Alexis de Tocqueville was born on July 29, 1805. Two hundred and twenty-one years later, he has become a man whom every political tribe seeks to claim as its own. The most ardent suitors at the moment are the post-liberals. Patrick Deneen and the national conservatives have made Tocqueville something close to a patron saint, finding in his portrait of democratic America an early glimpse of liberalism’s fatal contradiction. Liberal societies, they argue, dissolve the moral and communal supports on which they depend, until nothing is left but isolated individuals standing alone before an enormous state. The remedy, they say, is to recover virtue, religion, and community, and to enlist a government willing to form its citizens toward the common good.

The first half of this story is hard to argue with. Tocqueville indeed believed that a free society draws on reserves of virtue it does not itself create. And he believed that a people interested in nothing beyond its own comfort would eventually lose the capacity to govern itself. He sometimes put the point more strongly still. “Despotism may govern without faith,” he wrote, “but liberty cannot.”

But the post-liberals have Tocqueville exactly backwards on the question that actually divides us, which is not whether free societies need virtue but where a free society is supposed to get it.

A careful reading of Tocqueville reveals that the cure he prescribed is very nearly the opposite of the one they are selling.

What Tocqueville Granted

Tocqueville thought that religion was indispensable to American freedom. One of its most important roles, he believed, was to serve as a public institution that gave democratic citizens fixed points in a world of flux. Tocqueville believed that the mores of a people — their habits, beliefs, and settled ways of living — mattered more to the survival of free government than its written laws.

“There is no country in the world,” he wrote, “in which political institutions can prove a substitute for common sense and public morality.”

Notice, though, that there are two different claims tangled together here. One is that a free people need virtue. This is the sound core of the post-liberal worry. A liberalism that pictures the free individual as requiring no formation, no restraint, and no inherited traditions is living on borrowed capital, and eventually the loan comes due.

The other claim is that freedom requires not merely virtue but religious faith. This claim is far more contestable, especially in our secular age. Nevertheless, we can grant it without handing the argument to the post-liberals. That’s because the real debate is not about ends but about means.

In a free society, what is it that actually cultivates virtue and sustains faith? It turns out that Tocqueville had an answer to this question. But it is far from anything on the post-liberal agenda.

Where Virtue Comes From

In America, Tocqueville found a wide variety of institutions aimed at improving the character of the people. Crucially, however, the vast majority of these institutions belonged to society rather than the state. The thing that struck Tocqueville most forcibly was the sheer density of voluntary association.

“Wherever at the head of some new undertaking you see the government in France, or a man of rank in England,” he wrote, “in the United States you will be sure to find an association.”

Americans banded together to build schools, churches, hospitals, and a thousand other things a Frenchman would have waited for the state to provide. These associations were a kind of practical school where people developed customs of cooperation, responsibility, and self-command. Virtue, for the American, grows out of habit, and habit out of free action repeated until it becomes second nature.

The same was true of self-government. Tocqueville called the New England township the place where Americans learned to be free.

“Town-meetings are to liberty what primary schools are to science,” he wrote; “they bring it within the people’s reach, they teach men how to use and how to enjoy it.”

The citizen who managed the affairs of his own town acquired the habits a free people cannot do without, and acquired them in the only way such habits can be acquired: by exercise.

And then there is religion, where his argument is sharpest and least convenient for the people now quoting him. American religion was powerful, Tocqueville thought, precisely because it kept its distance from political power.

“Religion in America takes no direct part in the government of society,” he wrote, “but it must nevertheless be regarded as the foremost of the political institutions of that country.”

He had seen what happened in Europe when churches climbed into bed with regimes, and he stated the lesson clearly: “The Church cannot share the temporal power of the State without being the object of a portion of that animosity which the latter excites.”

Tying a faith to the state only weakens it, binding its fortunes to a government that will someday fall and to all the resentments that government gathers on its way down.

The pattern here is clear. Every one of these institutions is local, participatory, and independent of central power. Each does its work from below, through free people acting for themselves. For Tocqueville, neither virtue nor faith is the kind of thing that can be handed down from above.

The Cure That Is the Disease

Tocqueville would have been alarmed, then, by the post-liberal agenda, or at least by its most ambitious version. A post-liberal who wanted only to defend the family, the church, and the school against the forces dissolving them would find Tocqueville a friend, not a critic. The alarm comes with the further step of enlisting the central state in the work of moral formation.

Using the power of the state to make citizens good would, on his account, only deepen the very isolation and passivity of democracy that it promises to heal.

His most famous prophecy was of a new kind of despotism, gentler than the old and thus much harder to resist. He imagined “an immense and tutelary power” rising over a nation of busy private individuals and taking the whole business of living off their hands. The power would be “absolute, minute, regular, provident, and mild.” It would labor willingly for their happiness, but would insist on being “the sole agent and the only arbiter of that happiness,” and would keep them, he said, in “perpetual childhood.”

Tocqueville’s target was a state that frees its people from the burden of an adult responsible life, one that takes the trouble of living off their hands and leaves them little to do but enjoy themselves. This comforting paternalism is, of course, not what the post-liberals are after. But in making the state the arbiter of virtue, they produce the same infantilizing effect in the domain that matters most. The post-liberal state relieves its citizens of the hardest and most personal labor there is: the labor of working out for themselves how to live.

That labor is precisely the mechanism through which character develops. Virtue is the fruit of habit, and the habits a free people most need ripen only where they are practiced. Law can restrain vice and shore up the institutions in which such practices happen. What it cannot do is practice for us. A government that commands its citizens into goodness gets the outward act, but the active virtue Tocqueville admired has to be grown, and it grows only where people govern themselves.

To be clear, this is not an argument against coercion as such. Tocqueville was no libertarian, and the townships he praised as schools of virtue were, after all, institutions of coercive government. But the authority of the townships was local, plural, and answerable. It was an authority that citizens could influence through voice and, if necessary, escape through exit.

What Tocqueville feared was not government but administrative centralization — the drawing of every local and private concern into the central state. Let a centralized power “penetrate into the privacy of individual interests,” he wrote, and “freedom would soon be banished.”

The post-liberal virtue-state is that penetration carried to the soul: the formation of souls lodged in the central state, the one task he thought had to stay dispersed, handed to the institution he trusted least to hold it.

In the end, Tocqueville cared less about who held power than about how much of it had pooled in one place.

“There is,” he wrote, “and I cannot repeat it too often, there is in this matter for profound reflection for those who look on freedom as a holy thing, and who hate not only the despot, but despotism.”

When he felt the hand of power lie heavy on him, he said, he cared little to know whose hand it was, and was no readier to bow because it was “held out to me by the arms of a million of men.” He might have added that it makes little difference whether such a power reaches for our property or for our souls.

Classical liberals have always feared concentrated power in the first of those domains, and met it with competition and dispersion rather than gentler masters. The post-liberal virtue-state asks us to make an exception in the second. But a government strong enough to make us virtuous is a government strong enough to make us anything it likes. That alone is reason to keep the making of virtue where Tocqueville found it: in the hands of free people, governing and improving themselves.

The idea of a “pink tax,” that women commonly pay more for equivalent goods, has sparked public debate and inspired various policy proposals. This concept gained prominence after the New York City Department of Consumer Affairs released its 2015 report From Cradle to Cane: The Cost of Being a Female Consumer, describing many examples of women’s products costing more than nearly identical men’s products. While the report documented many cases of women paying more than men for similar products, the causes of these differences are more complicated than the notion of a straightforward tax. Understanding how prices emerge in a market economy offers another way to interpret these disparities.

The NYC study offers several examples intended to highlight real-world price differences for women’s products. Early in the study, the authors acknowledge that some price disparities are justifiable but claim that “these higher prices are ‘mostly unavoidable for women.’”

Some cases raise as many questions as they answer. One example in the report compares two Radio Flyer scooters sold on Target’s website: a standard red version priced at $24.99 and a ‘pink sparkle’ version priced at $49.99. The report treats this difference as an unavoidable burden on women or parents of girls, yet consumers remain free to purchase either product. Paying for the higher-priced pink version reflects a preference for a particular product design, rather than an unavoidable tax.

Even the study’s own data suggest a more nuanced picture. Women’s products were priced higher 42 percent of the time, men’s products were higher 18 percent of the time, and prices were equal in the remaining 40 percent. Such findings are more complicated than the notion of a uniform tax imposed on women.

Critics might push back against the scooter example as an outlier. The strongest version of the pink-tax argument isn’t really about isolated items like a single scooter. Rather, critics point to broader patterns across categories where comparison is harder to avoid, such as dry cleaning that charges more for women’s shirts, or personal-care products like razors marketed to women at a premium. In these cases, critics argue, “choice” is a weaker defense, since substitutes aren’t always available and the men’s and women’s products do not appear, at first glance, to differ in production costs.

This is a fair challenge, but it still doesn’t establish gendered pricing as the cause. Dry cleaners often cite genuine cost differences; women’s shirts frequently require hand processing or different cleaning methods altogether due to design and fabric. Personal care markups may reflect smaller batch sizes, different formulations, or packaging costs rather than gender per se. However, even if production costs are identical, a price difference alone does not establish bias any more than airlines charging more for aisle seats constitutes discrimination against passengers who prefer extra legroom.

Economists associated with the Austrian school, beginning with Carl Menger and later developed by Friedrich Hayek and others, emphasized that value is subjective rather than inherent in goods themselves. As Peter Boettke, Don Lavoie, and Virgil Storr observe, subjectivism lies at the center of the Austrian tradition and directs attention toward the meanings and preferences individuals attach to goods and services. Earlier theories, such as the labor theory of value, suggested that value derives from production inputs, but experience shows otherwise. A hand-turned chair requiring many hours of labor may still garner no buyers, while a designer handbag costing relatively little to produce may sell for thousands.

More than a century before the Austrian school emerged, Adam Smith observed the famous water-diamond paradox. Water is essential to life, yet it is generally inexpensive because it is abundant. Diamonds, though far less necessary, command high prices because they are scarce and highly valued by consumers.

These examples show why price differences between men’s and women’s products are not necessarily discriminatory. Prices emerge from consumer preferences, perceived value, and supply and demand. If pink items are valued more highly, companies rationally price them higher. Even identical production costs can result in different prices if a segment of consumers is willing to pay more for one variant. Conversely, if people do not value a product as highly, they will pay less.

Price differences should not automatically be interpreted as evidence of bias. More commonly, they are signals, the accumulated result of millions of individual preferences and purchasing decisions made across countless transactions. No single firm sets these prices arbitrarily. Prices emerge from the interaction of producers and consumers responding to the information available to them.

The pink tax framing, while an entry into an interesting discussion, is misleading. A tax is imposed from above and remains just as it was legislated. Unlike a traditional “tax,” no one is forced to pay markup for women’s items. Prices respond, however imperfectly, to what consumers actually value. If prices are to change, the most direct mechanism is not legislation, but the accumulated force of consumer choices over time. Prices are not obstacles imposed on consumer preferences, but reflections of them.

The Federal Open Market Committee is expected to leave its policy rate unchanged at this week’s meeting, with CME FedWatch assigning close to a 65 percent probability that the FOMC will maintain the current target range of 3.5 to 3.75 percent. For the second meeting in a row, that expected outcome is at odds with the guidance provided by the leading monetary rules. This raises the question of whether the new Warsh-led Fed is prepared to follow through on its promise of delivering price stability.

What the Rules Say

The latest Monetary Rules Report from AIER’s Sound Money Project shows that the Fed’s current policy rate falls below the range recommended by leading monetary rules. All twelve estimates in the report indicate that the Fed should raise its policy rate at the upcoming meeting.

The strongest case for tighter policy comes from Taylor-type rules. These rules respond to both inflation and labor market conditions, raising the recommended policy rate when inflation exceeds the Fed’s target unless that pressure is offset by significant economic weakness. With inflation still well above 2 percent and little evidence of substantial labor market weakness, both factors point toward a less accommodative policy stance.

The original Taylor Rule produces the most aggressive estimate, prescribing a federal funds rate of 6.01 percent. A modified version, which places more weight on the current policy rate and uses a forecast of future inflation, produces a lower estimate of 4.24 percent. Even after incorporating those more gradual and forward-looking features, however, the rule still prescribes a federal funds rate roughly half a percentage point above the current target range.

Rules based on nominal GDP, or total dollar spending in the economy, tell a similar story. A nominal GDP growth rule, which calls for raising rates when nominal GDP growth exceeds 4 percent, points to a 4.25 percent policy rate. A nominal GDP level rule, which recommends raising rates when total spending exceeds a steady growth path, produces the lowest estimate, at 3.76 percent. That prescription is very close to the upper bound of the current target range. Nevertheless, it is also consistent with a 25-basis-point hike, especially when considered alongside the other rules.

A Test of the Fed’s Credibility

The first FOMC statement of the Warsh era plainly stated, “The Committee will deliver price stability.” With inflation still well above the Fed’s 2-percent target and every leading monetary rule pointing toward a rate increase, will Warsh and his colleagues follow through on that promise and tighten monetary policy? The market considers a hike possible but unlikely, with CME FedWatch pricing in roughly a 35 percent probability of a 25-basis-point increase.

The committee can offer several reasons for waiting at least one more meeting before raising rates. The latest inflation data showed a notable decline in June, with the year-over-year CPI inflation rate falling from 4.2 percent in May to 3.5 percent in June, while overall prices declined by 0.4 percent on a monthly basis. Officials may want to see whether that trend continues through the next September FOMC meeting before tightening policy. The Fed will also likely receive some assistance from a planned change in how the BEA calculates the Fed’s preferred inflation gauge, the PCE price index, which may trim a few tenths from the PCE inflation rate this fall. Estimates of second-quarter growth have also weakened. The Atlanta Fed’s GDPNow model currently puts real GDP growth at just 1.7 percent, down from the first quarter’s 2.1 percent pace.

