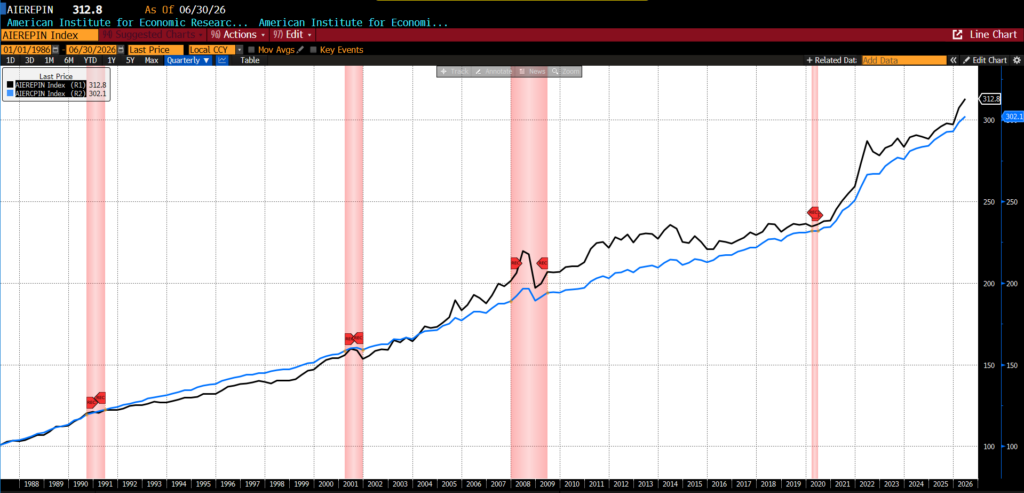

The AIER Everyday Price Index (EPI) fell to 312.8 in June 2026, down from 316.0 in May. The 1.02 percent monthly decline reversed part of May’s sharp energy-driven increase and brought the index down by roughly 3.2 points. Fifteen EPI categories rose, eight declined, and no indicator was unchanged, but the sizable drop in motor fuel more than offset price increases elsewhere.

The largest monthly decline came from motor fuel, which fell 9.6 percent in June. Other notable declines included movie and theater admissions, tobacco and smoking products, and purchase, subscription, and video rentals. The largest increases came from gardening and lawncare services, intracity transportation, personal care services, and fuels and utilities. Food away from home and food at home also rose, but not by enough to counteract the decline in gasoline-related costs.

AIER Everyday Price Index vs. US Consumer Price Index (NSA, 1987 = 100)

(Source: Bloomberg Finance, LP)

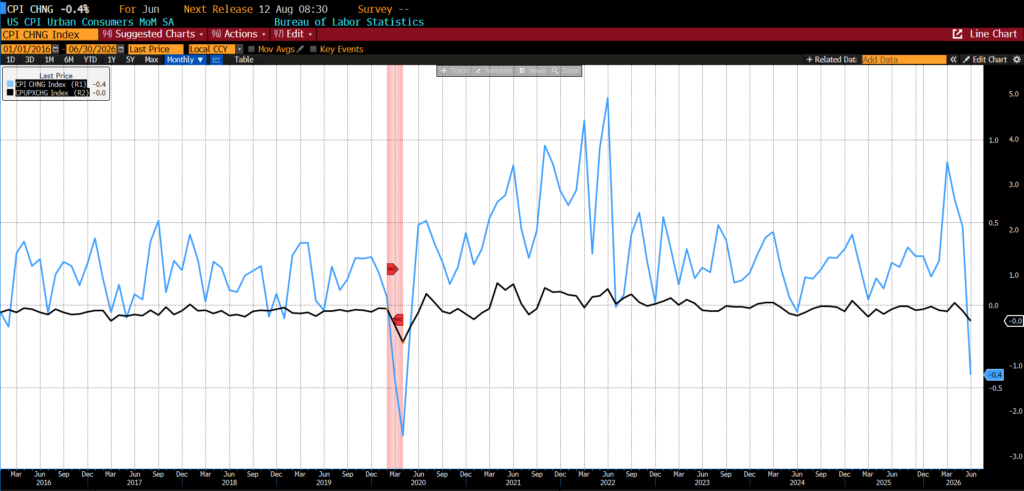

Also on July 14, 2026, the US Bureau of Labor Statistics (BLS) released the June 2026 Consumer Price Index (CPI) data. Headline CPI fell 0.4 percent on a seasonally adjusted basis in June after rising 0.5 percent in May; this was the largest one-month decline since April 2020. Core CPI, which excludes food and energy, was unchanged in the month after increasing 0.2 percent in May.

June 2026 US CPI headline and core month-over-month (2016 – present)

(Source: Bloomberg Finance, LP)

Consumer prices in June were driven overwhelmingly by a reversal in energy costs. The energy index fell 5.7 percent after rising 3.9 percent in May, 3.8 percent in April, and 10.9 percent in March. Gasoline prices declined 9.7 percent on the month, both seasonally adjusted and before seasonal adjustment, making energy the largest contributor to the decline in the all-items CPI. Electricity fell 1.0 percent, while utility gas service rose 0.5 percent.

Food prices continued to rise, though moderately. The food index increased 0.2 percent in June, as did food at home and food away from home. Within groceries, meats, poultry, fish, and eggs rose 0.6 percent, with eggs up 4.3 percent. Dairy and related products increased 1.2 percent, cereals and bakery products rose 0.3 percent, and other food at home increased 0.5 percent. Offsetting those gains, nonalcoholic beverages fell 1.5 percent, helped by a 2.0 percent decline in coffee prices, while fruits and vegetables slipped 0.2 percent.

Core inflation softened notably. The index for all items less food and energy was unchanged in June, with several categories declining outright. Motor vehicle insurance fell 2.0 percent, communications declined 1.5 percent, apparel fell 0.6 percent, medical care slipped 0.1 percent, and used cars and trucks declined 0.2 percent. Shelter rose only 0.1 percent, its smallest monthly increase since January 2021. Rent of primary residence rose 0.1 percent, owners’ equivalent rent increased 0.2 percent, and lodging away from home fell 2.3 percent.

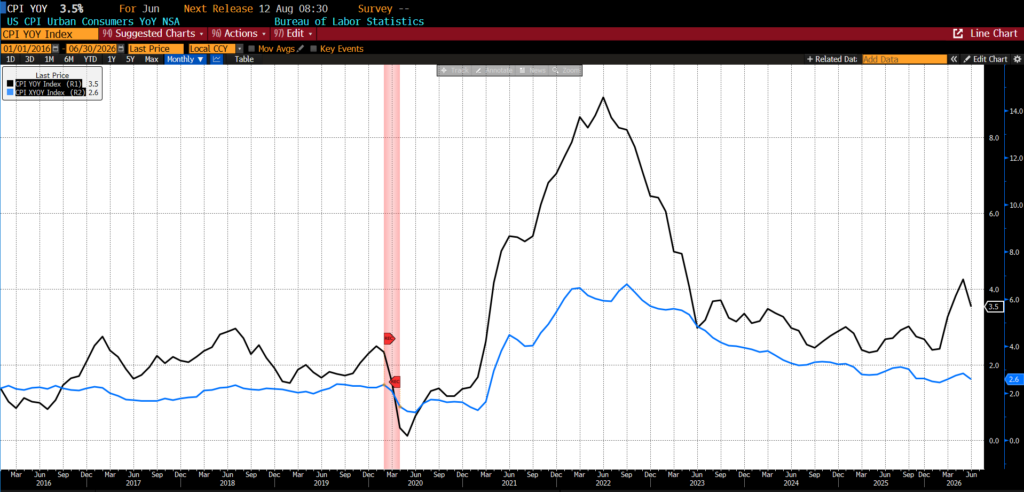

Over the twelve months ending in June 2026, headline CPI rose 3.5 percent, down from 4.2 percent in May. Core CPI increased 2.6 percent over the year, following a 2.9 percent annual increase in May.

June 2026 US CPI headline and core year-over-year (2016 – present)

(Source: Bloomberg Finance, LP)

From June 2025 to June 2026, food inflation remained moderate but persistent. Food at home rose 2.7 percent over the year, while food away from home increased 3.4 percent. Fruits and vegetables rose 5.3 percent, other food at home increased 2.4 percent, meats, poultry, fish, and eggs rose 2.6 percent, nonalcoholic beverages advanced 2.9 percent, and cereals and bakery products increased 2.4 percent. Dairy prices were nearly flat, rising only 0.4 percent over the year.

Energy remained the dominant annual inflation story despite June’s monthly pullback. The energy index increased 15.7 percent over the twelve months ending in June, with gasoline prices still up 26.7 percent from a year earlier. Electricity rose 4.0 percent and utility gas service increased 3.0 percent over the same period. Thus, while June brought meaningful short-term relief at the pump, energy costs remained substantially higher than a year earlier.

Core inflation was less dramatic but still broad enough to matter. Prices excluding food and energy rose 2.6 percent over the year. Shelter increased 3.3 percent, continuing to anchor underlying inflation, while medical care rose 2.0 percent, recreation increased 2.8 percent, and household furnishings and operations advanced 2.5 percent. Airline fares remained one of the most striking annual increases, rising 26.5 percent from June 2025, even as they eased modestly on the month.

