end.

As noted earlier, the IPI also does not account for exchange rate movements, which can either amplify or obscure the effects of trade policy. During the tariff escalation of 2018 and 2019, the US dollar became significantly stronger against the Chinese yuan. This was in part due to the tariffs, which foreign countries can respond to by devaluing their own currency, but also because of Chinese state policy designed to monetize their growing debt problems. A weakened yuan will automatically lower the dollar price of US imports from China, which would show up in the IPI as falling import prices. But again, this is not evidence that China was “paying the tariffs.”

The IPI also does not capture product switching or supplier substitution. When tariffs make imports from one country more expensive, firms often adjust to avoid them. When the US imposed tariffs on South Korean washing machines in 2012, Samsung and LG simply moved production to China and continued exporting from there. Likewise, US importers shifted their purchases to Vietnam and Mexico. Tariffs on Chinese steel redirected purchases to Canada and Brazil. In these cases, the IPI remained largely unchanged because the now-tariffed products were rerouted through alternative countries not subject to tariffs. Yet the actual costs that Americans paid for these products rose, as production shifted to less efficient and more distant suppliers.

Finally, the IPI cannot measure trades that did not happen. Because tariffs impose costs, they necessarily reduce the volume of trade by preventing transactions that otherwise would have happened and made both parties better off. In the absence of these trades, domestic resources are redirected toward less efficient uses. The IPI reflects none of this, capturing only the price of goods that were actually imported. It remains silent on the economic welfare costs of goods that were not imported because the tariffs made them too costly.

Reading the Import Price Index Responsibly

The IPI is a genuinely valuable tool — well-constructed and useful when applied appropriately. It becomes even more powerful when used alongside other data, such as exchange rates and consumer and producer price indices. For economists, business analysts, central bankers, and policymakers, it can provide important insights into the effects of trade policy.

Every tool has proper uses and improper ones. A thermometer is a great tool for determining if someone is sick, and your doctor carries one for good reason. However, a thermometer alone is not a good tool for distinguishing between the flu and a common cold. Likewise, using the IPI to claim that foreign countries are “paying the tariff” is like using a thermometer reading alone to declare that someone is healthy.

Fortunately, the data needed for this kind of analysis and others like it are freely available online. The IPI, the consumer and producer price indices, and exchange rate data are all publicly available and updated regularly. Understanding what each measure captures is not just important for economists and their students taking exams. When trade policy is changing rapidly and justified with sweeping claims, an informed public that knows how to read the evidence is essential.

What the IPI is not, however, is a complete answer to the question of who bears the cost of tariffs. It tells us what happens at the water’s edge, not on the factory floor, not at the warehouse, and not at the cash register. It cannot capture the effects of currency movements or supply chain shifts, nor can it tell us anything about trades that did not happen.