Taken together, these factors make a plausible case for waiting. If inflation falls toward 2.5 percent and real growth slows to roughly 1.5 percent, nominal GDP growth would return to the NGDP growth rule’s 4 percent benchmark by September. Under that scenario, the current policy rate might prove appropriate, and a July increase would look premature.

The problem with this argument is that it assumes too much. The conflict with Iran is re-escalating, and despite energy prices declining from May to June, average gas prices are already pushing back over $4 while diesel prices exceed $5. The Fed should generally avoid overreacting to a temporary supply shock, but it should also be cautious about assuming inflationary pressures will resolve on their own, especially given the uncertain path of the conflict. And while the BEA update may bring the Fed’s preferred inflation rate down slightly, Fed officials should not rely on methodological revisions to deliver price stability. Lastly, even if real GDP growth in the second quarter comes in a bit below 2 percent, NGDP growth would likely still exceed 4 percent without any signs of imminent weakness in the labor market. Overall, if the Warsh Fed is serious about delivering price stability, it’s time to start backing up words with actions.

Words and Actions

Chair Warsh has called for less groupthink and more open disagreement inside the FOMC. Dallas Fed President Lorie Logan may provide an early test of that commitment by making the case for higher rates at the July meeting. With nearly half of FOMC participants projecting at least one increase in 2026, she may find considerable support even if a majority is not yet prepared to act.

If the Fed leaves rates unchanged this week, the September meeting will take on added importance. Another two months of inflation near current levels would make it increasingly difficult for the Committee to reconcile its commitment to deliver price stability with its reluctance to raise rates. The leading monetary rules already indicate that policy is too accommodative. If inflation remains elevated, the Warsh Fed will eventually have to back its promise of price stability with action.

In September 2025, two months before the election, Democratic candidate for New York City’s mayoral Election, Zohran Mamdani, pledged to take on FIFA, the world’s largest soccer federation, with a bold proposal. Celebrating “Game Over Greed,” the campaign sought to end dynamic pricing, the practice of adjusting prices in real time based on market demand and scarcity. Zohran’s petition would made three demands: “No dynamic pricing, Reinstatement of the cap on ticket resales; 15 percent of tickets set aside for residents at a discount.” Much of the discontent among fans came from the fact that FIFA’s ticket pricing would allow seats initially sold for affordable prices to be marked up by thousands. Critics argued that these market practices were another form of price gouging by FIFA, exploiting historically high demand.

Now, with the tournament finished, the debate has intensified among fans and officials. The attorney general of both New York and New Jersey issued subpoenas to FIFA, investigating ticketing practices and citing a 34-percent price hike across all ticket categories. Reports showed that prices for seats at the World Cup Final in MetLife Stadium in the New York/New Jersey area reached new heights. Questions of how to allocate that game’s 80,663 seats among five billion soccer fans invited scrutiny of FIFA’s pricing practices and the broader use of dynamic pricing.

So what is dynamic pricing exactly, and how does it work? Unlike traditional ticketing, where prices are predetermined at a fixed rate regardless of conditions, dynamic pricing uses algorithms to adjust prices based on supply, demand, remaining inventory, and purchase timing. Companies adjust rates based on demand while also allocating scarce tickets to the consumers who value them most (as measured by willingness to pay). For example, if thousands of fans want to buy tickets to a playoff game, teams raise prices in response to stronger demand. It also helps consumers, though, by allowing them to get true market prices for tickets, especially in conditions that might drive down demand, such as a game on a hot Tuesday afternoon or a team performing poorly late in the season. Dynamic pricing allows prices to move (up or down and often both) toward a market-clearing price, as supply and demand change.

Sports teams have employed demand-based and variable pricing models for decades. Teams set their ticket prices in response to team quality, fan interest, market size, and even business concentration. The Yankees, Cowboys, Knicks, Dodgers, and others have capitalized on that flexibility, setting prices based on team success, national branding, and broader economic activity. Sports ticket pricing has long been tied to tiered systems, with dynamic pricing adjusting those tiers in real time based on various indicators.

This is consistent with firms’ expected behavior. In a 2012 study, researchers Shapiro and Drayer examined ticket pricing behavior across MLB teams, accounting for both primary and secondary markets. Their results supported the hypothesis that baseball teams maximized ticket prices, like any other competing firm. MLB teams were responsive to ongoing shifts in demand, adjusting prices based on the strength of the matchup, day of the week, current team success, and seasonal milestones. In other words, teams will use dynamic pricing to gain up-to-date data about demand, maximizing the profitability of each transaction. Both teams and fans discover the market-clearing price. Fans evaluate the opportunity costs and may choose lower-demand games that better fit their budgets.

Critics argue that the World Cup is different, as fans may travel around the world to find themselves priced out at the gate. With a limited number of games and incredibly high demand, few affordable options are available for fans to attend games without spending a fortune. Accusations of “price gouging” view the system itself is flawed, with prices continuing to rise given as evidence that FIFA exploiting its market power at consumers’ expense.

We watched this scenario play out in real time as fans scrambled to purchase tickets to the World Cup final in New York/New Jersey. As defending champion Argentina prepared to take on Spain, Forbes reported an average ticket price of over $11,000 (the highest ever recorded for a sporting event). Few fans could afford to purchase tickets, prompting online backlash against FIFA and dynamic pricing.

No failure of the market is necessary here. Prices are logical consequence of an extraordinarily high demand from fans chasing a fixed supply of seats. Allegations of “price gouging” by corporations, and attempts to fix them with policy, will do little to shift either factor.

(Some attorneys general are investigating allegations involving deceptive practices or broken promises in the ticketing process. Policymakers should distinguish between high prices caused by scarcity and deceptive or fraudulent practices, which are legitimate cause for official inquiry.)

More to the point, Mamdani’s proposal to FIFA to end dynamic pricing for the World Cup would not have “ended dynamic pricing,” but would likely make the problem worse. In fact, banning dynamic pricing would push more ticket sales off official sites and into secondary markets, where scalpers can capture the premium created by scarcity

Imagine FIFA sells tickets to a game at $100 apiece. The game may sell out immediately, with resellers and automated bots acquiring many of the available tickets. In turn, scalpers can charge prices close to or above the market-demand price that fans would have been willing to pay on FIFA’s own site, raking in a large profit margin on each transaction. The swap reduces FIFA’s potential revenue (by $500, if a $100 ticket were resold for $600), gained by the scalper rather than the federation itself. The buyer is no better off.

This may not seem like such a big deal for a global federation or national sports league; however, its effects will be greater on smaller franchises with tighter margins. Local clubs, newer leagues, and smaller venues rely on revenue from high-demand games to subsidize their high fixed operating costs. Stripping them of the opportunity to set prices based on demand may be destructive to many smaller operations.

Perhaps the great irony of Mamdani’s proposal is that even the most well-intended price caps couldn’t reduce what fans ultimately pay. Demand remains unchanged, so some fans still pay the market rate for tickets regardless of the supplier, while others will be priced out, or encounter sellouts or lotteries. What price-fixing policy does is transfer FIFA’s “excess revenue” to a middleman reseller. By widening the gap between face value and resale value (resale premium), the attempted “fix” attracts professional scalpers and bot networks to purchase scarce inventory before regular consumers can access it, forcing them to buy on a less-transparent gray market.

While slogans such as “Game Over Greed” may resonate intuitively, policymakers should carefully consider the unintended economic consequences of restricting dynamic pricing. With states already reviewing bills to ban dynamic pricing across a variety of entertainment industries, alongside outdated or inconsistently enforced anti-scalping laws, these proposals are gaining more traction in mainstream policy debate.

Dynamic pricing does not create scarcity. It exposes it. Banning market prices won’t create more seats in the stadium — it will only change who profits. If policymakers want to help fans, they should allow prices to reflect real market conditions.