The June CPI report provided the clearest evidence yet that the spring 2026 energy shock is beginning to reverse. After gasoline and other fuel costs drove inflation sharply higher in March through May, June brought falling gasoline prices, a lower headline CPI reading, and a decline in AIER’s EPI. For consumers, this was particularly significant because gasoline is among the most visible and psychologically influential prices they face. Even so, affordability remains strained as shelter, dining out, and many service-sector prices continue to rise, leaving June looking more like a pause in an energy-driven inflation surge than the end of the inflation problem.

The report also reshaped the Federal Reserve’s near-term outlook. Chair Kevin Warsh has emphasized that restoring price stability remains the Fed’s overriding priority, but the softer June inflation data reduce the urgency for another rate hike while allowing policymakers to maintain a hawkish tone. Markets responded by substantially lowering the probability of a near-term increase in interest rates, suggesting the Fed can afford to wait for additional evidence from future inflation reports, labor-market conditions, and energy prices before deciding whether further tightening is warranted.

That patience, however, comes with risks. June’s improvement depended heavily on lower gasoline prices, leaving inflation vulnerable to renewed geopolitical disruptions, higher oil prices, tariffs, or continued AI-related investment pressures that could reignite cost increases. While the Fed cannot produce more oil or resolve supply shocks, it must remain alert to the possibility that temporary increases in energy costs become embedded in inflation expectations, wage demands, and business pricing decisions. The result is a delicate balancing act: avoiding an unnecessary policy response to what may prove to be a temporary supply shock while ensuring that inflation does not become entrenched once again.

The overall rate of inflation declined sharply in June, the Bureau of Labor Statistics reported this week. The Consumer Price Index fell 0.4 percent last month, a sharp reversal from the 0.5 percent increase in May. On a year-over-year basis, headline inflation eased to 3.5 percent from 4.2 percent, reversing three straight monthly increases in the annual rate and pulling it back from its highest reading in more than a year.

Core inflation cooled as well. Excluding volatile food and energy prices, CPI was flat in June, down from a 0.2 percent increase in May. On a year-over-year basis, core inflation eased to 2.6 percent from 2.9 percent.

As in recent months, much of the headline story came down to energy, but this time in reverse. The energy index fell 5.7 percent in June, its largest monthly decline since April 2020, and was, according to the BLS, “the largest contributor to the monthly all items decrease, more than offsetting increases in other indexes including those for shelter and food.” Gasoline prices fell 9.7 percent over the month, though they remain up 26.7 percent over the past year. The broader energy index is still up 15.7 percent, a reminder of how far energy prices had climbed during the oil shock tied to the conflict involving Iran and the disruption to shipping through the Strait of Hormuz.

But the cooling was not confined to energy. Services excluding energy were flat in June, core goods prices fell 0.1 percent, and shelter rose just 0.1 percent, its smallest monthly increase since January 2021. That breadth distinguishes the June report from earlier months, when softer core readings often coexisted with persistent pressure in major service categories.

The recent trend confirms the price moderation. Over the three months through June, headline CPI rose at a 2.8 percent annualized rate, well below its 3.5 percent year-over-year pace. Core CPI rose at a 2.4 percent annualized rate over the same period, also below its 2.6 percent year-over-year rate. For the first time in months, recent momentum in both headline and core inflation is running cooler than the annual figures, not hotter.

Although the Federal Reserve officially targets the personal consumption expenditures price index, CPI data remain a timely and relevant gauge for policymakers. The June report clearly moved expectations. At the time of writing, the CME Group’s FedWatch tool put the probability that the Fed would raise rates at its meeting later this month at roughly 16 percent, down from 42 percent before the release. A hold is now the clear baseline expectation, pushing the debate over further tightening into the fall.

The labor market has lost some momentum as well. Employers added just 57,000 jobs in June, and the BLS revised April and May payrolls down by a combined 74,000. The unemployment rate fell slightly to 4.2 percent, average hourly earnings rose 0.3 percent on the month and 3.5 percent over the past year, and labor-force participation slipped to 61.5 percent.

With workforce growth held down by an aging population and reduced immigration, even soft payroll gains need not signal a weakening economy. Indeed, June’s increase was roughly in line with the average over the prior year. But the combination of slower hiring and cooler prices marks a clear change from where things stood just a few months ago.

The case for tightening rested on inflation that was drifting higher and on the risk that the energy shock would spread to broader prices. That case has weakened. The June data offer the first meaningful sign that price pressures are abating rather than broadening.

Still, one month does not make a trend, and the deeper question is whether demand is moderating. A one-time oil shock changes relative prices. By itself, it cannot sustain inflation year after year; that requires nominal spending to continue outpacing the economy’s capacity to produce. The advance estimate of second-quarter GDP, due at the end of the month, will provide the first comprehensive reading on whether nominal spending has begun to slow. If it has, June’s report will look like the start of genuine disinflation. If it does not, the month may prove an energy-driven reprieve rather than a turning point.

For now, the Fed has little reason to change rates in July. The case for an increase, which markets took seriously only weeks ago, has faded. But inflation remains above target, and the labor market, though softer, is not weak enough to demand a cut.

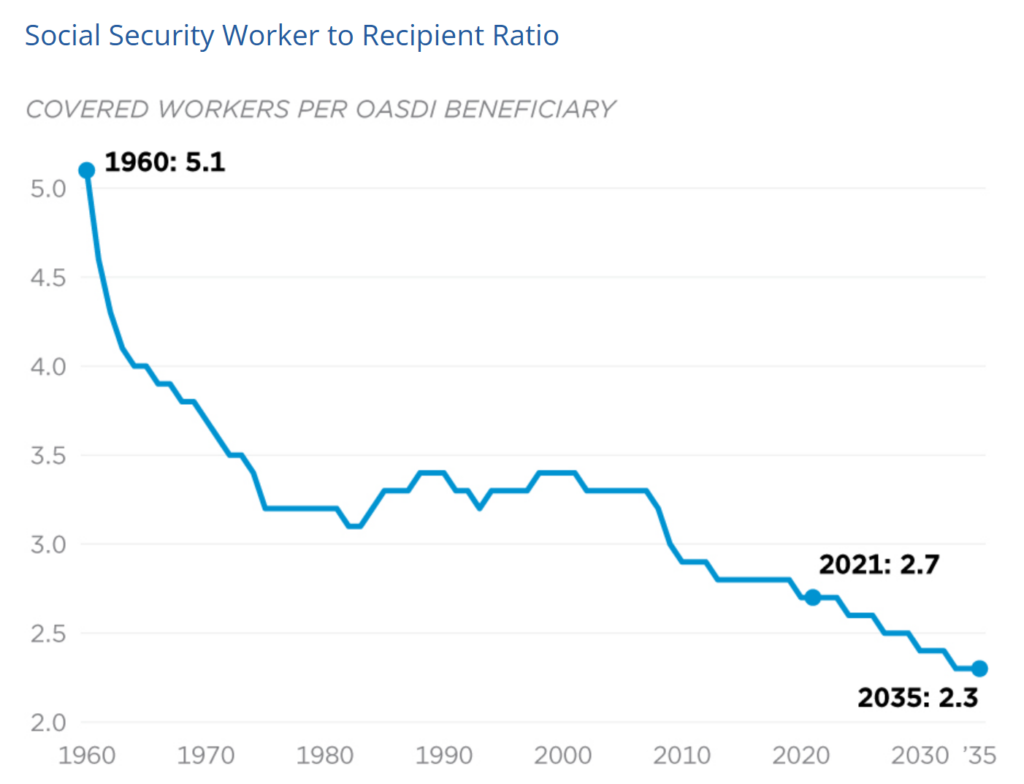

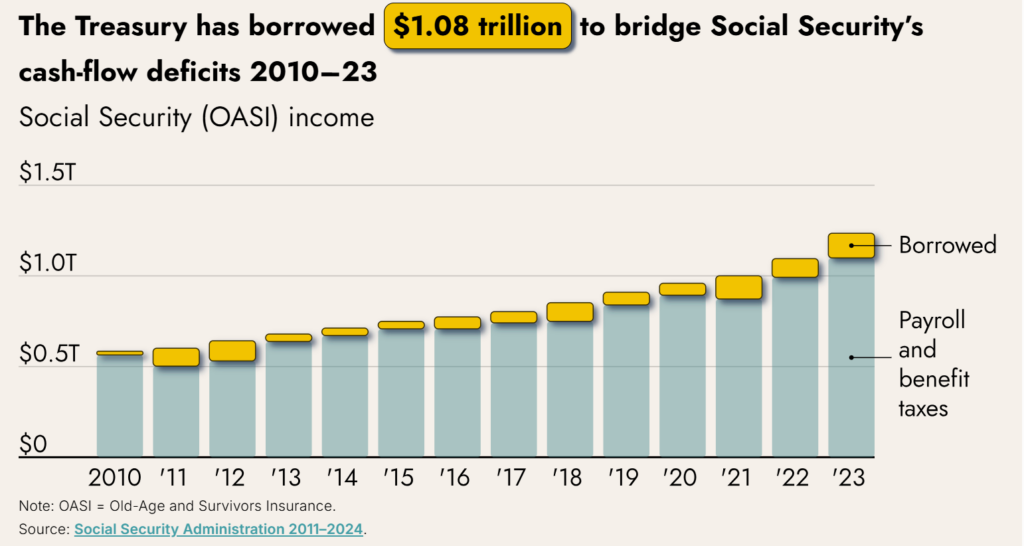

As Social Security reaches its ninety-first anniversary this August, it’s running out of room for evasion. The 2026 Trustees Report projects Old-Age and Survivors Insurance (OASI) trust fund will be depleted by the fourth quarter of 2032, after which dedicated revenue would only cover 78 percent of scheduled benefits. On a combined basis with Disability Insurance, reserves would run out in late 2034, with 83 percent payable then and 65 percent by 2100.