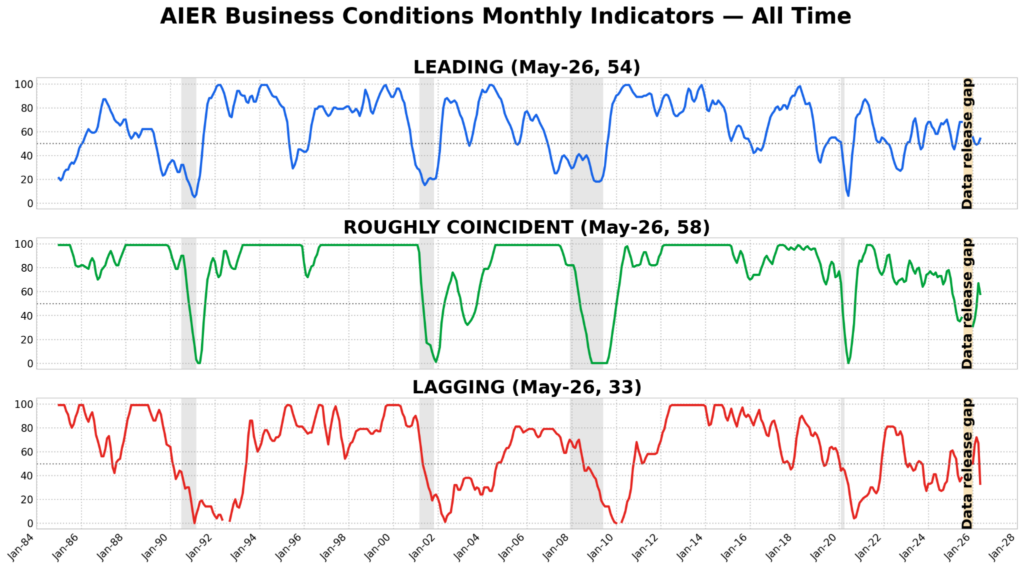

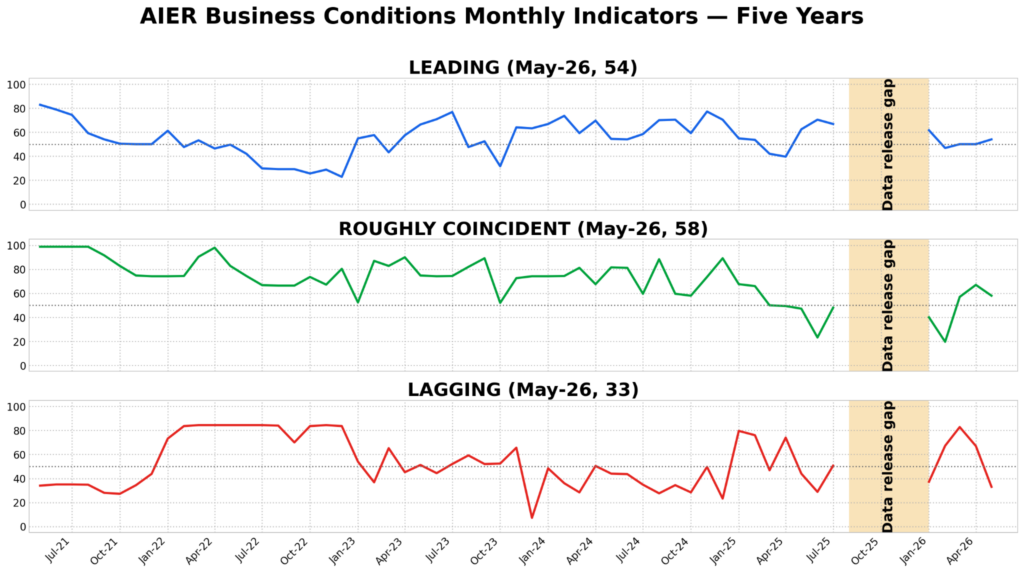

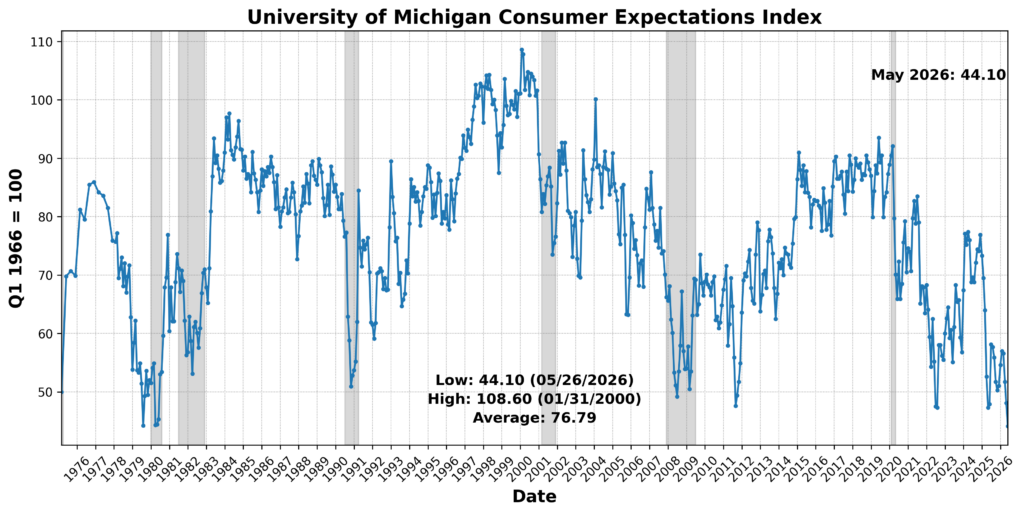

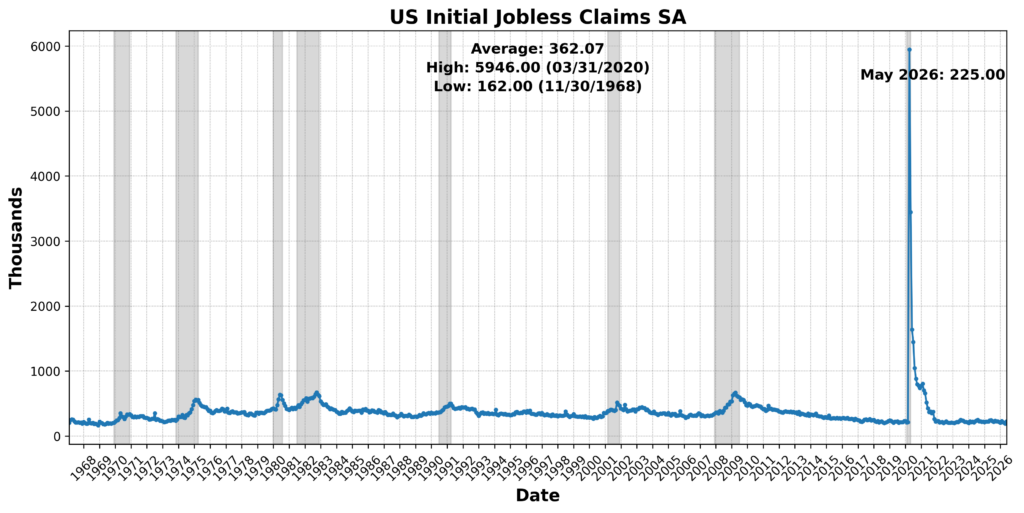

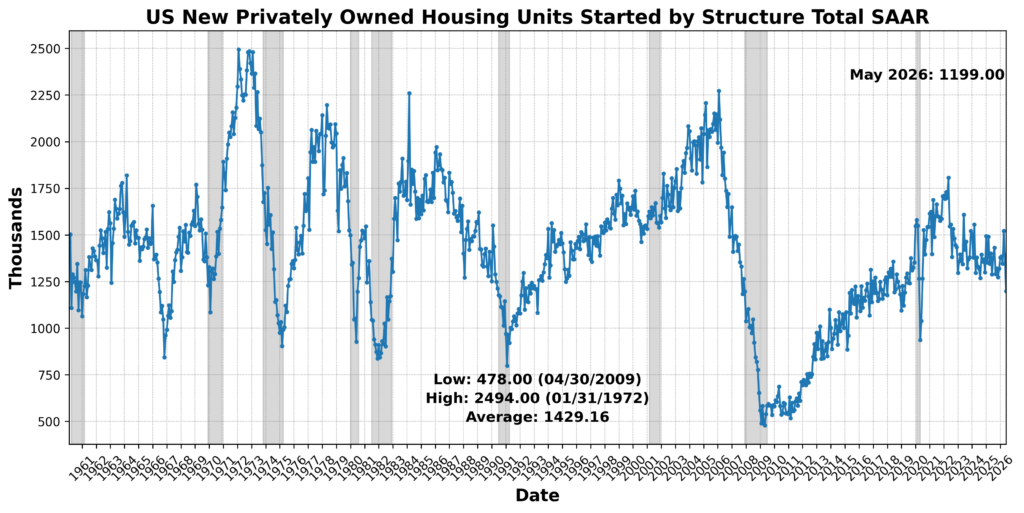

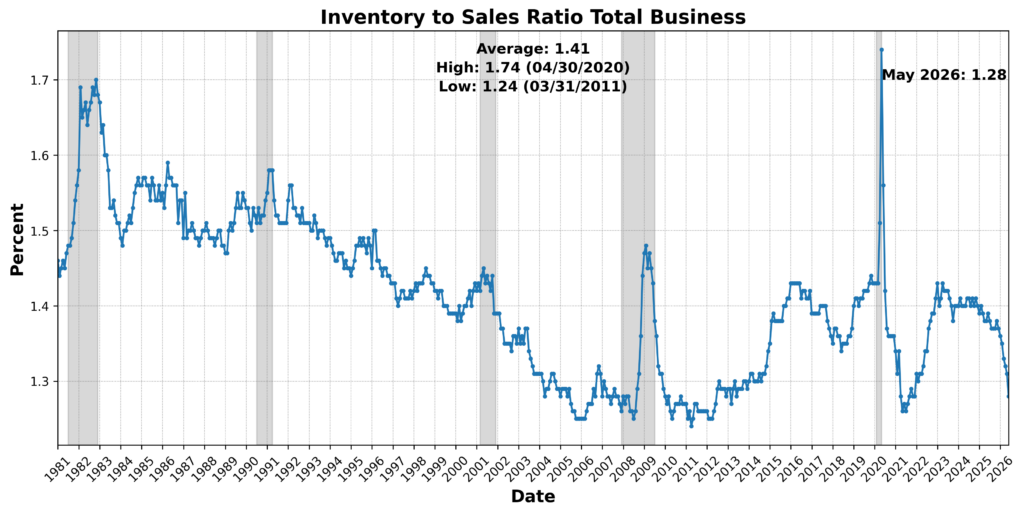

The May 2026 AIER Business Conditions Monthly (BCM) points to an economy that remains mixed, with a modest improvement in forward-looking breadth, a softer read on current activity, and a clear deterioration in lagging conditions. The Leading Indicator rose to 54 from 50, moving slightly above neutral after last month’s evenly split reading. The Roughly Coincident Indicator declined to 58 from 67, suggesting that current activity remains positive but less broadly firm than in April. The Lagging Indicator fell sharply to 33 from 67, indicating that slower-moving measures weakened meaningfully after last month’s more expansionary reading.

LEADING INDICATOR (54)

The Leading Indicator came in at 54, with six of 12 components improving, one essentially unchanged, and five declining.