The current schedule and financing cannot survive under existing law. That is the setting for Romina Boccia and Ivane Nachkebia’s Reimagining Social Security. Nearly a year after its release, the book is more relevant than ever.

The authors argue that Social Security should return to the program’s original purpose: old-age poverty protection. As President Roosevelt warned, “We can never insure one hundred percent of the population against one hundred percent of the hazards and vicissitudes of life.” Yet the program has become both a redistribution and a public pension promise for nearly everyone, making it politically untouchable.

The book draws lessons from Canada, Germany, New Zealand, and Sweden. Its reform menu includes a higher retirement age, a flatter benefit, automatic balancing mechanisms, and expanded private saving. Cato’s reform hub frames the problem clearly: promises exceed dedicated financing, and delay makes the eventual adjustment larger.

The book’s strongest point is that solvency and purpose are separate questions. Congress could close the gap through higher payroll taxes, benefit cuts, borrowing, heavier taxation of benefits, a higher retirement age, or some combination. None of those prescriptions answers what Social Security is for. If the goal is old-age poverty prevention, a flat benefit makes sense. If the goal is an earnings-related federal pension, higher taxes become harder to avoid.

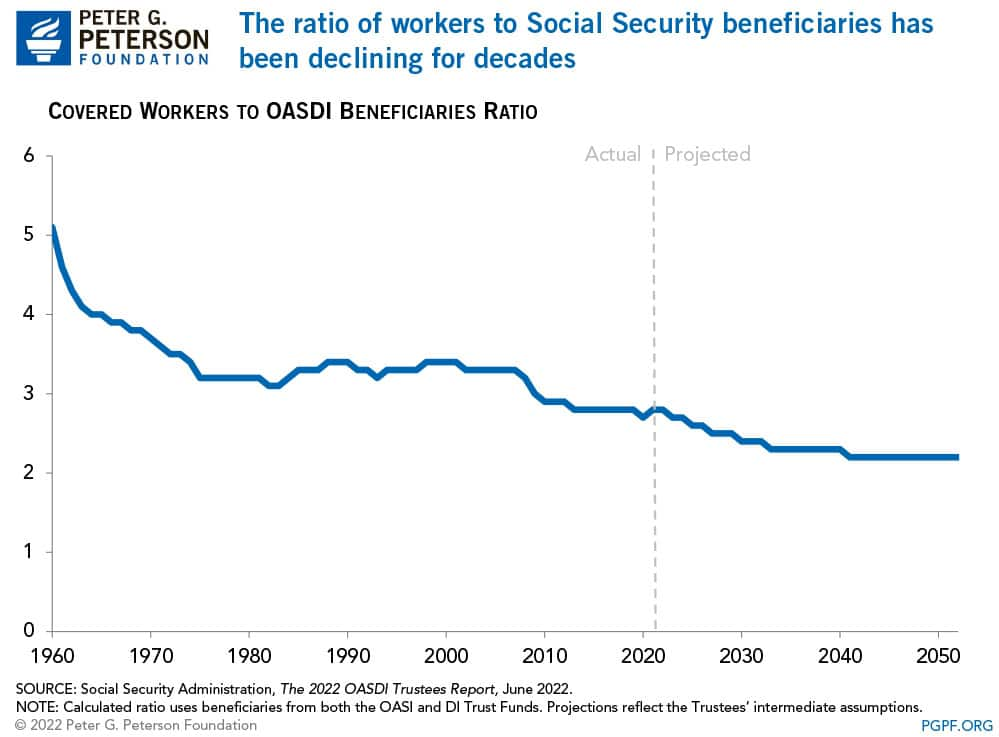

Recent work sharpens the case. Boccia and Krit Chanwong argue that the low fertility assumptions used by the Trustees report raise the long-term shortfall from roughly $33 trillion to $35 trillion or $36 trillion. The warning is clear: pay-as-you-go systems are hostage to demography.

Social Security Data. Image from The Federal Budget in Pictures

The trust-fund question receives similar care both in the book and on Cato’s visual feature on Social Security’s financial crisis, which rightly rejects the idea that the trust fund is a pile of saved payroll-tax contributions. Social Security is mostly pay-as-you-go. When costs exceed non-interest income, redeeming trust-fund securities requires Treasury financing. The bonds are legal obligations; the issue is who pays.

From Cato’s visual feature Social Security’s Financial Crisis

A flat benefit would bring Old-Age Insurance back to its original promise of “some measure of protection” against end-of-life poverty while making redistribution more explicit. Low earners would be protected. Middle- and high-income workers would rely more on private saving and receive less than scheduled benefits.

A higher retirement age has similar appeal and danger. Longer lifespans support later eligibility in the aggregate, but averages conceal workers with shorter life expectancy, manual jobs, disability risk, or weak late-career attachment. This is the greatest challenge for reformers.

Without a sustainable transition, political backlash can unravel any reform. The 2007 AIER Bulletin “What You Need to Know About Social Security” warned that current retirees and near-retirees have planned around specific benefits. Reducing them, especially for middle and high earners, will feel like a rug pull deserving of political punishment. Reformers should, therefore, keep cohort politics at the center of any proposal.

I hope the next phase of this project tackles cohort differentiation. Simply put, this involves separating citizens by age group and applying different changes to each cohort. Retirees and near-retirees could remain in the current system, while COLA adjustments, transitions to flat benefits, and switches to private savings accounts phased in for succeeding generations. Here I am a bit more hopeful than Boccia that Trump Accounts and Trump IRAs can help create the universal savings account off-ramps to Social Security’s crisis.

The book’s savings account proposal is attractive for younger workers, myself included, because it promises ownership, portability, and flexibility. Yet voluntary accounts may suffer from low take-up, while automatic enrollment moves toward compulsion. That tension is unavoidable. Retirement policy operates amid inertia, liquidity constraints, and imperfect foresight.

Reimagining Social Security asks whether Social Security should remain an expansive public pension promise or become a clear floor against old-age poverty. The latest Trustees Report makes that question urgent. Boccia and Nachkebia’s answer is a smaller, more candid system: protect seniors at the bottom, honor reliance interests among current retirees, and stop pretending payroll taxes can finance promises demographic change has already undermined.

As Social Security rapidly approaches the fiscal cliff, Reimagining serves as an important starting point for a national conversation about the program’s future — one that can no longer be deferred.

How can one sign a contract before birth? That question can’t be answered by President Bill Clinton, who said “we mustn’t break the solemn compact between generations,” in a 1998 address on Social Security.

Such a speech constructs Social Security as a contractual mandate in need of protection rather than an insurance and redistribution program. Grand national “contracts” should face significant scrutiny, as they borrow the moral force of a contract without the requirements that define one.

No national contract language appeared in the Social Security Act when Franklin D. Roosevelt signed it in 1935. The argument was about insurance, protection against unemployment, and poverty among the elderly. The original New Deal case for Social Security was that the federal government had a responsibility to create a system of economic security against the hazards of modern life. Contrast that with the contract framing of Social Security. Social Security becomes a question of sacred duty and obligation, not policy. Altering the program, a necessity given the debt, would seem to be a generational betrayal.

But for contracts to be legally enforceable, at a minimum, both parties must be capable of consent.

Legally, the four requirements of a contract are offer, consideration, acceptance, and an intention to create legal relations. A person not yet born cannot be offered a contract, consider it in any manner or ask for compensation, accept it in any way, or intend legal relations. By any measure, Social Security cannot be a legal contract.

True, some contracts allow you to consent in ways other than signature. John Locke’s ideas of Social Contract Theory hold that paying taxes and participating in the democratic process constitute a valid contract with the government. Even this type of contract, however, needs clear parties and justification for the consent. Social Security cannot meet this most basic criterion, as the Social Security contract relies on the participant before they are alive. To highlight this absurdity: I was born in 2005, and Social Security relied on my payments to beneficiaries long before I existed. I supposedly entered a contract decades before I, in any meaningful sense, existed. This is not a minor technicality but a central contradiction. A contract is, at root, an agreement between two parties; Social Security is neither an agreement nor between two parties.

The defender of Social Security may object that this is too literal. “Generational contract” is a mere metaphor. Such a notion creates a dilemma: if the phrase is only metaphorical, Social Security cannot carry the moral duty of an actual contract. Following that claim, younger workers are not morally bound by the choices of prior political actors. But Clinton clearly intended us to be so bound. If the phrase is meant to carry moral force and contractual obligations, then we are entitled to ask the basic questions: Who agreed? When did they agree? What were the terms? And how could people who were not consulted be said to have consented?

The metaphor survives by morphing into a form that is most convenient. When challenged, it is a metaphor. When used politically, it is an obligation — specifically (at least) 30 trillion in unfunded obligations over the next 75 years.

Once demographic realities are taken into account, relying on future generations of unborn contributors becomes less a matter of social contract than one of program solvency. Social Security is largely financed on a pay-as-you-go basis. Taxes from current workers fund benefits for current retirees. This system can only work if the number of workers is sufficient to pay for the number of retirees. That is not a timeless contract but gambling the future on unknown, and unknowable, demographic trends.

If fertility falls, immigration slows, the worker-to-beneficiary ratio declines, wage growth disappoints, or longevity increases faster than expected, the supposed contract becomes harder to honor. Retirees are told after a lifetime of payroll taxes that they will have secure funding, but the actual financing of that compact depends on workers yet unborn — workers who may never exist in sufficient numbers.

If the number of workers is insufficient, few remedies are available, and each has significant drawbacks. In short, options are limited to cutting benefits, raising taxes, or taking on still more national debt. All violate some of the system’s promises. Contracts don’t work under these conditions. A contract does not normally depend on a party that never consented, may not exist in sufficient numbers, and can have its obligations rewritten by future legislation. Yet this is exactly the structure of Social Security’s “generational bargain.”

To be clear, this is not a critique of Social Security for failing to predict the future perfectly. No government program can foresee every war, recession, pandemic, fertility decline, or demographic shift. The fault is not that Social Security lacks omniscience. The fault is that the pay-as-you-go system needs omniscience to function. Every time history turns, benefits and taxes need to be rewritten. Policymakers need to know the demographics of the far-off future to ensure the budget remains balanced. While year-to-year Social Security can survive without knowing the future, it is impossible in the long term to avoid repeated tax increases, benefit reductions, or new borrowing. All allow policymakers to retroactively alter the deal, while conscripted participants can only pray it isn’t altered further.

Social Security’s defenders should say what they mean and mean what they say. If the program is redistributive, defend the program as redistribution. If it is an anti-poverty policy, defend it as such. If it is forced retirement saving, defend forced saving. If it is social insurance, defend social insurance. Each of those claims may have merit, but it is in no shape or form a contract.

It is a great disservice to the American people that a program as massive as Social Security, a program that takes 6.2 percent (often twice as much) of every paycheck, is so poorly argued for, and its rationale is murky and drifting.

Justice requires that a program of this magnitude have clearly articulated goals and functions. Unfortunately, Social Security does not. A contract requires intent and consent. Unfortunately, Social Security mocks them. Even taxation requires the consent of the governed, and representation of the taxed, to distinguish itself from tyranny, extortion, and abuse. Unfortunately, Social Security defies that standard.

In director Richard Linklater’s early ’90s classic Dazed and Confused, high school teacher Ms. Stroud (Kim Krizan) tells her class, right before dismissing them into the summer of 1976, that they should be skeptical of the incoming bicentennial hoopla they’re likely to encounter. She tells them that what everyone around them will really be celebrating is “the fact that a bunch of slave-owning, aristocratic, white males didn’t want to pay their taxes.”

That particular phrasing may be fictional, but it is not hard to imagine a young high school teacher, fresh out of college in the era of radical politics, delivering such a verdict to her teenage charges in the mid-1970s. And such lessons have only become more common over time. The left-wing contempt for our founding values has, by this point, acquired a long pedigree of its own, from Howard Zinn’s A People’s History of the United States (1980) to James Loewen’s Lies My Teacher Told Me (1995) and beyond.

It is often said that any work of history reveals as much about the time in which it is written as it does the period on which it is ostensibly focused. While that is true of historical works in general, it seems virtually guaranteed to be true of a new book whose topic is the semiquincentennial of the signing of the Declaration of Independence.

After 250 years of conflict and compromise, the Declaration is still considered essential US political theory and the starting point for arguments about which sort of country we have, and which sort we should have. Richard Reinsch’s new edited collection of essays — The Civitas Collection 250 — certainly fits into that tradition.

A student of US history approaching debates over the American Founding for the first time might not see this immediately. Many of the essayists spend most of their time in the eighteenth century, or before. The writings of Thomas Jefferson, John Adams, and John Dickinson get plenty of attention, as do familiar names like John Locke, Thomas Hobbes, and Montesquieu, and famous precedent documents like the Declaration of Right (1689), Petition of Right (1628), and Magna Carta (1215). But first impressions can be deceiving.

Is Kody Cooper’s essay on the sources of liberty in the Declaration of Independence, for example, just about the development of law and philosophy prior to the American founding? He certainly covers writers ranging from Cicero and Tacitus to Richard Hooker and Locke, but he also moves forward in time to contrast the founding principles of the Declaration to much later interpreters. Arguing for a universalist view of the rights proclaimed in 1776, Cooper writes “Contrary to exclusive interpretations advanced by later jurists like Justice Roger Taney and his successors among the critical race theorists, the word ‘men’ did not mean merely white men.”

In the blink of an eye, the discussion zoomed past the ancient philosophers and early modern legalists to The 1619 Project and Ibram X. Kendi. The contributors to The Civitas Collection are all serious scholars with much to say about the founding era, but it is also clear they have contemporary battles to wage with their interpretation of what our founding documents really say. With the Declaration functioning, in the famous words of the late historian Pauline Maier as “American scripture,” it seems inevitable that most combatants in US politics will want to claim the document’s mantle for their own preferred ideological strain.

Some of these conflicts are longstanding and easily recognizable ones, between political theorists of the right and the left. Cynicism about the motives and beliefs of the founding generation, for example, is not new.

Anti-hagiographies of the Revolutionary generation are so common they’ve inspired their own subgenre of anti-anti-founding fathers publishing, including books like Thomas West’s Vindicating the Founders (1997), Larry Schweikart and Michael Allen’s A Patriot’s History of the United States (2004), and Brion McClanahan’s The Politically Incorrect Guide to the Founding Fathers (2009).

Those left-versus-right debates continue to be timely and there’s plenty of scholarship in the present volume to illuminate them further. But perhaps more interesting are the fights, more often flying under the radar, that are happening within the center-right segment of the political spectrum. Not between conservatives and Marxists, but between nationalists, libertarians, classical liberals, new whigs, and whatever else the non-leftists of America are calling themselves these days.

Adam Lebowitz, for example, laments early in his essay that a “broadly libertarian reading [of the Declaration] has hardened into something like conventional wisdom.” Rather than being fearful of executive authority and a strong government because of the negative example of King George III, Lebowitz argues that our founders thought of the Declaration as “a warrant for a stronger, more energetic government, grounded in democratic sovereignty and endowed with plenary powers.”

The argument that the spirit of the Declaration was consistent with a strong executive and a federal government of essentially unbounded authority obviously has implications for how the powers of the presidency are practiced and circumscribed in the age of Donald Trump. High-profile debates over immigration and deportation, National Guard deployments, and the bombing of Iran are directly relevant to whether our nation’s founders are perceived to have been wary and concerned about dictatorial executive power or in favor of its wide exercise.

Even more pointed is the contribution of former deputy attorney general John Yoo, who writes, “We should not mistake…the colonists’ frontal attack on tyranny for a rejection of the idea of executive power,” stating plainly that “the Declaration of Independence itself is not a rejection of executive power.” Yoo documents the history of the Articles of Confederation and the rapidly evolving state constitutions of the 1780s, which initially favored a very weak (often plural) executive, but were quickly reformed to establish offices of more effective leadership. Yoo’s previous scholarship and policy advocacy for a maximalist view of the president’s war powers during the George W. Bush administration are clearly relevant here.

Beyond the specific powers of the federal government — the kind that can be parsed in a decision of the Supreme Court, for example — contributors also take on the wider cultural understanding of the Declaration. Wilfred McClay, for example, considers the contemporary divide “between creed and culture.” He asks whether being an American is defined more by embracing the universal propositions of the Declaration’s famous second paragraph (about all men being created equal) or whether our Americanness has as much, or more, to do with the unique heritage of our geographical homeland.

This question could, of course, not be more timely. One of the hottest debates in the second Trump administration has been over the birthright citizenship doctrine of the Fourteenth Amendment, and whether it is just and reasonable to gatekeep US citizenship based on racial, religious, ethnic, or other criteria. Are we all equal as Americans because of the doctrine of the Declaration, or are some Americans with longer North American lineages, so-called “Heritage Americans,” entitled to more deference and privileges? And if not formal legal privileges, some ask, are they at least able to credibly claim to be “more American” than someone who took the oath of citizenship yesterday?

Contributors to The Civitas Collection 250 also take on that other great cause of the day: tariffs and trade. Samuel Gregg, in particular, lays out how the American Revolution was an anti-mercantilist one, with much of the fervor of the patriot cause generated by infringements on the colonists’ commercial relationships, not just the rights and relationships that are usually considered to have the most sublime claim to moral seriousness.

Many popular revolts against alleged tyranny, both before and after 1776, centered on things like religious conscience and freedom of expression. Certainly, many of the violent and bloody conflicts in the West between the time of the Protestant Reformation and the Treaty of Westphalia involved both. Colonists of British North America were relatively short on complaints about burning churches, executions for heresy, smashed printing presses, and tarred-and-feathered pamphleteers. They did, however, complain most vociferously about the King “cutting off our Trade with all parts of the world” and being subjected to the British East India Company’s crown-granted monopoly on tea and other commodities.

As with the other questions about contemporary public policy, the attitude of the founders toward the freedom to trade is directly relevant to what the president and Congress are doing today. The late eighteenth century was a significantly less globally integrated place, with much of British North America consisting of smallholding farmers who rarely traded with anyone more than a day’s journey from home. If the freedom to buy and sell goods internationally was important enough to help spark the American Revolution back then, how much more important should we consider it to be in the twenty-first century of the Internet, containerized shipping, and FedEx?