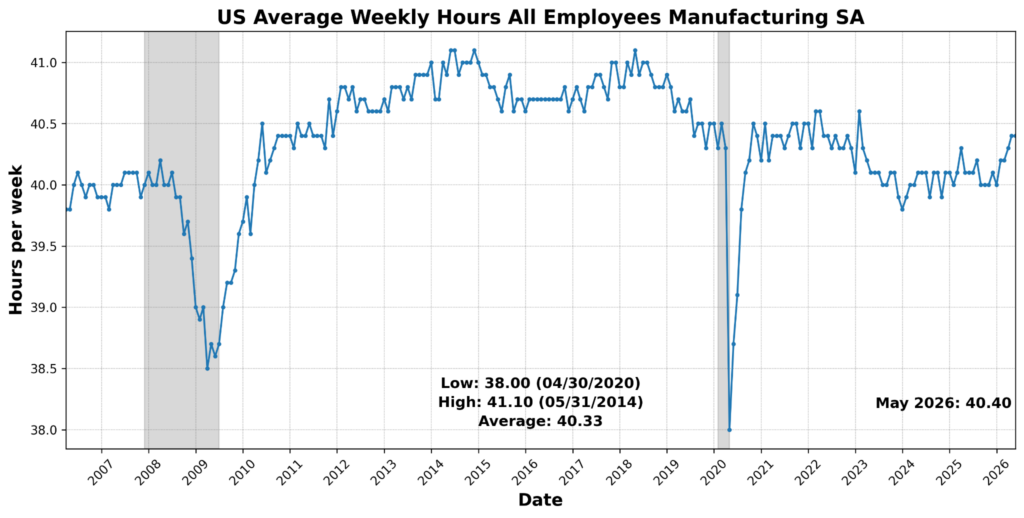

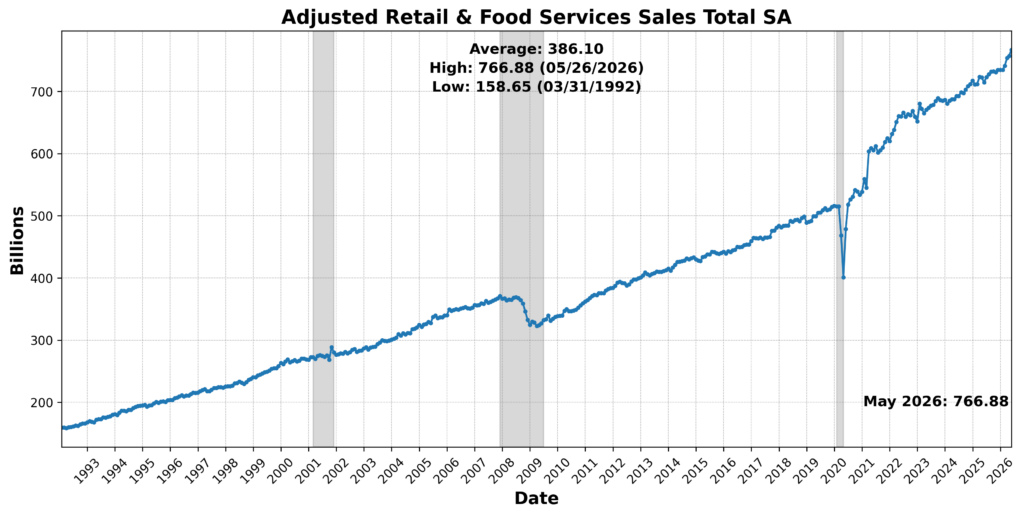

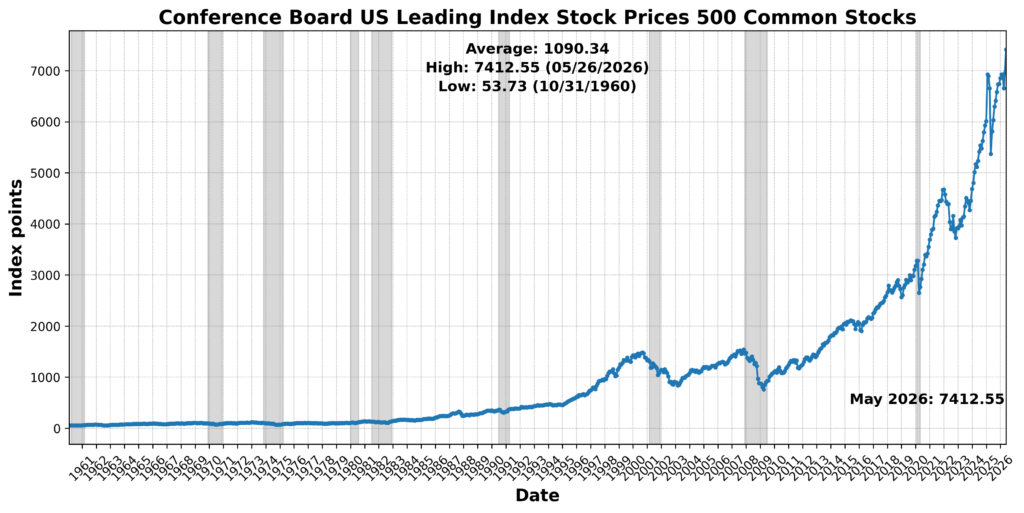

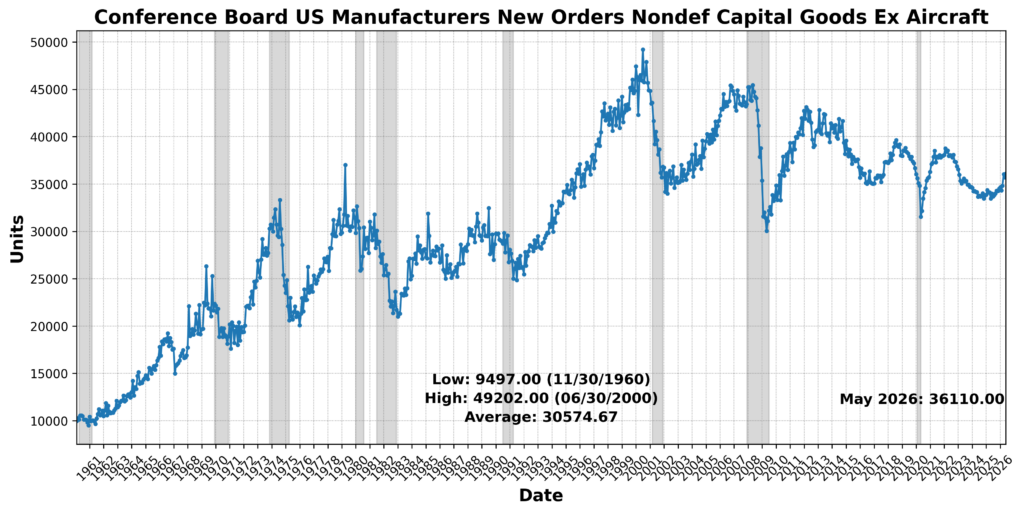

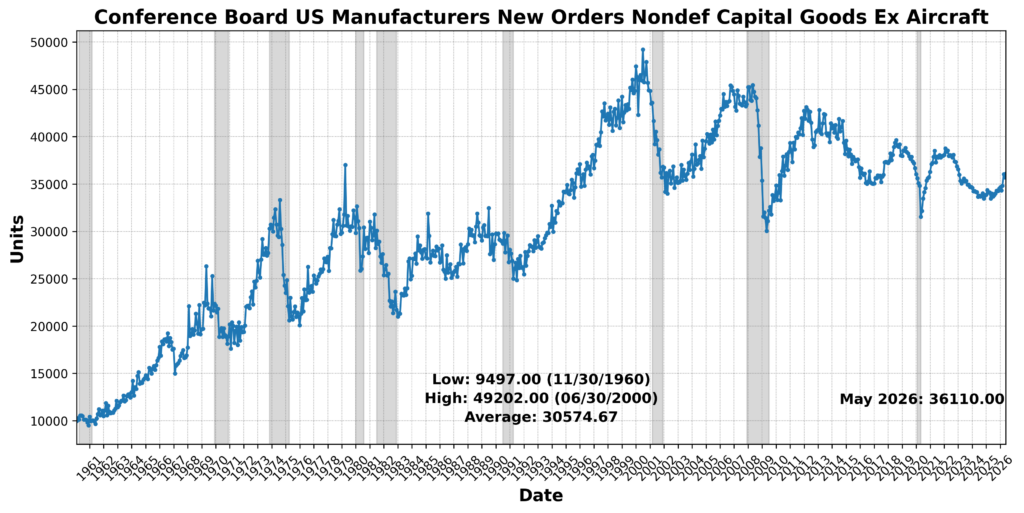

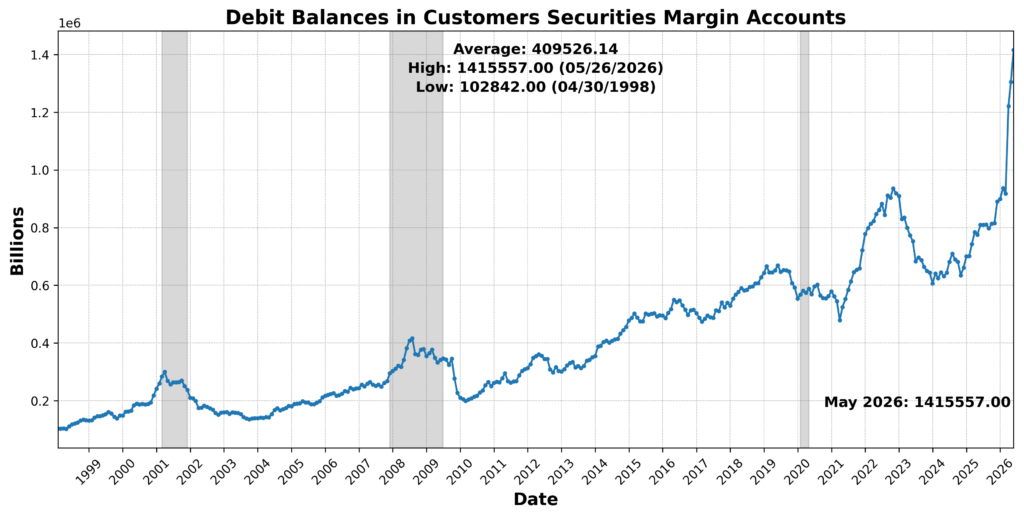

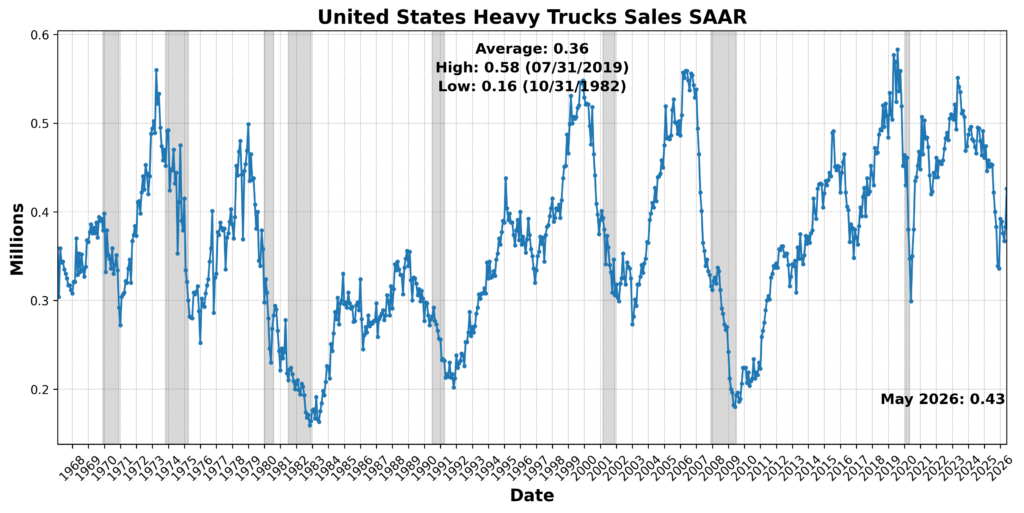

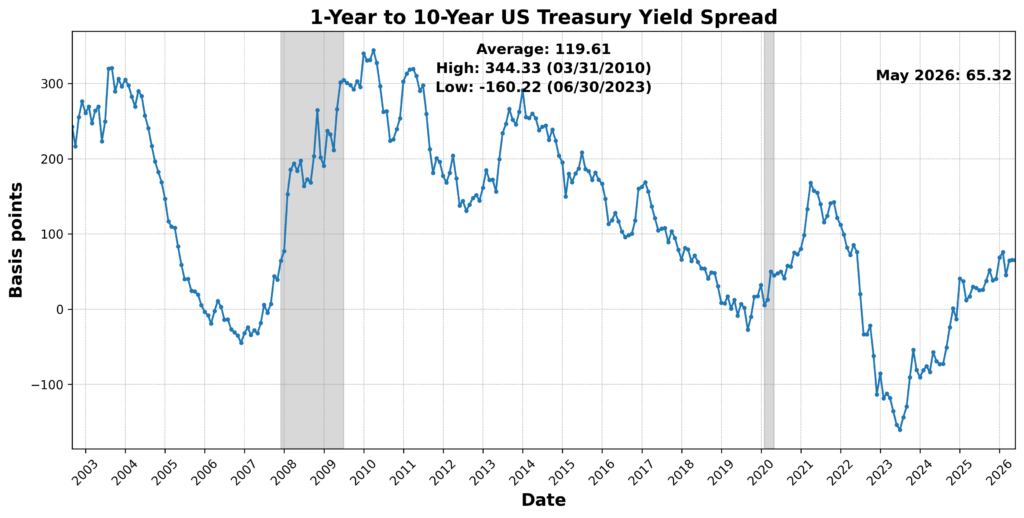

Positive contributions came from a mix of financial-market, demand-sensitive, orders, and yield-spread measures. The Conference Board US Leading Index Stock Prices 500 Common Stocks rose 6.5 percent, while Conference Board US Manufacturers New Orders Nondefense Capital Goods Ex Aircraft increased 1.1 percent. Adjusted Retail and Food Services Sales Total SA advanced 1.3 percent, United States Heavy Trucks Sales SAAR rose 11.2 percent, and Debit Balances in Customers’ Securities Margin Accounts increased 8.5 percent. The 1-Year to 10-Year US Treasury Yield Spread narrowed 0.3 percent and was scored positively after inversion. US Average Weekly Hours All Employees Manufacturing SA was effectively unchanged, contributing neutrally.

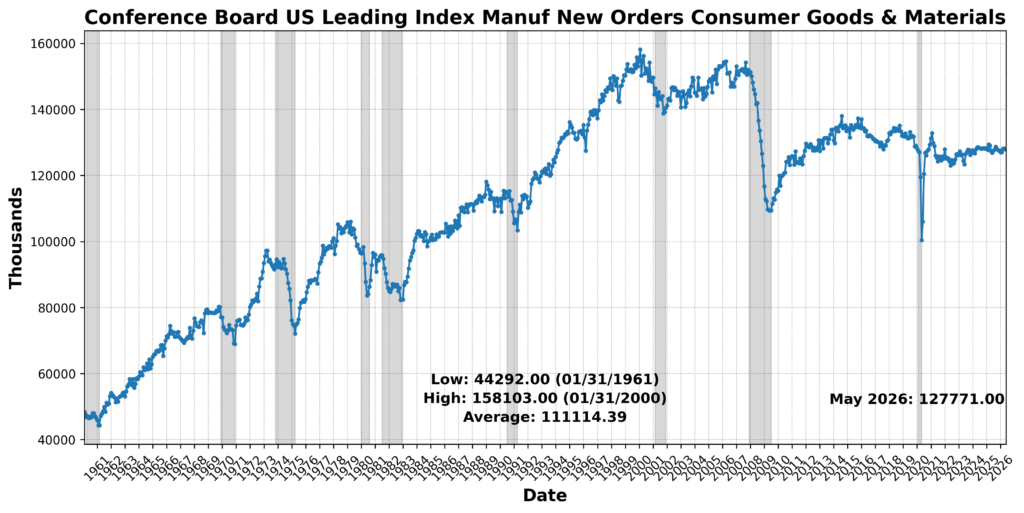

Those gains were offset by weakness in several important forward-looking areas. The University of Michigan Consumer Expectations Index fell 8.3 percent, pointing to another deterioration in household expectations. US Initial Jobless Claims SA rose 18.4 percent and was scored negatively after inversion. Conference Board US Leading Index Manufacturers’ New Orders Consumer Goods and Materials slipped 0.2 percent, while US New Privately Owned Housing Units Started by Structure Total SAAR dropped 13.9 percent. The Inventory-to-Sales Ratio Total Business declined 2.3 percent and, under the BCM scoring approach, was scored negatively.

Taken together, the leading components suggest a forward-looking environment that improved modestly but remains divided]. Equity prices, capital goods orders, retail activity, heavy truck sales, margin debt, and the yield-spread signal provided support, while consumer expectations, initial claims, consumer-goods orders, housing starts, and inventories restrained the index. The rise from 50 to 54 points to a slightly better leading picture than in April, but not a decisive or broad-based acceleration.

ROUGHLY COINCIDENT INDICATOR (58)

The Roughly Coincident Indicator registered 58, with three of six components improving, one essentially unchanged, and two declining.

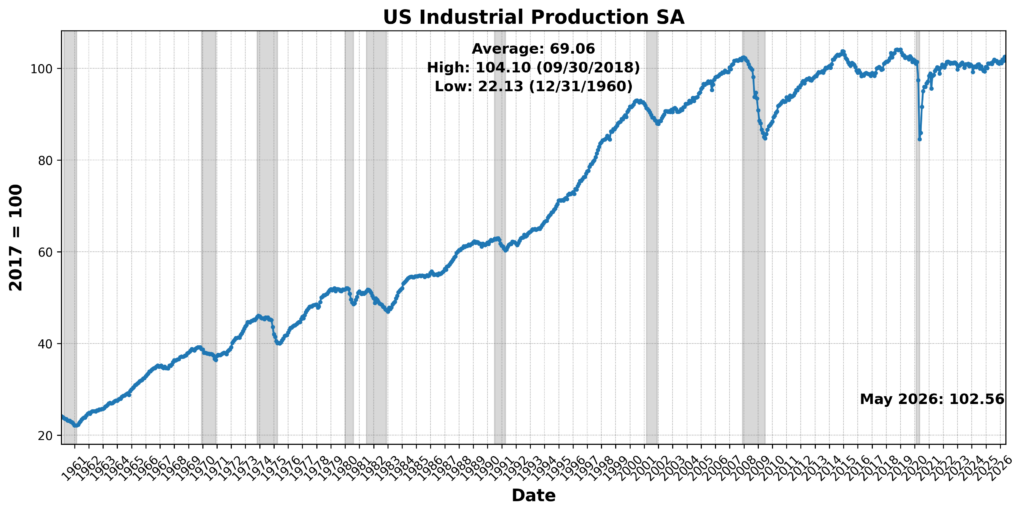

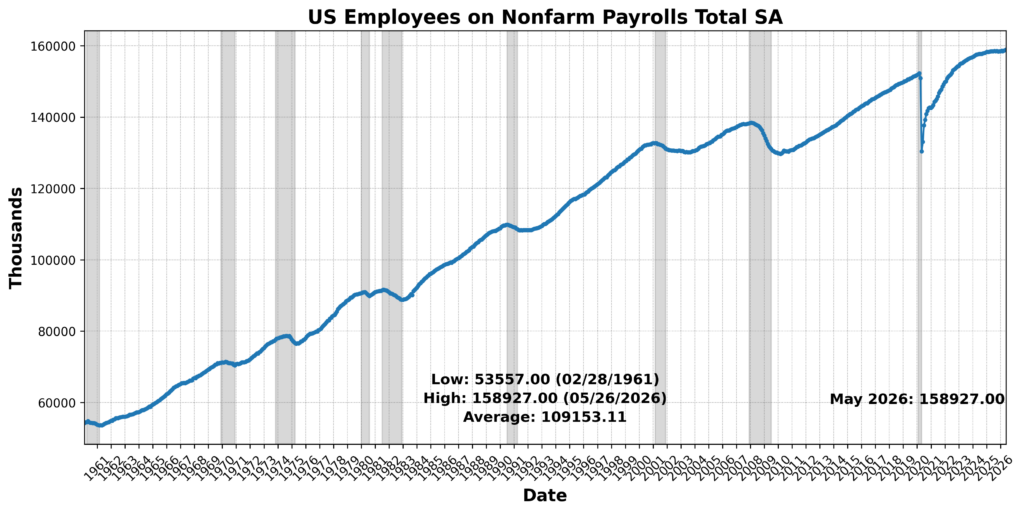

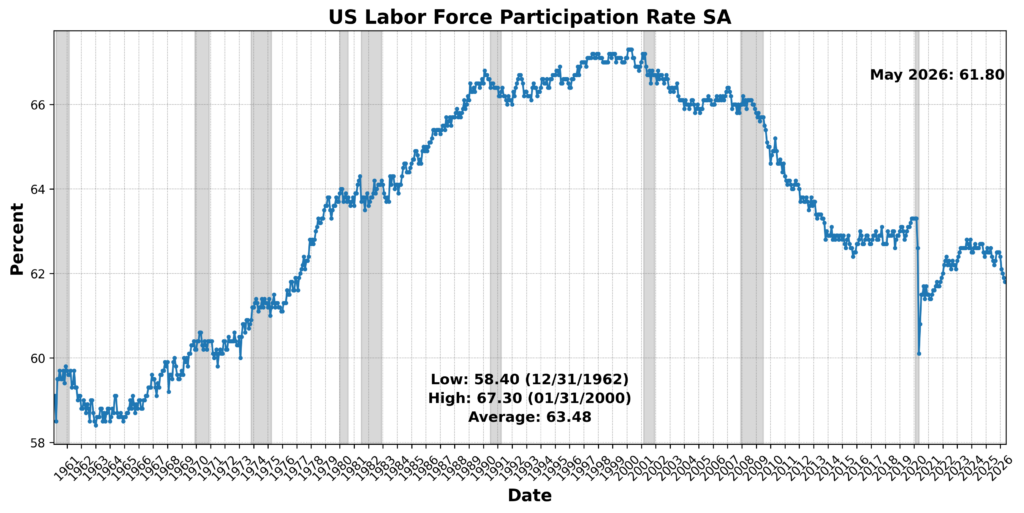

Current activity remained modestly positive, though less uniformly strong than in April. Conference Board Coincident Personal Income Less Transfer Payments rose 0.3 percent. US Industrial Production SA edged up 0.1 percent, and US Employees on Nonfarm Payrolls Total SA also increased 0.1 percent. The US Labor Force Participation Rate SA was effectively unchanged and therefore contributed neutrally.

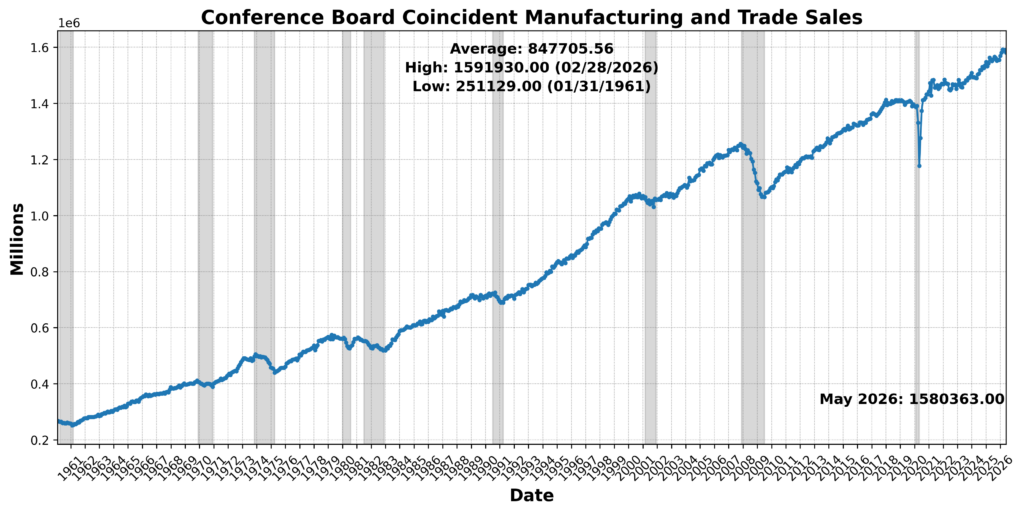

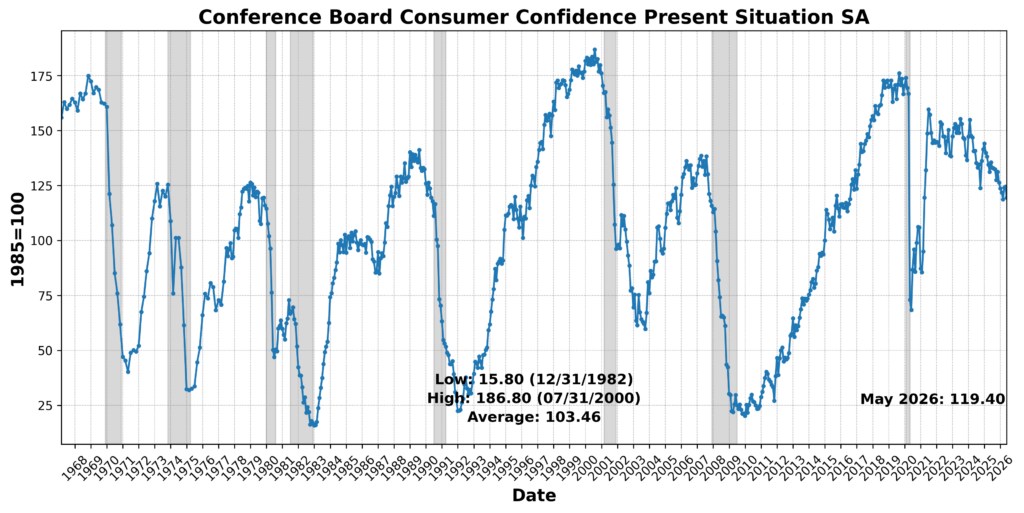

Two components weakened. Conference Board Coincident Manufacturing and Trade Sales declined 0.7 percent, and Conference Board Consumer Confidence Present Situation SA fell 4.0 percent. Those declines suggest that while income, production, and payrolls continued to advance, sales activity and present-situation sentiment softened during the month.

Overall, the roughly coincident data point to continued expansion in current conditions, but with less breadth than in April. The decline from 67 to 58 reflects a cooling in real-time activity rather than a broad contraction. Payrolls, income, and industrial production remained supportive, while weaker manufacturing and trade sales and softer present-situation confidence pulled the index lower.

LAGGING INDICATOR (33)

The Lagging Indicator stood at 33, with two of six components improving and four declining.

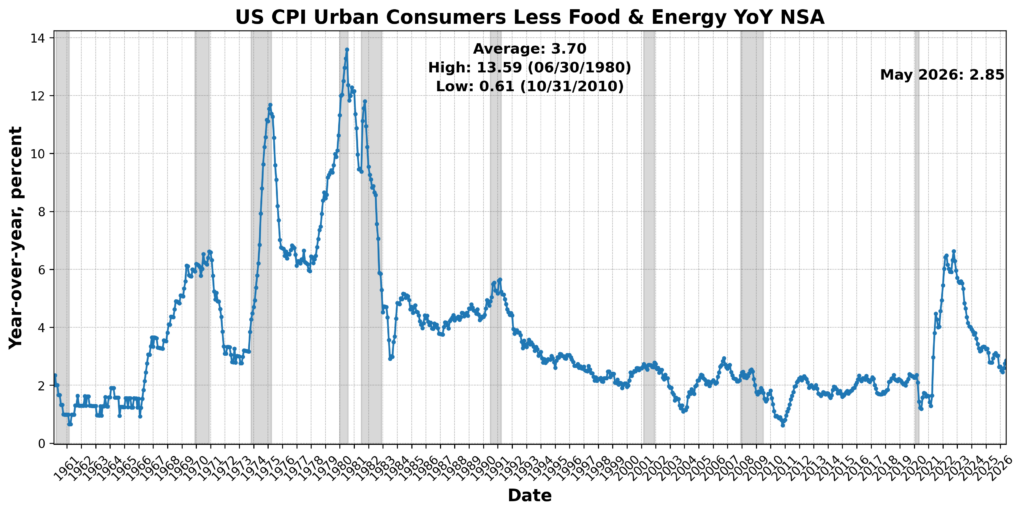

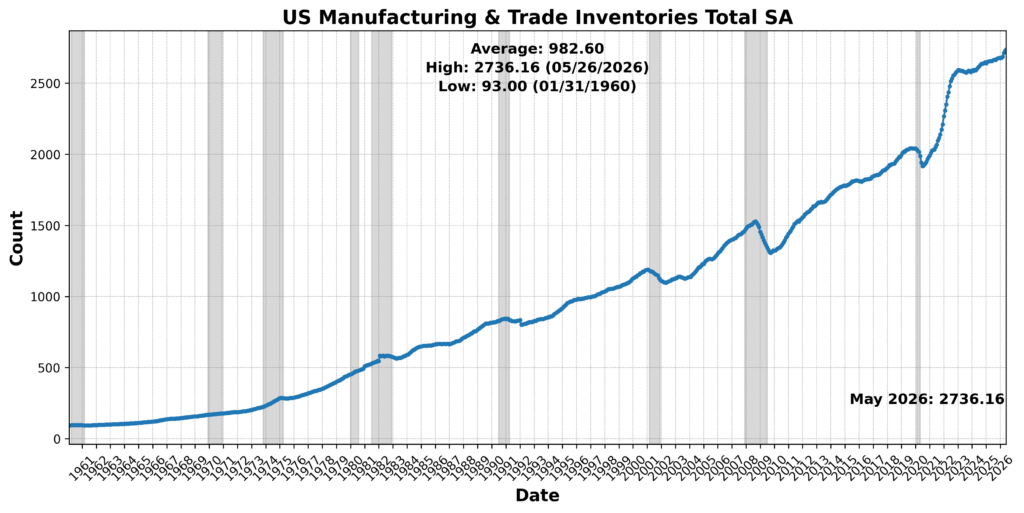

Two slower-moving measures contributed positively. US CPI Urban Consumers Less Food and Energy Year over Year NSA rose 3.7 percent, and US Manufacturing and Trade Inventories Total SA increased 0.4 percent. Those readings provided support from inflation and inventory measures.