American history nerds will love poring over the detailed references in the book and noticing references to events and documents that are often forgotten today, like the Continental Congress’ Olive Branch Petition (1775) or the infamous Cornerstone Speech (1861) by Confederate Vice President Alexander Stephens.

Armchair political theorists will likewise thrill to the supporting roles played by a long list of distinguished thinkers, both prominent and obscure. The academic tone may be a little intimidating for regular Americans just hoping for some Independence Day fireworks, but amateur historians and bookish patriots everywhere will no doubt love the collection Reinsch has assembled.

Heatwaves have pushed temperatures to record highs across both Europe and the United States. Yet the human toll between these two locales was dramatically different, with Europe recording more than 10,000 excess deaths in June.

This is a familiar pattern, notes Jack Nicastro:

The United Nations estimates that the European continent accounted for approximately 175,000 heat-related deaths annually between 2000 and 2019. The Environmental Protection Agency, meanwhile, calculates that about 1,300 deaths per year in the US are due to extreme heat. (This translates to four heat-related deaths per million annually in the US and 235 heat-related deaths per million annually across Europe.)

Europe and the US differ in demographics, urban density, reporting methods, and climate patterns. Even so, the death rate due to heat in Europe is 59 times higher than in the US.

In the United Kingdom, only about five percent of homes have air conditioning. In the United States, roughly 93 percent do.

Research identifies 72°F and 45 percent humidity as optimal for maximizing office and mental productivity.

With sweltering temperatures once again gripping much of the world, it is worth appreciating air conditioning — the quiet invention that transforms dangerous heat into manageable discomfort, shields millions from heat-related suffering and death, boosts productivity, and makes once-hostile climates livable. It is a powerful reminder that wealth, innovation, and human ingenuity enable societies to adapt to nature’s extremes and protect human life.

To understand why the US heat death rate is 59 times lower than that of Europe, it helps to begin with a young engineer named Willis Carrier.

The Father of Air Conditioning

Willis H. Carrier was born outside of Buffalo, New York on November 26, 1876, the same day inventor Alexander Graham Bell successfully demonstrated his large box telephone between Boston and Salem, Massachusetts. Carrier was an only child and attended a one-room schoolhouse. When he was nine years old he struggled to grasp the concept of fractions. His mother helped him master the idea using a pot of apples and slicing them into portions. Carrier remembered this event fondly as “the most important thing that ever happened to me.”

Carrier was awarded a full scholarship to attend Cornell University. He majored in engineering, earning a Master’s degree in 1901. After graduation, Carrier accepted a job at the Buffalo Forge Company for $10 a week.

The Sackett & Wilhelms printing plant in Brooklyn, New York was losing money because the sweltering, humid summers caused sheets of paper to absorb moisture from the air. The paper would expand and warp, throwing off the alignment of colored inks on the printed page and ruining entire print runs. They asked the Buffalo Forge Company for help. Carrier was assigned to solve the problem.

He was not trying to cool people. He was trying to save knowledge.

Air conditioning began not as a luxury, but as a technology of information, productivity, and adaptation — a machine that transformed oppressive heat from an economic barrier into a manageable inconvenience.

Carrier’s breakthrough system, in July of 1902, controlled both temperature and humidity, stabilizing the paper and rescuing the precision of mass communication.

Carrier applied for a patent on his invention, an “Apparatus for Treating Air,” which became patent No. 808897 and was issued on January 2, 1906.

On December 3, 1911, Carrier presented what is perhaps the most significant document ever prepared on air conditioning – Rational Psychrometric Formulae – at the annual meeting of the American Society of Mechanical Engineers. It became known as the Magna Carta of Psychrometrics and tied together the concepts of relative humidity, absolute humidity, and dew-point temperature, thus making it possible to design air-conditioning systems to precisely fit the requirements at hand.

In 1915 Carrier and six other engineers formed the Carrier Engineering Corporation using their personal savings of $32,600. Carrier Global Corporation (NYSE: CARR), the parent company of the Carrier HVAC and refrigeration business, has a current market capitalization of approximately $56 billion. This valuation makes it one of the largest climate and energy solutions providers in the world.

“With his new company,” Alexander Hammond notes, Carrier began to expand the use of air conditioning units by supplying hotels, department stores, movie theaters and private homes. His units were even installed in the White House, the US Congress and Madison Square Garden.”

Another overlooked legacy of Carrier’s invention is the birth of the summer blockbuster. Before air conditioning, movie theaters dreaded the hot months — few people wanted to sit in a crowded, sweltering auditorium. That changed in 1925 when the Rivoli Theatre in Times Square installed one of Carrier’s new cooling systems. Crowds flocked in, many as eager for the cool air as for the feature presentation. Almost overnight, summer transformed from Hollywood’s off-season into its most profitable season. Air conditioning didn’t just cool theaters — it reshaped the economics of entertainment and helped create one of America’s most enduring cultural traditions.

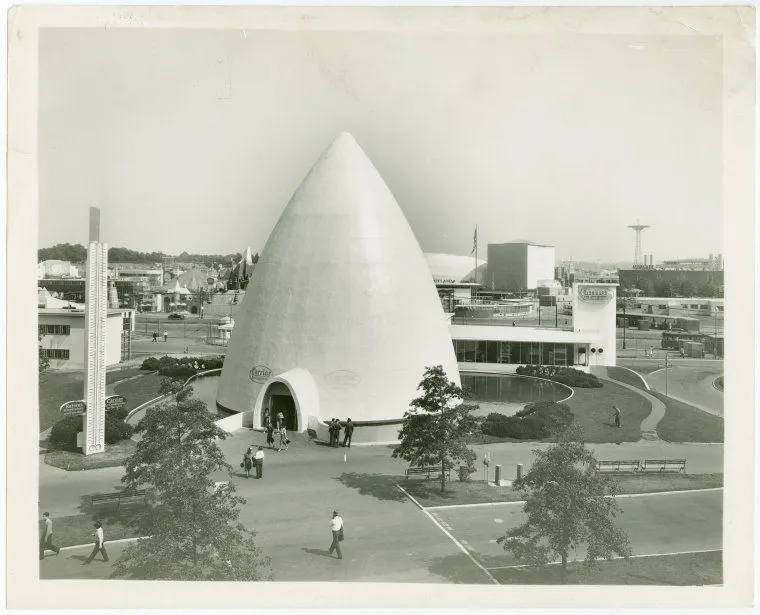

When New York City organizers launched the 1939 World’s Fair under the motto “Building the World of Tomorrow,” they sought technologies that would advance human progress and improve everyday life. Few embodied that vision better than modern air conditioning. During the Fair’s first 100 days, nearly 1.3 million visitors toured the striking “Carrier Igloo of Tomorrow.”

Carrier Corp’s Igloo, image from New York Public Library Digital Collections.

Inside, guests learned how air conditioning worked, explored a modern refrigerated food store, and experienced Carrier’s latest self-contained cooling systems — getting a glimpse of a future that would soon make homes, offices, and entire cities more comfortable, productive, and livable.

In 1985, Willis H. Carrier was inducted into the National Inventors Hall of Fame, and in 1998, Time magazine recognized him as one of the 100 most influential people of the 20th century.

By conquering heat and humidity with knowledge, Carrier enlarged the realm of human possibility. His invention transformed sweltering regions into thriving economies, extended human productivity, and brought comfort and prosperity to billions around the world.

One of the great triumphs of entrepreneurial capitalism is how quickly air conditioning traveled the familiar path from luxury to necessity. What began as an expensive convenience for a tiny elite became, within a generation, affordable to ordinary families. The market did not merely invent comfort — it democratized it.

In their report Time Well Spent: The Declining Real Cost of Living in America, Michael Cox and Richard Alm found that a 5,500-BTU air-conditioning unit cost about $350 in 1952. At the time, entry-level workers earned roughly 83 cents an hour, putting the time price at 422 hours.

Today, Walmart sells a far more efficient 6,000 BTU air-conditioning unit (with a remote control) for only $115. The current hourly wage for limited-service restaurant workers is around $19 an hour, putting the time price at six hours.

The time price has decreased by 98.6 percent. For the time it took US workers to earn the money to buy one unit in 1952, they get 70 today.

If air conditioning saves lives, why don’t more Europeans have it?

Europe’s electricity prices are typically much higher than the US, driven by higher taxes, network costs, renewable energy mandates, and energy import dependence. Customers in the US pay 17 to 19 cents per kilowatt-hour (kWh) compared to 25 to 32 cents in Europe. This means Europeans pay roughly 47 to 68 percent more per kWh than US customers.

Americans are also much richer than Europeans. According to World Bank data, American gross domestic product (GDP) per capita was $84,809 in 2024, while the European Union’s was 25 percent lower at $63,585. That $21,224 difference could buy a lot of comfortable cooling.

The European Union also prioritizes environmental targets over human comfort by imposing strict regulations for heating and cooling, making these amenities much more costly. The commission encourages citizens to use fans instead of air conditioning. Imagine the government doing that in Phoenix and Atlanta in July. Italy, Greece, and Spain even announced temperature limits in public spaces during the 2022 heatwave in an effort to meet these environmental objectives. Spain limited air conditioners to be set no lower than 80°F. No wonder European productivity is 38 percent lower than the US.