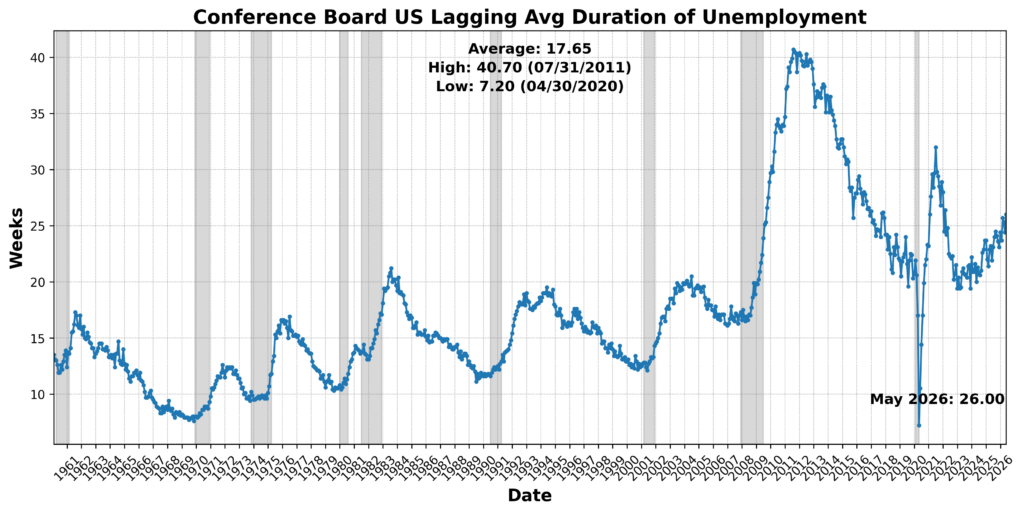

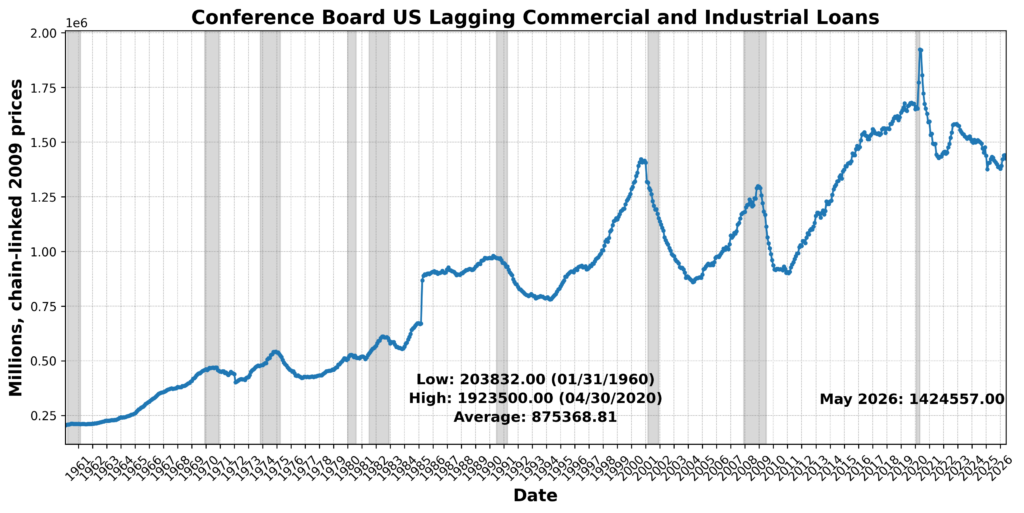

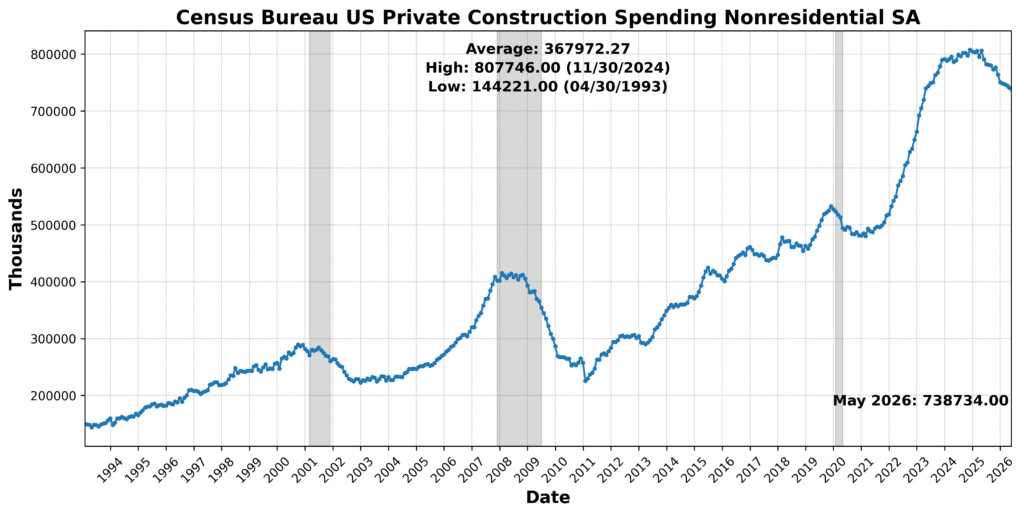

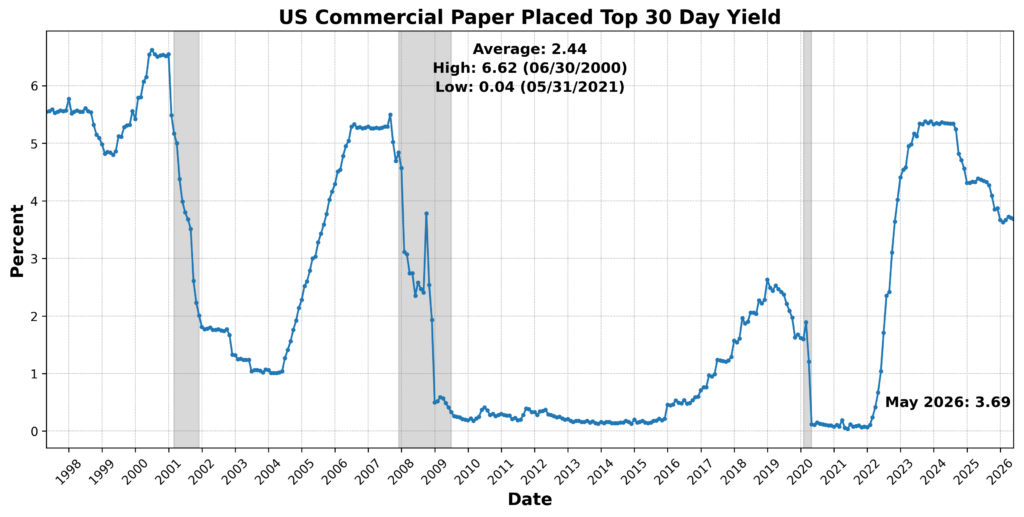

The remaining components weakened. US Commercial Paper Placed Top 30 Day Yield declined 0.4 percent and was scored negatively. Conference Board US Lagging Average Duration of Unemployment increased 6.6 percent and was scored negatively after inversion. Conference Board US Lagging Commercial and Industrial Loans declined 1.1 percent, and Census Bureau US Private Construction Spending Nonresidential SA slipped 0.3 percent. Together, those moves point to softer trailing conditions across short-term credit yields, unemployment duration, commercial lending, and nonresidential construction.

The lagging data deteriorated meaningfully in May. The drop from 67 to 33 suggests that much of the residual strength visible in April’s backward-looking measures faded during the month. While core inflation and inventories remained positive contributors, the broader lagging category turned contractionary, with weakness concentrated in credit, labor-market duration, lending, and construction-related measures.

May’s BCM results describe an economy that is still mixed, but less comfortably balanced than in April. Relative to April, the story is one of modestly better leading conditions, softer coincident momentum, and a sharp weakening in trailing measures — not a broad rollover, but a less reassuring mix than last month.

DISCUSSION (June/July 2026)

Recent inflation data point to a sharp improvement in headline price pressures, but a less decisive easing in the underlying measures most relevant to the Federal Reserve. June’s CPI was substantially softer than expected, with headline prices falling 0.4 percent as gasoline dropped nearly 10 percent, while core prices were essentially unchanged and year-over-year core inflation slowed to 2.6 percent. The improvement extended well beyond energy: shelter inflation moderated, medical services and car insurance declined, airfares barely increased, discretionary services cooled, and core goods prices fell for a second consecutive month, suggesting that most tariff-related passthrough has already occurred and that consumers are increasingly resisting further price increases. The breadth of inflation also narrowed considerably, with fewer than half of core categories rising at annualized rates above the Fed’s 2 percent target. Producer prices reinforced the near-term disinflationary signal, as headline PPI fell 0.3 percent on cheaper gasoline, lower transportation costs, and subdued services inflation, while portfolio-management fees and airfare — important inputs into the Fed’s preferred PCE index — came in below expectations. Upstream pressures have not disappeared, however: core PPI remains elevated from a year earlier, manufacturing inputs are still rising, freight costs remain high, and healthcare prices strengthened. Moreover, May’s PCE report showed that inflation had accelerated before the June energy reversal, with core PCE reaching 3.4 percent as portfolio fees, air travel, and healthcare accounted for much of the increase, while strong income growth and resilient consumer spending reduced the urgency of monetary easing. Taken together, the reports suggest that May likely marked the peak in headline inflation and that lower energy prices, softer goods prices, cooling shelter, and weaker pricing power are restoring disinflation, but persistent service sector and producer side pressures will allow the Fed to maintain a hawkish posture while leaving interest rates unchanged through the remainder of the year.

Recent labor market data continue to portray an economy that is cooling gradually rather than deteriorating abruptly. June’s employment report showed payroll growth slowing to 57,000, with downward revisions to prior months and a narrower breadth of hiring, yet the three-month average remains above most estimates of the pace needed to stabilize unemployment. The decline in the unemployment rate was less encouraging than it appeared, reflecting a sharp drop in labor-force participation — including a notable decline among prime-age workers — rather than stronger hiring, while wage growth remained modest and consistent with easing inflation pressures. Job creation continues to be concentrated in higher skill service industries such as healthcare, professional services, and finance, while consumer-facing sectors including leisure, hospitality, retail, and information weakened. Other labor indicators present a somewhat firmer picture: ADP payrolls and the May JOLTS report point to steady hiring, low layoffs, stable quits, and job openings that remain sufficient to support continued expansion without generating significant wage inflation. At the same time, early evidence suggests artificial intelligence may be beginning to reshape hiring patterns, with employment softening in technology, information, and financial activities through slower hiring and attrition rather than widespread layoffs. Taken together, the labor market appears neither overheated nor recessionary: hiring is moderating, labor demand remains generally healthy, wage pressures are contained, and the combination of softer employment growth and subdued inflation should leave the Federal Reserve comfortable remaining on hold while monitoring whether the recent cooling proves temporary or marks the beginning of a more sustained slowdown.

June’s purchasing manager surveys point to continued but moderating expansion across both manufacturing and services, with demand still solid, supply conditions improving, and cost pressures easing from their recent war-driven peak. The ISM manufacturing index slipped to 53.3 but remained near a four-year high and marked a sixth consecutive month of growth, supported by capital investment tied to artificial intelligence, defense spending, inventory accumulation, and strength across most industries. New orders and production slowed, however, employment remained slightly contractionary, backlogs grew at their weakest pace of the year, and factory commentary stayed cautious amid tariffs, elevated metals costs, stretched lead times, weaker consumer demand, and lingering uncertainty surrounding the Middle East. The most encouraging development was a sharp decline in the prices-paid index as falling oil prices relieved pressure on energy-intensive inputs, although overall costs remain well above early-year levels. Services activity followed a similar pattern: the ISM services index eased to 54.0 as new orders and production decelerated following May’s inventory buildup, but the sector continued to expand, export orders and backlogs strengthened, supplier performance improved, and employment increased. Taken together, the surveys suggest that the economy retains considerable momentum but is shifting toward a slower and better-balanced expansion, with firms still investing and hiring selectively even as demand visibility weakens, inventories rise, and producers remain wary of tariffs, geopolitical disruptions, and persistent input-cost pressures.

Measures of consumer and small-business sentiment improved in early summer, reflecting lower energy prices and growing confidence that economic conditions are stabilizing, though both households and firms remain cautious about inflation and geopolitical risks. The University of Michigan’s preliminary July consumer sentiment index rose to its highest level since February as falling gasoline prices eased pressure on household budgets, inflation expectations moderated, and buying conditions for major durable goods improved. Even so, concerns about the cost of living remained widespread, and because most survey responses were collected before renewed US military action against Iran pushed oil prices higher, some of July’s improvement may prove temporary. Small businesses likewise became more optimistic, with the NFIB Small Business Optimism Index posting its strongest reading of the year as better sales expectations, stronger hiring intentions, and increased capital spending plans pointed to firmer momentum heading into the second half of 2026. Uncertainty surrounding investment decisions declined, supply chain disruptions eased modestly, and hiring plans returned to their long-run average, although labor shortages and inflation remained the most frequently cited obstacles. Taken together, the surveys suggest that lower energy costs have materially improved economic confidence across households and businesses, but persistent inflation concerns, labor constraints, and the risk of renewed energy-price shocks continue to temper the outlook.

The FIFA World Cup appears to have provided a meaningful, if temporary, boost to US consumer spending in June, with its effects likely to become more evident in the Bureau of Economic Analysis’ personal spending report due July 30. Host cities experienced stronger restaurant traffic, as reflected in OpenTable reservation data, while retailers also benefited: Amazon moved its Prime Day promotion into late June to coincide with heightened consumer engagement during the tournament, supporting online merchandise sales. The event also fueled unprecedented sports betting activity, with more than $5 billion wagered through prediction markets such as Polymarket and Kalshi, record June betting volumes in New Jersey, and sharp increases in wagering in New York. However, that surge may not translate into stronger measured consumer spending because the BEA records gambling expenditures as net gaming revenue rather than total wagers, and early state data suggest casino and sportsbook revenues softened despite higher betting volumes. Taken together, the World Cup likely lifted June consumption primarily through hospitality and retail spending rather than gaming, contributing to an estimated 0.4 percent increase in nominal personal spending (roughly 0.5 percent in real terms) while providing a modest but noticeable tailwind to overall consumer demand.

Building on signs of resilient consumer demand, June’s industrial production report painted a somewhat softer picture on the supply side, although it appears weaker than many other indicators would suggest. Industrial output rose just 0.1 percent, with factory production essentially flat as declines in most durable-goods industries offset gains in computers and electronics, household appliances, transportation equipment, and several nondurable categories including food, apparel, printing, and energy products. Business equipment production weakened, though oil and gas drilling and utility output continued to expand. The report stands in contrast to stronger ISM manufacturing surveys, improving manufacturing employment, and other measures pointing to healthier factory activity, suggesting that June’s production figures may understate underlying momentum rather than signal a meaningful deterioration. Even so, while continued investment in artificial intelligence, defense, and industrial infrastructure should support demand for capital goods and durable manufacturing over the coming months, the evidence still falls well short of indicating the broad-based manufacturing renaissance that some observers have anticipated.

The Federal Reserve’s latest Beige Book largely reinforced the picture emerging from recent economic data: growth continues at a modest pace, inflation pressures are gradually easing, and policymakers have little reason to alter their current stance. Business contacts across most districts reported slightly improved sentiment, supported by lower fuel prices, resilient consumer spending, including a boost from World Cup-related tourism in some regions, and continued strength in manufacturing tied to artificial intelligence, data centers, machinery, and defense. Labor markets remained generally healthy, with employment expanding modestly despite persistent shortages of skilled workers in technical and trade occupations. Price pressures also moderated, as every district reported inflation that was either unchanged or slower than in the previous survey, although expectations for future inflation remained mixed amid uncertainty surrounding energy markets and geopolitical developments. Overall, the Beige Book suggests an economy that continues to expand without significant overheating, providing further support for the Federal Reserve’s strategy of maintaining a cautious, mildly hawkish posture while leaving interest rates unchanged as it awaits clearer evidence that inflation is moving sustainably back toward target.

Attention now shifts to the July FOMC meeting, where officials are widely expected to leave interest rates unchanged despite lingering concerns over inflation and renewed geopolitical risks stemming from the lengthening and increasingly unpredictable conflict with Iran. While softer June inflation data and easing energy costs before the latest oil price rebound strengthen the case for patience, policymakers are also likely to scrutinize incoming GDP, personal spending, Core PCE, employment costs, and consumer confidence data for evidence that resilient consumer demand and continued AI-driven investment are not rekindling underlying inflationary pressures. The result is a policy outlook that remains finely balanced: the Fed appears comfortable staying on hold for now, but is unlikely to signal an imminent easing cycle until disinflation becomes more firmly established.

In the aggregate, recent economic data suggest the US economy continues to expand at a moderate, more sustainable pace rather than sliding toward recession. Inflation is easing, labor markets remain resilient despite slower hiring, and business activity continues to grow, supported by AI-related investment and steady consumer spending. While geopolitical risks, elevated services inflation, and lingering producer-price pressures warrant caution, the overall picture is one of continued expansion with gradually cooling inflation: conditions that should keep the Federal Reserve on hold as it awaits further evidence that price stability is being restored.

Early corporate earnings reports reinforce that cautiously optimistic outlook. An alternative, real-time gauge of economic activity generated by Bloomberg and based on whether S&P 500 companies exceed sales expectations has produced one of its strongest early readings since 2015. Twenty-nine of the first thirty-one reporting firms surpassed revenue forecasts through July 22. Because firm revenue growth provides a cleaner measure of underlying demand than earnings (which can be boosted by cost-cutting or financial engineering) the unusually broad strength in sales suggests second-quarter GDP may ultimately exceed current consensus forecasts by roughly a quarter of a percentage point. The sample remains small and should be interpreted cautiously, but the early earnings season adds to a growing body of evidence that consumer demand, business investment, and overall economic activity were firmer in the second quarter than many economists had anticipated, which in turn reinforces the case for continued economic expansion alongside a Federal Reserve that remains comfortably on hold.

In Edgar Allan Poe’s classic short story The Purloined Letter, a group of investigators search tirelessly for a stolen letter containing information that could be used for blackmail. They conduct elaborate searches and speculate endlessly about where the letter could be hidden, only for detective C. Auguste Dupin to find it hiding in plain sight on a card rack.

The story mirrors how policymakers often respond to problems: crafting elaborate policies while overlooking simpler solutions that may be hiding in plain sight.