Historic preservation laws and strict landlord rules frequently ban exterior window units to maintain aesthetic uniformity.

While air conditioning ownership increases households’ electricity consumption, it may be a small price to pay for comfort and avoiding death.

The problem is not the climate but the policy mindset. Too many European regulators approach energy and technology through the ideological lens of scarcity rather than creative innovation and human flourishing. One reason such policies persist is that the officials who design them are largely insulated from the consequences of their decisions and rarely experience their costs directly. Instead, those costs are borne by millions of ordinary citizens.

Air conditioning is not ultimately a story about cooling. It is a story about knowledge. It transformed oppressive heat into comfort, inhospitable regions into thriving communities, and summer misery into year-round productivity. Coal, copper, and electricity become valuable only after humans discover how to harness them. The history of air conditioning is the history of knowledge triumphing over nature’s constraints.

The ultimate resource is neither energy nor matter. It is the infinite capacity of human beings to learn, create, and discover.

A common argument for government regulation and taxation of tech companies begins with the observation that government research has contributed to the success of those companies. Mariana Mazzucato, professor of the Economics of Innovation and Public Value at University College London, writes:

Much of modern technology came from a collective investment, with public institutions like the US Defense Advanced Research Projects Agency (DARPA) or the European Council for Nuclear Research (CERN), leading the way in the most high-risk capital-intensive phase. What would Google be without the DARPA-funded internet? What would Uber be without the US Navy-funded GPS? What would Apple be without the CIA-funded touch-screen technology and DARPA-funded voice assistant, Siri?

Thinkers like Mazzucato seem to view the state as a sort of partner in these businesses; after all, it’s only fair that a partner should get a cut of the profits and a say in their operations.

“We need to develop a new governance structure, which starts with creating a new vocabulary,” she says. “For example, calling platform companies ‘tech giants’ implies they have invested in the technologies from which they are profiting, when it was really taxpayers who funded the key underlying technologies — from the Internet to GPS.”

This argument is particularly relevant to the case of AI, especially as both Donald Trump and Bernie Sanders have expressed support for partial government ownership of major AI companies. Mazzucato herself suggests that government officials ought “to actively steer [AI’s] development.”

At first glance, the claim that governments are entitled to help control AI companies because they helped create AI sounds plausible. If you were part of building something, don’t you deserve a share of it?

The case for government control of tech companies is far more complicated than it appears, however.

First, note that people are compelled to fund government research. To see why this makes a moral difference, consider a case inspired by the philosopher Michael Huemer.

Suppose you’re an entrepreneur in the beverage industry trying to create a new soda. One day, a rogue food scientist bursts into your office and demands money for his flavor research. He doesn’t ask politely or offer you a contract; he points a gun at you and takes your money. Years later, he develops a delicious new synthetic flavor. You discover it, add it to your soda, and your company takes off, making you a multimillionaire.

Does the food scientist now own part of your company because you used his flavor? Of course not. There’s no doubt your business benefited from his research. Without the flavor he created, your soda might never have existed. But the scientist has already been paid — and it’s worth remembering that he obtained that payment by force. The idea that he’s entitled to additional compensation because you successfully used his research is absurd. Contributing an input does not automatically confer ownership over everything built with that input. Likewise, the fact that government-funded research contributed to AI development does not automatically give the government ownership rights in AI companies.

In fact, the “government investment” argument fails even in a friendlier scenario that doesn’t involve coercion. Imagine that you voluntarily hire the food scientist to develop a new flavor. You agree to pay him $100,000 for his research, and he accepts. You then use the flavor he creates to launch a highly successful soda company.

Again, the food scientist does not own part of your company merely because he contributed to its success. He is entitled to whatever compensation the agreement specifies — nothing more and nothing less. If the contract grants him an equity stake, he has a claim to it. If it doesn’t, he doesn’t. That’s how market exchange generally works. Suppliers of inputs do not automatically acquire ownership of outputs. If the government wants to fund research in exchange for equity, it can try to negotiate those terms in advance. But that’s very different from claiming, after the fact, that successful companies partly belong to the government because some of the knowledge they relied upon emerged from government-funded research.

If merely contributing to a business entitled someone to partial ownership, every business would face endless competing claims from the countless people who helped make it possible. Imagine your local barista claiming partial ownership of the house you built ten years ago because the coffee she sold you helped fuel its construction.

This matters because property rights determine who gets to make decisions about how resources are used. A workable system of property rights requires clear rules for identifying who controls an asset. Without such rules, individuals and firms could never know whether they were free to use, improve, or exchange a resource. In market economies, ownership is generally determined by voluntary agreement, not by the mere fact of having played some causal role in a project’s success. The food scientist is paid as agreed; he does not acquire an open-ended claim on everything his work makes possible. Likewise, even if government-funded research contributed to the development of AI, it does not follow that governments thereby acquire ownership rights over AI companies. Causal contribution may explain how something came into existence, but it is not enough to establish a right to control it.

Public conversations about billionaires tend to oscillate between fascination and condemnation. Headlines emphasize excess, inequality, political influence, or corporate misconduct. And while criticism in some instances is certainly warranted, if we look only through the lens of suspicion, we risk overlooking the unexpected ways private fortunes sometimes become public inheritances.

California has long been a proving ground for where fortunes were spent as quickly as they were made. It is where private ambition often takes physical form in estates, gardens, and grand personal experiments which escape the boundaries of wealth itself, transforming over time to enrich civic life long after their creators are gone.

To illustrate this point, let’s consider the lives of a few remarkable women whose relationships with wealth were strikingly different, yet whose legacies ultimately became public in unexpected ways. Some inherited fortunes. Some accumulated wealth through relationships and social mobility. Others earned influence through ideas rather than vast riches. But in California, each left behind something larger than herself.

Consider Ganna Walska. She was born in Poland in 1887, and reinvented herself repeatedly throughout her life. She moved through elite circles in Europe and America as an opera singer, socialite, and cosmopolitan celebrity. Her wealth came largely through a series of marriages to extraordinarily rich men, including multimillionaire carpet tycoon Alexander Smith Cochran and industrial heir Harold Fowler McCormick. Critics often regarded her as flamboyant and indulgent, a woman better known for glamour than substance. Yet in Santa Barbara, Walska built something extraordinary.

What began as a private estate evolved into Lotusland, now one of the most celebrated botanical gardens in the United States. Walska purchased the property in 1941 and spent decades reshaping it according to her own tastes. She transformed lawns into dramatic cactus collections, sculptural gardens, and exotic landscapes unlike anything else in America. Lotusland made little sense in traditional economic terms, yet its cultural capital is now immense. Visitors from around the world wander its paths, generating tourism, education, and conservation benefits Walska likely never fully anticipated.

Now consider a stranger example in California of how a private indulgence can generate second-order benefits. That of Sarah Winchester, heir to the Winchester rifle fortune. Sarah Lockwood Pardee married William Wirt Winchester in 1862 and the family fortune grew as the company’s rifles became famous in the post–Civil War American West, eventually earning the nickname “the gun that won the West.”

But Sarah’s personal life was marked by profound tragedy. In 1866, Sarah gave birth to a daughter who died only a few weeks later. Then, in 1881, Sarah’s husband William died of tuberculosis. By her early forties, Sarah had lost her family but inherited a vast fortune.

Grief-stricken and increasingly reclusive, Winchester relocated to California and began construction on what became the Winchester Mystery House in San Jose. According to popular legend, spiritual advisors convinced her she was haunted by those killed by Winchester rifles and that continuous building would keep malevolent forces at bay.

For decades, construction continued almost without logic or restraint. The mansion grew into a labyrinth of staircases leading nowhere, doors opening into walls, oddly proportioned rooms, hidden passages, and architectural dead ends. To many contemporaries, the estate appeared little more than irrational excess and a waste of wealth.

Yet history has a curious habit of repurposing private eccentricity into public value. Today, the Winchester Mystery House is one of California’s most beloved tourist attractions. It is a site of fascination, storytelling, and local identity. What looked absurd in one generation became cultural curiosity in another.

And then there is Ayn Rand, who also settled in California but whose story offers a deliberate contrast. Unlike Walska and Winchester, Rand did not inherit a fortune or accumulate one through marriage. Born Alisa Rosenbaum in Russia in 1905, she fled Soviet collectivism for the United States, eventually becoming one of the twentieth century’s most influential defenders of capitalism and individual ambition. Rand’s intellectual work established her philosophy of Objectivism, celebrated builders and creators, and shaped generations of political and economic thought.

During the 1940s, Rand lived with her husband, Frank O’Connor, in the dramatic Von Sternberg House in Southern California. Designed by Richard Neutra for Hollywood director Josef von Sternberg, the house was one of California’s most architecturally significant private homes. Rand called it “unbelievably wonderful.” It was here that she wrote much of Atlas Shrugged, her most ambitious work, but her deep engagement with architecture and beauty had already found full expression in The Fountainhead, completed before she arrived in the San Fernando Valley. That novel, built around a fiercely idealistic architect who refuses to compromise his vision, suggests that Rand understood, perhaps better than most, what it meant to shape physical space as an act of individual will.

But here the pattern breaks with that of Lotusland or the Winchester house. Rand’s California residence did not survive to become a public place. The house was demolished in 1972, after Rand had sold it in 1951, and with it went one of Neutra’s most unusual works. In hindsight, many came to see the demolition as a major cultural loss, and some historians argue that it helped spur the formation of later preservation movements like the Los Angeles Conservancy.