As geopolitical competition with China and conflicts across the world highlight shortcomings in America’s defense industrial base and vulnerabilities in its supply chain for rare earth minerals, industrial policy has become fashionable on both sides of the aisle. Whether it’s the subsidies included in President Biden’s signature CHIPS and Science Act or President Trump’s sweeping tariffs, leaders of both parties seem willing to enact costly, distortionary measures to rebuild America’s industrial base and sever dangerous dependencies.

While it is worth discussing the merits and drawbacks of these policies, there are more straightforward ways to strengthen America’s industrial capacity. One of the most important is permitting reform: improving the way infrastructure, manufacturing, and mining projects are approved. If implemented impartially, permitting reform could enable entrepreneurs to respond more rapidly to America’s security needs and unleash the country’s industrial potential.

In order to get a project in mining or manufacturing approved, one must navigate a sprawling web of (frequently overlapping) regulations and get approval from a multitude of state and federal authorities. Agencies can often retroactively veto already-approved projects (if they get around to the approval decision at all), and the lengthy process opens up opportunities for interest groups to shoot down projects they oppose through litigation.

Former National Security Advisor Jake Sullivan summarized America’s permitting challenges well when he argued, “Too many people possess the power to say no. Too few are empowered to say yes.”

Permitting reform tackles this issue head-on with measures like reducing redundant permission requirements, modernizing legal processes, eliminating retroactive veto power, and setting strict timelines for regulators to reduce delays and uncertainty.

As it stands, mining projects critical to America’s industrial needs are often bogged down by extensive permitting requirements. A report from S&P Global found that the average lead time — the gap between mineral discovery and production — for mines worldwide has increased from about six years in 1990 to nearly 30 years today. Permitting delays frequently push projects back by years or cause them to be cancelled altogether. For the United States to access its abundant reserves of rare earths and eventually reduce its reliance on Chinese supply chains, the permitting process must be reformed.

These problems plague manufacturing as well. One study examining permitting and microchip production noted that “permit notification and review processes can impose delays of weeks, months, or even years. In the presence of competition, delays threaten to erode slim technological and marketing leads.” This echoes broader economic research showing that extensive regulation impedes capital investment and reduces industrial efficiency and competitiveness.

If the process for approving projects were simplified and streamlined, it would empower miners, manufacturers, and entrepreneurs to respond more effectively to demand for critical minerals and improvements in America’s industrial base. A mistake many proponents of state-directed industry make is underestimating the ability of markets to respond to national security priorities. Record private investment in defense manufacturing demonstrates that markets can identify strategic needs and allocate capital accordingly. Effective permitting reform would allow those investments to become finished projects more quickly.

As America’s industrial and infrastructure needs continue to take center stage, policymakers will inevitably face pressure to take an ad hoc approach to permitting reform, allowing favored projects to move through the process more quickly while others remain stuck. Recent permitting exceptions for data centers in Utah and Wyoming, as well as streamlined permitting efforts for rare earth mining, illustrate this tendency.

If lawmakers continue this piecemeal approach, they risk making themselves the kingmakers of industrial policy. An abundance of economic research suggests that government favoritism in industry has a tendency to distort markets, impede competition, and create destructive incentives for rent-seeking among government officials.

More immediately, government favoritism is already hindering broader permitting reform efforts that could provide a genuine boost to American industry. The bipartisan SPEED Act, a bill that streamlines legal processes for industrial projects, faces an uncertain fate in the Senate after being passed by the House of Representatives, as many democrats remain hesitant to embrace broad permitting reform while the Trump administration weaponizes regulatory power to block clean energy projects.

Given the bipartisan momentum behind permitting reform, this should be the moment for a historic compromise. Reform could allow manufacturers, miners, and energy producers to address America’s strategic and economic needs more quickly and effectively.

Americans should ask themselves, like detective C. Auguste Dupin did, whether a solution is hiding in plain sight. If analysts, journalists, and the public paid as much attention to permitting as they do tariffs and subsidies, it could build momentum for policymakers to prioritize the issue and finally unlock meaningful change.

Every few years, Americans rediscover Scandinavia.

Someone visits Norway or Denmark, returns dazzled and envious of parental leave and universal childcare, and asks why America refuses to copy what obviously works. On the day dedicated to celebrating America, Nicholas Kristof, a Pulitzer Prize-winning journalist, wrote for The New York Times that America is so great that, in fact, it should be more like Norway. If American companies can pay high wages and generous benefits to workers there, Kristof observed, they could do so in New York, too.

If only America were willing to embrace a little more social democracy and bigger government, this popular and recurring story goes, perhaps it could enjoy the same prosperity and flourishing that Norway does — and have its population also routinely rank among the happiest on the planet.

I was born and raised in one Nordic country, have worked in another, and for the last six years have lived in a third, so I’m fairly familiar with our way of life. I’ve also spent much time in America, stunned and enamored of the way things are in the vast, diverse, and unruly union of states. Europeans are simultaneously fascinated and bewildered by America.

Plenty of things are amazing about these United States, and quite a few things awful about the Nordics; I suspect American intellectuals, dreaming about Norway without understanding its nature and tradeoffs, overlook both.

“You Want Security, Health Care and the American Dream? Look to Scandinavia”

Norwegian workers certainly have higher wages than those in many European countries, including those of its fellow Scandinavians. Hotel cleaners, retail clerks, and construction workers often earn salaries that surprise visiting Americans. Thanks to Baumol’s cost disease, decades of well-managed petroleum wealth have pushed up industrial and service wages.

The first thing an American professional moving to Norway would notice isn’t the generous parental leave, but the great loss of disposable income and material well-being. Norwegians households average 30 percent less disposable income than those the US, and the cost of everyday items is much higher.

The Scandinavian bargain might look like free services, but it as tradeoff: more public goods, fewer private goods.

When American politicians or intellectuals promise Nordic welfare states, most people imagine this happening automatically or by taxing the rich, and everybody benefits. That’s not the case. The real Nordic model taxes earners more (45 percent in Denmark, 40 in Norway, 41 in Sweden, compared to 25 percent in the United States) and charging flat value added tax (VAT). Broad welfare states require broad tax bases; Nordic welfare states are financed not by billionaires but by ordinary workers. The “free” benefits are bought with invasive and regressive consumption taxes (up to 25 percent), payroll taxes, and income taxes that reach well that begin after just $10,000 (the first $16,000 is tax free in the US).

An American professional, pocketing the median earnings of about $65,000, would pay over $17,000 in Norwegian income taxes (compared to about $5,000 per the IRS calculator, naturally subject to state taxes and various deductions), with the employer forced to chip in another $9,200 for the privilege of merely hiring her. From what’s left over, she faces a high cost of living and sales taxes between 11 percent and 25 percent.

Were she in Sweden, a much poorer country with wages well below Norway’s, our middle-of-the-road American professional would land herself in the top 20 percent of earners — though not yet triggering the top 53 percent (or 64 percent) marginal tax rates.

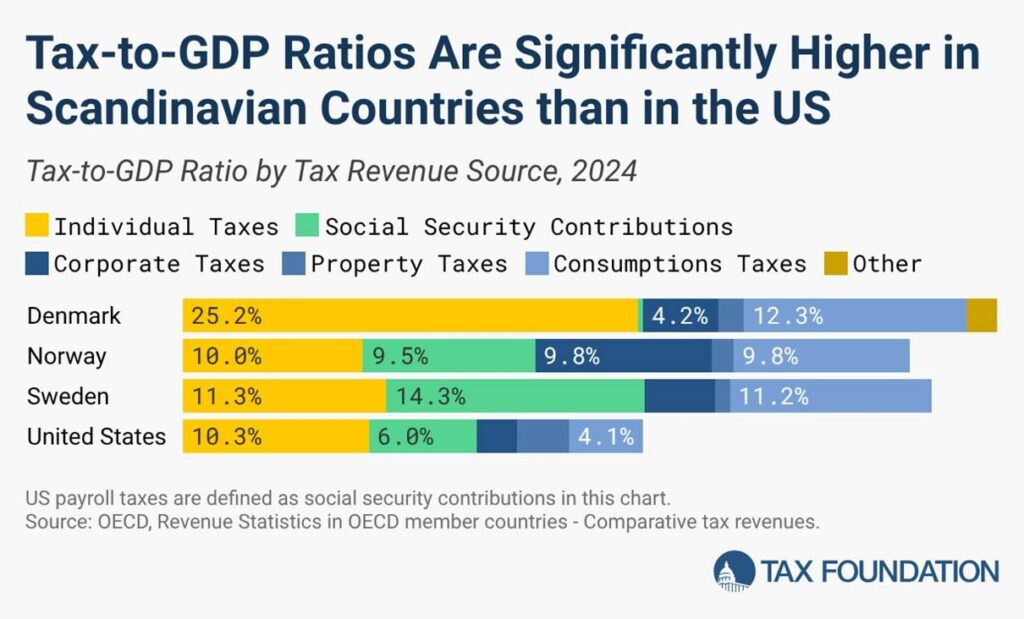

For the Tax Foundation, Cristina Enach summarized, “In 2024, Denmark’s tax-to-GDP ratio was 45.2 percent, Norway’s was 40.2 percent, and Sweden’s was 41.4 percent. This compares to a ratio of 25.6 percent in the United States.”

Some of that difference is accounted for by healthcare spending (private, not government) and pension contributions (401(k) or other retirement accounts) and other personalized options. The Nordics give you one option: the state.

In return, yes, our hypothetical expat would receive subsidized childcare, education, paid time off, and health care. Those services would be of dubious quality, with waiting times stretching into months even for life-threatening conditions. For some, that’s a trade worth making, but it’s not obviously superior, as economist Noah Smith concluded in his comparison a few months ago.

Inequality is indeed lower in Norway, where a person in the top 10 percent earns just three times as much as a person in the bottom 10 percent. That means there’s less reason to strive, less room to grow. Looking to the future, investments in growth, employment, and AI-fueled opportunities are far more attractive stateside than in stagnating Scandinavia. Suppressing growth at the top has suppressed everyone’s potential.

The Norwegian Story Isn’t the Nordic Story

The gap between the average person’s wellbeing in America and that of almost all European countries has widened dramatically over the past three decades. In income per capita, the United States has steadily pulled away from Europe over the last thirty years. The United States’ average income now exceeds every EU member except Luxembourg and Ireland. Citizens of fourteen EU nations earn less on average than residents of even the poorest state: Mississippi, and the EU as a whole ranks between Oklahoma and Maine.

Joseph Sternberg’s opinion piece in the Wall Street Journal earlier this year is illustrative: both Americans and Europeans are shocked when they learn how much materially better off America is. “Politically, bliss is ignorance,” concluded Sternberg. “European welfare states, by creating relatively comfortable lives for voters, conceal the full extent of Europe’s prosperity gap.”

Norway is an affluent country by European standards, but only average compared to America as a whole. Rough figures indicate that Americans, on average, enjoy material economic abundance on par with Iceland and Norway,but are 20 percent to 60 percent better off than the other Nordics. (The difference between the economic outliers and the other Nordics is the difference between New York State and Michigan.) While there are nuances in life, politics, and economics between the five Nordic countries, it’s not like the tax rates, labor economics, public schooling, the overall welfare state, or the generosity of parental leave are that different.

It’s no accident that Kristof reported from Norway; had he run this comparison with Sweden or Finland, the economic outcome would have been so unacceptably low that few Americans would be persuaded by the promise. People in the Norwegian and Icelandic success stories are significantly richer than the other Nordics. Even adjusting for purchasing-power-parity numbers via the University of Groningen-Penn World Table data for 2023, Americans are still a comfortable 15-20 percent richer than most Scandinavians.

It’s Impossible Anyway, So Why Are We Dreaming?

The most immediate sticking point to inflated dreams about the Nordics is that nobody has figured out a way to effectively translate and recreate social and economic institutions elsewhere. To say nothing about a population’s values, behaviors, and traditions.

Institutions emerge from particular and path-dependent histories. They’re not IKEA furniture to merely ship across an ocean and assemble at home. Academic or political observers often make the mistake of thinking you can just isolate a few desirable behaviors or economic institutions, retrofit them onto America, and effortlessly create better lives here.

Plus, America has long tolerated — indeed celebrated — a remarkable degree of eccentricity and ambition. Americans start improbable companies in garages, and they love their “weirdos.” When they do things, they (over)do them properly — SpaceX. College football. Time Square. Las Vegas. Whatever you’re interested in or passionate about, some all-American oddball has built a community for that. It’s a nation of inventors and obsessive animal lovers. They build Burning Man in the desert and whole cities at sea. Their wide-open spaces connect a web of places-as peoples-as-philosophies: Hollywood, elite universities, Silicon Valley and Broadway, Nashville and Detroit, Amish meeting houses and evangelical megachurches, Hindu temples and Highland games from coast to coast. Our great hybrid culture thrives on liberty, not just lower taxes. Our cultural inheritance is the result of having astonishingly many different attempts thrown at the American wall to see what sticks.

The Nordics don’t have that. With the recent exception of fintech and startup wonders (riding on an early, high-tech boom from the ‘90s), trying new, eccentric things in those cold lands isn’t exactly welcome. The Scandinavian idea of Jantelagen, the expectation that nobody should think themselves special, results in a lack of opportunities and a disregard for novelty that most Americans see as both rude and discouraging.

The political equilibrium keeping Scandinavia afloat was, until recently, a mostly homogenous population on sparsely populated lands eerily willing to subjugate individual preferences and quirks to common, collective rules. America stands out in the exact opposite way: letting 15 times as many people pursue radically different lifestyles and individual ambitions with cheerful respect, but little regard for whether the neighbors approve.

Even if it were possible to transplant Norwegian economic and political institutions onto America, how can we be confident we won’t have a Swedish-level economic debacle instead of the wealthy, comfortable Norway a social reformer might dream of?

We can admire and learn from Scandinavian countries using the “Nordic Model,” which have achieved robust social programs without sacrificing too much in the way of economic prosperity. That balance is fragile, and might not work forever: immigration troubles, stagnating growth, and an overbearing regulatory state are exposing the cracks.

Scandinavia has built wildly successful societies for a few million very similar-minded people. But the United States has built something more impressive: a vast, messy republic of economic and social flourishing where hundreds of millions of people peacefully pursue wildly different visions of a good life.

Becoming more like Norway means becoming less American, with less of the opportunity, ingenuity, and the entrepreneurship that made America great.

The Trump administration finalized new Section 301 tariffs on dozens of trading partners, ranging from 10 to 12.5 percent, perfectly timed to take effect as the temporary global tariff of 10 percent under Section 122 expires. The basis for these new tariffs is a five-month investigation into whether those countries have done enough to keep goods made with forced labor out of their supply chains.

There has been plenty of coverage on this. Ilya Somin lays out why this action is likely illegal and runs afoul of Section 301’s own requirements as well as the major questions and nondelegation doctrines. Scott Lincicome argues, powerfully, that the investigation itself was a sham, with the outcome promised early and repeatedly by several members of the administration well before the investigation was completed.

But there’s a far worse outcome from this that cannot be undone by courts, elections, or policy reversals. These new tariffs and their justifications have only served to further destroy the relationships with allies and trading partners that we had previously taken as given. The costs of this will outlast every tariff schedule, court ruling, and this administration. They won’t show up on BLS reports, BEA analyses, or Fed surveys. But they will be felt by every single American for years to come.

As a result of these tariffs, Japan, South Korea, and Australia now face 12.5 percent tariffs for their alleged complicity in using forced labor. China is in the same boat. Three of our closest allies are now accused of being just as negligent about slave labor as China.

Canada, the European Union, the United Kingdom, and Mexico now face 10 percent tariffs for their alleged forced labor practices. Canada and Mexico are, of course, also parties to the USMCA, a trade agreement that this very president negotiated, signed, and called “a colossal victory” only to then walk away from. That same week, the President hit Canada with an additional 50 percent tariff on goods ranging from “wine to hockey sticks to cement” regardless of whether or not those goods qualify under the USMCA.

So in the span of a week, the White House effectively told Canada, our closest trading partner and ally, that America’s word means nothing and then told them that they are complicit in forced labor.

An ordinary tariff is a tax. Trading partners are annoyed, sometimes retaliate, and sometimes negotiate. These tariffs are different. We didn’t just tax Japanese goods. We announced to the world, as an official finding of the United States government, that Japan is profiting from slavery and needs to be punished for it. Norway, Switzerland, Australia, the United Kingdom, and South Korea are guilty of this, too. Then we set a penalty that just so happens to approximate the Section 122 tariffs that just expired.

Foreign officials must now contend with an even clearer reality: not only is an agreement with the United States not worth the paper it’s printed on, but we will accuse you of horrendous practices if it means that an administration can re-impose tariffs. Our trading partners saw that the findings of investigations will be written to fit the desires of an administration instead of the facts on the ground. They learned that not only is America protectionist but that they will publish a serious moral accusation against a friend when doing so is politically convenient.

This changes how other countries will deal with us going forward.

Consider what a foreign trade minister in Tokyo or Ottawa does next. Obviously, over the coming days, they will be releasing press statements. But over the following years, two things become obvious. First, an agreement with the US is never a settled matter. Second, compliance with the American findings buys nothing because the US Trade Representative did not issue any guidelines of what sorts of labor practices could be adopted to lift these tariffs.

If nothing you do can get you off the list, there’s no reason to try. And if no trade agreement is actually binding, there’s no need to come to the table. Instead, there is every reason to find new trading partners.

That work is already happening. The countries hit by tariffs this week have been signing agreements with one another, expanding trading blocs that do not include the US, and diversifying supply chains away from the American market. Every one of those deals is a small, but largely permanent move away from doing business with America. Factories being built in Europe, China, and India won’t be picked up and moved if the US suddenly reverses its tariff policy. These lost opportunities won’t show up in BLS reports, BEA analyses, or Fed surveys.

The impacts of these tariffs and the accusations they come with aren’t confined to the commercial realm. They also affect our national security. Alliances, whether they be trade or otherwise, work based on accumulated good will. When we ask a country to host our submarines or NATO members to send troops somewhere, we draw upon the goodwill that we have accumulated over decades. Those governments have to sell the request to their own legislatures and voters who will sensibly ask: “What has America done for us lately?” And unfortunately, trade policy over the past 18 months has not engendered support.

A schedule of tariff rates can be repealed by proclamation. An accusation, once made and in the name of the United States government, is not so easily repealed. Those accusations carry weight because, traditionally, we have used them sparingly and when the evidence was abundantly clear. Now, if Lincicome is correct, our credibility on this stage has been strained.

These new tariffs may not survive on a legal basis. Courts struck down the emergency tariffs in February and the Section 122 tariffs in May. Somin expects this action to be challenged and believes that courts will strike these down, too. Whether or not the courts strike these down, too, the damage is already done.

The trust that America enjoys took generations to build and is being spent at a record pace. In the meantime, the world is moving on and increasingly without us. Unfortunately, courts cannot restore what was actually lost this week. Judges can void tariffs and force refunds, but they cannot unsay an accusation.

A free society should be judged less by who becomes wealthy than by how easily people can improve their circumstances under impartial rules. Who gets wealthy matters less than how.

Income inequality is dominating a national news landscape primed for questions of affordability, contrasted with ever-growing private fortunes on the other. Socialists in the New York Mayor’s treat wealth concentration as one of America’s defining political problems. Debate erupted over Elon Musk’s growing fortune, accompanied by familiar declarations that America should never permit its first trillionaire. A $30 million wedding and a sweeping “housing affordability law.”

As another national campaign season begins, including some unapologetically redistributionist platforms, Americans should expect to hear still more about “income inequality.” Candidates will promise to narrow it, activists will measure it, and commentators will treat it as a proxy for economic justice.

But income inequality, while politically useful, is a poor measure of economic health. By itself, it tells us surprisingly little about whether an economy is flourishing or failing. More often than not, it distracts from the question that actually matters.

The Real Metric is Mobility

A free society does not merely permit unequal outcomes; it guarantees them. That is not principally because people differ in intelligence, industriousness, or luck, though they do. More fundamentally, they differ in what they want.

Some willingly exchange higher salaries for flexibility, especially balancing with care tasks. Others endure longer hours, greater stress, or years of additional education in pursuit of higher earnings. Some choose to relocate or remain in expensive metropolitan areas because the labor market rewards them accordingly. Others leave those same cities for lower costs of living, accepting slower wage growth in return for larger homes, shorter commutes, or proximity to family. Increasingly, adherents of the FIRE and Coast FIRE movements deliberately sacrifice their personal lives and some luxuries in their peak earning years in exchange for earlier financial independence or greater autonomy over their time. Of course, these people experience vastly different financial outcomes, largely as a result of those choices.

These decisions are not distortions of the market. They are among its principal expressions. Income is only one of many goods people seek to maximize. Leisure, stability, family, geographic preference, vocation, autonomy, and prestige all compete with wages. Once individuals are free to order those priorities differently, unequal outcomes become the predictable consequence of liberty itself.

Why France’s Labor Market Is Increasingly Concentrated Near the Minimum Wage

For all these reasons, the elimination of income inequality is not, in itself, a desirable policy objective. Stopping some people from moving up does not reallocate resources to the poor. It destroys them or fails to create them at all.

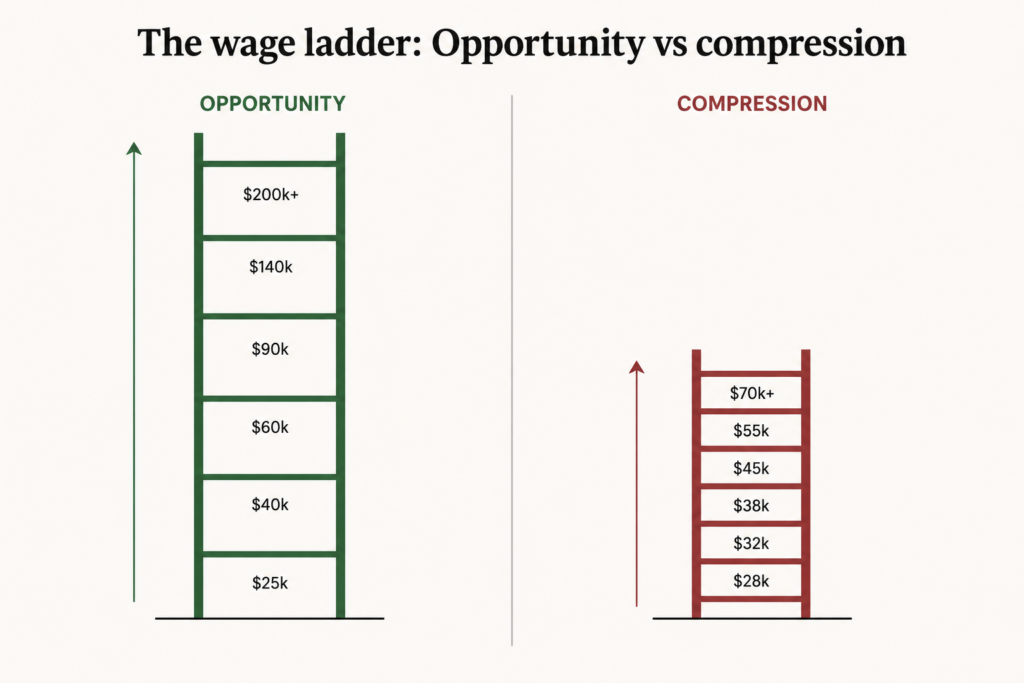

France offers a useful illustration. For years, economists have noted smicardisation — the concentration of wages at or near the statutory minimum. Wage compression has left fewer opportunities to advance beyond them. Promotions yield relatively modest gains, career progression slows, and fewer meaningful steps exist between the bottom and the top of the wage distribution.

The irony is difficult to miss. A society can reduce measured income inequality by reducing economic opportunity. Compressing wages may satisfy a political desire for “equity,” but it also flattens the incentive structure that encourages workers to acquire new skills, assume greater responsibility, or move into more productive occupations.

Markets are not valuable because they produce equal outcomes. They are valuable because they reward differences in productivity, specialization, innovation, and risk-taking. When those differences are compressed, the economy becomes less dynamic, not more just.

The relevant inquiry, then, is not whether incomes differ, but how freely people can move between economic strata.

Social mobility is a measure of opportunity rather than distribution. It asks whether individuals remain permanently confined to the economic circumstances into which they were born, or whether talent, effort, prudent decision-making, and changing life circumstances allow them to move upward — or downward — over time.

This distinction is frequently lost because public debate tends to treat income groups as though they were fixed populations. They are not.

Most People are Both Poor and Wealthy in Their Lifetimes

Individuals occupy different places in the income distribution at different stages of life. Earnings generally rise through middle age before declining in retirement. Total household wealth may spike when a house is sold or dip during a brief unemployment. Young workers who appear in the lowest quintiles often move substantially upward over their careers. Likewise, many who are born into affluent households fail to remain there as adults. The composition of each income quintile changes continuously, even if the statistical distribution appears relatively stable from year to year.

None of this is to suggest that mobility is perfect or that barriers to advancement do not exist. They plainly do. Housing costs, educational quality, occupational licensing, family instability, and regulatory barriers can all impede upward mobility and deserve serious attention. But those are questions about opportunity — not outcome.

Looking upward at those who have more, with blame, instead of inward asking how to achieve it, is a seductive impulse. Romans called it Invidia, envy, not simply an emotion but a destructive quasi-supernatural force capable of corroding both the individual and the Republic. Envy requires no self-examination, no acknowledgment of tradeoffs, no accounting for neglected opportunities or misjudgments. The belief that every disparity is evidence of injustice comforts the bruised psychology. Every success is an implicit accusation. To succeed becomes suspect.

A politics centered on mobility makes far greater demands. Asking how people rise obliges us to question institutions that either expand or restrict opportunity. It asks difficult questions of ourselves. Which ambitions did we pursue? Which sacrifices were we unwilling to make? Which opportunities, what profitable paths, did we decline in favor of other goods, or experiences, we valued more?

Joan Didion once observed that self-respect comes from accepting responsibility for oneself. That observation is no less applicable to economics than to character. A society committed to opportunity expects individuals to exercise agency within the freedoms they possess, even while recognizing that circumstances differ and misfortune is real.

Not everyone has the same combination of ability, appetite for risk, or singular ambition. We are not all born into homes with equal resources or offered the same educational and professional choices. But almost everyone possesses more agency than contemporary politics is willing to admit. The relevant question is seldom whether you could have become one of the wealthy elite. It is whether you might have become someone other than the person you are today.

Asking for personal accountability, for self-examination, is a far less politically convenient conversation than railing against “income inequality.” Campaigns built on redistribution require little more than resentment to move them along, but they only worsen the incentive problems they purport to solve. A society committed to expanding opportunity demands something more difficult: institutions that preserve mobility, not ‘equality,’ and citizens willing to bear responsibility for what they do — and fail to do — with their freedoms.

“Fascism entirely agrees with Mr. Maynard Keynes, despite the latter’s prominent position as a Liberal.”

So wrote the British fascist James Strachey Barnes in his 1928 book Universal Aspects of Fascism, which included a glowing preface written by Mussolini himself. “In fact,” Barnes continued, “Mr. Keynes’s excellent little book, The End of Laissez-Faire…might, so far as it goes, serve as a useful introduction to fascist economics.”