Overall, the contrast between these women is striking. Ganna Walska accumulated wealth through relationships and left behind beauty. Sarah Winchester inherited wealth and left behind mystery. Ayn Rand earned wealth through ideas and intellectual property and left behind a legacy.

California, perhaps more than anywhere else, reminds us that private ambitions have strange afterlives, and this broader perspective matters particularly in an era when the rich are often portrayed only as symbols of inequality or excess. Criticism has its place, but premises matter. If we begin from the assumption that concentrated wealth produces nothing beyond private consumption, we miss the ways history often transforms private visions into public goods, long after the owners of the property pass on.

Undoubtedly, extraordinary wealth creates extraordinary discretion, and billionaires can shape private worlds according to their own tastes and desires. But what is beautiful, bizarre, or deeply personal is up to the owner until their time passes. Critics may dismiss such projects as extreme, and sometimes they are. Yet history often proves less interested in motives than outcomes.

Private estates, as depicted above, have morphed into public treasures, and this pattern stretches far beyond California. Pierre du Pont’s horticultural passions produced Longwood Gardens in Pennsylvania, still one of the finest display gardens in the world. Henry Huntington’s railroad fortune gave rise not only to a legendary art collection and rare manuscript library, but to the stunning botanical gardens at his San Marino estate. The Vanderbilt family’s Biltmore Estate evolved from conspicuous luxury into a regional economic engine. And Rockefeller wealth transformed Kykuit into a cultural institution.

Public debate often treats extraordinary wealth as either proof of virtue or evidence of vice. Reality is usually more nuanced and more surprising. A pleasure garden becomes a sanctuary. A strange mansion becomes folklore. A demolished house becomes the reason a city learns to protect what it has. The rich, it turns out, have a habit of leaving things behind that those who would redirect their wealth never thought to build and couldn’t even imagine.

Thankfully, there are still some college professors who are not afraid to speak their minds on hot-button issues where their views will collide with prevailing academic orthodoxy.

One of them is Duke University professor Adrian Bejan. He has taught mechanical engineering there since 1984 and has authored numerous scientific books with a particular emphasis on constructal law — the organizing principle by which natural phenomena and human-designed systems evolve in a way that facilitates the optimal flow of energy and material through them. He has just published a new book entitled Diversity Through Freedom.In it, he contrasts the beneficial results that stem from diversity in nature and among humans with the harmful results that we see when governments, universities, or other organizations impose their plans for diversity (or equality or other goals) through force.

Bejan’s thinking was shaped by his youth in Romania, then ruled by a communist dictatorship. His family suffered under the regime because his parents were not of the favored “working class.” Bejan recounts how one night his father conspicuously burned many of his books to show that he wasn’t an enemy of the people — but as he explained to his son, it was the least valuable ones that were burned; the most important ones were saved and carefully hidden. In school, Bejan quickly figured out that much of what he was being taught was misleading, manipulative jargon “enrobed in clever metaphors that fool the young.” But he couldn’t be fooled.

In studying natural phenomena, Bejan concluded, “What changes the world is the ability to act, to make change, without fear. The ability does not come top-down from voices in high places. The ability bubbles up from the bottom, in a few enterprising individuals, engineers, builders, entrepreneurs, and doers.” What we should strive for, therefore, is freedom for people to learn and try — equality of opportunity, not equality of result. He often points to sports to make his point. Teams find the best players naturally and they would not be nearly as successful if they were required to make their rosters conform to some imposed notion of “diversity.”

The book abounds in scientific evidence for constructal law, with numerous photographs and charts. The message that will most resonate with AIER readers, I believe, is Bejan’s point that freedom optimizes outcomes while coercion leads to waste and conflict. His observations directly challenge many “progressive” beliefs about society.

Consider, for example, Bejan’s views about the academic world. He writes, “Academia is in trouble when the structure becomes rigid, which happens when those in charge refuse to be questioned because they are an elite, deeply in bed with even more powerful elites such as the government.” Unfortunately, our academic leaders are now much less interested in new ideas than they are in securing as much grant money for their institutions as they can from government officials. “Big money,” Bejan writes, “is funneled to those who promise ‘energy’ materials and ‘live matter’, not to those who dare to speak of fuels, machines and microscopic configurations in motion. Notions from creators with dirty hands are beneath the ruling class of science, which is indoctrinated in reductionism, and marching obediently behind the invisible.” Thus, much of the money that we spend on research is squandered.

Nowhere is the malign influence of academic groupthink more evident than in the quest for artificial diversity. University officials have so thoroughly succumbed to this artificial ideology that it infects the curriculum, hiring decisions, and research projects. Merit counts for much less than the happenstance of a person’s background — whether he or she is from an “underrepresented” group. But Bejan doesn’t think that most of the leaders who bow down to this idea actually believe it. He writes, “In reality, colleges and universities have never been woke. Instead, it’s more apt to understand these institutions as oriented around the interests and worldviews of highly educated and relatively well-off suburban whites — often at the expense of the marginalized and disadvantaged in society — ‘social justice’ discourse notwithstanding.”

Nevertheless, the “diversity” mania marches on. Bejan finds it chillingly similar to other ideological movements in this century where people were rewarded or punished merely because of their class background. He writes, “From Latsis, Timoshenko, and Grossman, we see a project of destroying the individual and replacing him with a new ‘disadvantaged class’ that wins the class struggle by force….It was all an envious and murderous dream and its henchmen are still busy today.”

In sum, nature yields a diversity of talent, which leads to progress and benefits for all. Capitalism works that way, as do competitive sports. Unfortunately, an elite few are not content to allow nature to take its course, demanding instead an artificial system they impose and control. Bejan hits the nail on the head when he states, “The class struggle is a design of unnatural diversity: only two classes, not the natural diversity of individuals with freedom to live, associate voluntarily, and move.”

What does the future hold? Bejan is optimistic that today’s diversity mania will die out “like all the other unnatural prescriptions.” I wish I could share that optimism; the desire of some elitists to dictate how a society must function seems to be more firmly rooted in America than ever and their tools of domination are powerful.

Unemployment Insurance in the Wake of 2020 and the Path to Reform

Executive Summary

The following paper examines unemployment insurance (UI) trust fund solvency before, during, and after the COVID-19 economic downturn of 2020. This paper examined UI trust fund solvency levels for all 50 states and the District of Columbia from 2014 through 2025. The central finding is that state UI systems did not fail or recover uniformly. States entered 2020 with different reserve positions, and those starting conditions shaped their ability to absorb the shock. States that exited federal pandemic UI programs earlier and more fully generally experienced stronger trust fund outcomes, while partial withdrawal, borrowing, and administrative weakness complicated recovery. The evidence is descriptive rather than causal, but it suggests that UI solvency depends on institutional design, fiscal discipline, and administrative execution.

Key Points

This paper finds the following:

State unemployment insurance trust funds entered 2020 with different levels of preparedness. Those with the strongest solvency were better positioned to absorb the 2020 shock and recover afterward.

The COVID-19 economic downturn produced a sharp solvency shock across the board. Some states were hit harder and took longer to recover, depending on their reserve levels, benefit payouts, and financing decisions.

States that exited the federal pandemic unemployment programs earlier in 2021 generally maintained stronger trust funds and recovered faster than states that remained in the program until expiration.

Timing mattered. States that exited earlier tended to see better outcomes, suggesting that prolonged participation may have weakened recovery.

Arkansas, Indiana, Maryland, and Oklahoma attempted to exit the program early but were only partially successful because of legal or administrative obstacles. These cases suggest “partial withdrawal” did not produce the same results as full withdrawal.

Debt and improper payments compounded existing problems. Although improper payments were not the primary drivers of solvency deterioration, states with higher improper payment rates tended to recover more slowly and benefited less from policy changes.

The path forward is to replace the existing framework with personal savings-based alternatives. Personal unemployment insurance savings accounts (PISAs) may improve on the status quo, but universal savings accounts (USAs) offer a broader and potentially stronger alternative.

How a Temporary Crisis Exposed Permanent Weaknesses

The 2026 Department of Labor report on State Unemployment Insurance Trust Fund Solvency notes that only eighteen states meet the minimum solvency standard going into a recession.[1] Conversely, in February 2020, 31 states had solvency levels “greater than or at the recommended minimum solvency standard.”[2]

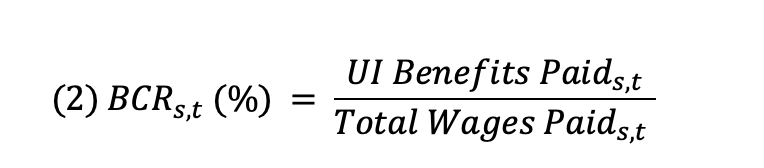

Solvency reflects a state’s ability to pay full unemployment benefits — typically 30 percent to 50 percent of lost wages for up to 26 consecutive weeks — relative to total wages within the state.[3] The current structure is especially vulnerable to the next economic downturn. This paper explores why state UI trust funds experienced such different outcomes after the same national shock. The analysis finds that the interaction between the 2020 shock, pre-2020 trust fund solvency, state policy choices, and administrative capacities all contributed to the variation in solvency outcomes. It also examines how a federal-state program designed for stabilization can weaken fiscal discipline when costs are pooled across governments or pushed onto future taxpayers and employers.

With the federal government facing growing fiscal pressure from rising public debt and structural deficits, the unemployment insurance program cannot rely indefinitely on emergency cash injections to compensate for underlying program weaknesses. While technical fixes aimed at improving program integrity can offer slight improvements, fully replacing UI with universal savings accounts (USAs) can help remove the structural problems that produced the current situation.

The first section briefly outlines unemployment insurance (UI) and where UI policy currently stands. The second section examines UI trust fund solvency before and after the 2020 downturn. The third section explores ways to reduce stress on UI trust funds, including improving program integrity and expanding state flexibility. It also discusses replacing the existing UI system with universal savings accounts. The fourth section concludes. The appendix includes a glossary of key terms, describes the data, and fully discusses model equations and empirical results.

Section 1: What is Unemployment Insurance and How Does it Work?

To understand unemployment insurance, it is important to understand the concept of a reservation price, specifically a reservation wage. A reservation wage is the lowest wage at which someone will accept a job. When someone searches for a job, they look for a job that matches that reservation wage or higher. This comes at the cost of the foregone income you give up by not taking the first job available.

In practice, unemployment insurance (UI) is a joint state-federal program that provides cash benefits to eligible workers who lose their jobs. While states follow uniform federal law, each state administers its own UI program. These programs are funded with taxes on employers based on the wages paid to employees. The taxes are then transferred into trust fund accounts maintained at the US Treasury.[4] There are no federal requirements specifying how much money states must maintain in their trust funds. Instead, states operate on a forward-funding basis, building up reserves during periods of economic growth in anticipation of higher benefit payouts during recessionary periods.[5] The Unemployment Insurance Trust Fund (UTF) is overseen by the Treasury and contains 59 different accounts: 53 state accounts — representing all 50 states, the District of Columbia, Puerto Rico, and the US Virgin Islands — along with four interrelated federal accounts and two accounts associated with the Railroad Retirement Board.[6] For states, these accounts act similarly to a checking account, but understanding how taxpayer dollars flow to these accounts can be complicated.

The modern UI system was created in 1935 through the Social Security Act. At the time, most unemployment insurance options were voluntarily created by employers or established in trade agreements.[7] One exception was the state of Wisconsin, which was the only state to establish an unemployment insurance fund managed by the state government.[8] The creation of the joint federal-state program ushered in a federal unemployment payroll tax that was paired with a tax offset for employers. This structure allowed the federal government to create the financing framework while leaving states substantial discretion over benefit levels, eligibility rules, and program administration. Additionally, different sectors of the economy were given “experience ratings,” which tied the amount of payroll taxes to firms’ “layoff behavior.” Employers who maintain a “stable work force” are assigned favorable tax rates compared with the rates of other employers.[9]

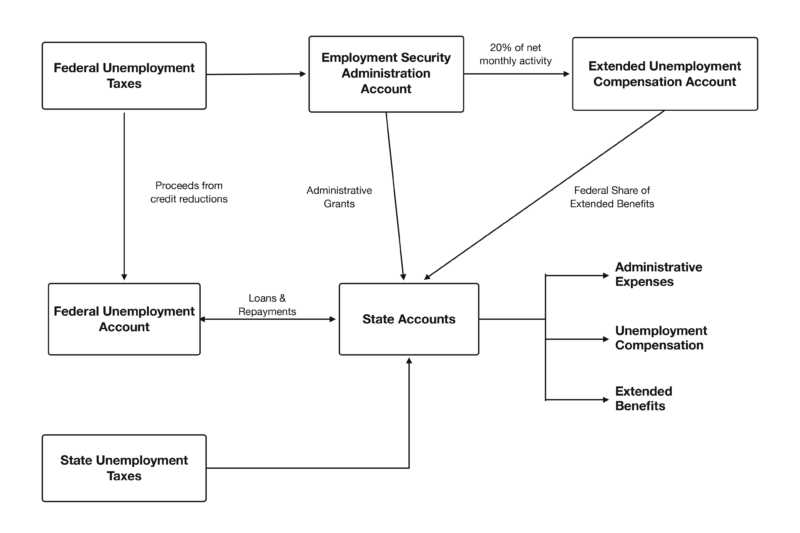

The creation of the mandatory, tax-financed system reshaped the landscape of private and voluntary unemployment insurance arrangements. The program crowded out private unemployment insurance plans using mandatory payroll taxes (coming at the cost of higher employee compensation, a private unemployment insurance plan, or a myriad of other uses) as well as the broader risk-pooling capacity of the public system, backstopped by federal taxpayers. [10] Over time, the program grew in size and scope, introducing new layers of financial and administrative complexity. Coverage broadened from a limited segment of the workforce to include most wage and salary workers. Bene-fit structures converged toward a standard of replacing about half of prior wages for up to 26 weeks. The broader federal program evolved to include mechanisms for extending and increasing benefits during periods of high unemployment. Beginning with temporary programs in the postwar period and culminating in the establishment of a permanent extended benefits framework in 1970, unemployment insurance increasingly incorporated features designed to respond automatically to cyclical downturns.[11] These additions transformed the program from a narrowly defined insurance mechanism into a central component of the federal government’s countercyclical policy toolkit.[12] Figure 1 (below), reproduced from the Bipartisan Policy Center, illustrates how money flows through the UTF.[13]

Figure 1: How Taxpayer Dollars Flow Through the Unemployment Insurance Trust Fund

Sources: Sprick, Emerson. “How Is the Unemployment Insurance Program Financed?” Bipartisan Policy Center. 15 Mar 2022; US Department of Labor.

In Figure 1, previous page, the three accounts (seen in bold) serve the following purposes:

Employment Security Administration Account (ESAA): This is the first destination of most federal unemployment tax revenue. The federal government treats this like a checking account, directing tax revenues in one of three ways:

Funding federal administrative costs of the UI program

Funding state administrative costs by dividing the funds earmarked for administrative purposes into state accounts.

Extended Unemployment Compensation Account (EUCA): This finances the federal government’s share of Extended Benefits costs. The Treasury is statutorily required to transfer 20 percent of ESAA’s net monthly balance (revenue minus distributions) into the EUCA each month.

Federal Unemployment Account (FUA): This provides loans to states that do not have sufficient funds to cover UI benefits. This is funded by loan repayments from state tax dollars and revenue from higher federal unemployment taxes placed on employers when the state has outstanding loans.

Federal Employees Compensation Account (FECA): This account reimburses states for UI benefits paid to former federal employees. Each federal agency transfers money to FECA to cover UI benefits for its workers.[14]

The evolution of the unemployment insurance system introduced new layers of complexity into its financing and governance. While the original design emphasized the accumulation of reserves during periods of economic expansion, repeated downturns exposed weaknesses in state-level programs. In response, the federal government expanded its role through mechanisms that facilitate borrowing, redistributed funds across states, and support extended-benefit payments. Federal borrowing and cross-state financing weakened the link between contributions and payouts, reducing cost discipline.

Public agencies operating under conditions of imperfect oversight and indirect cost allocation tend to expand beyond strictly efficient levels, particularly when their budgets are financed through pooled or opaque revenue sources.[15] The unemployment insurance system’s administrative financing and shared fiscal structure exhibit these characteristics, as costs are spread broadly while decision-making authority remains fragmented.

At the same time, the financing mechanisms embedded in the unemployment insurance system create opportunities for intertemporal cost shifting. Federal lending to state trust funds and the use of deferred tax adjustments allow policymakers to deliver benefits during downturns without imposing immediate, visible costs on taxpayers or employers. This dynamic aligns with James Buchanan’s analysis of public finance, which emphasizes how political actors face incentives to shift the burden of current expenditures into the future, thereby reducing present resistance to spending increases.[16] In the context of unemployment insurance, borrowing and delayed financing mechanisms soften budget constraints and enable benefit expansion during periods of economic stress, while postponing the fiscal adjustments required to restore solvency.

These institutional features are reinforced by increasing reliance on automatic stabilizers within the unemployment insurance system. The development of extended benefit programs and other countercyclical mechanisms allows expenditures to rise without the need for new legislative action. While such features can enhance macroeconomic stabilization, they also reduce the frequency with which policymakers must explicitly weigh the tradeoffs between program generosity and financing. More broadly, the system illustrates a central insight of public choice theory: policy outcomes are shaped not only by stated objectives, but by the incentive structures embedded in institutions.[17] In this case, the combination of decentralized administration, pooled financing, and intertemporal fiscal mechanisms produces a system that is capable of responding flexibly to economic shocks, but one in which the link between costs and benefits is obscured.

It’s also important to note that an unemployed worker is not currently employed but is seeking employment. Those who do not have a job and are not looking for one are counted as not in the labor force.[18] Workers who are not in the labor force are not eligible for UI benefits.

A worker becomes qualified for UI payments if.[19]:

The worker is terminated from a job without cause.

The worker meets work and wage requirements, such as the state’s requirements for wages earned or time worked during a calendar period.

The worker meets any additional state requirements.

To maintain eligibility, workers must file weekly claims, report earnings, job offers and enroll with the State Employment Service to assist the worker in finding employment.[20] These UI benefits are designed to supplement income while workers are searching for a job. By supplementing income, workers can spend more time searching for a job that provides their desired wage. Unfortunately, this system is susceptible to fraud and corruption. As outlined in the introduction, the changes made to UI benefits during the course of the pandemic made unemployment fraud much easier and more widespread.

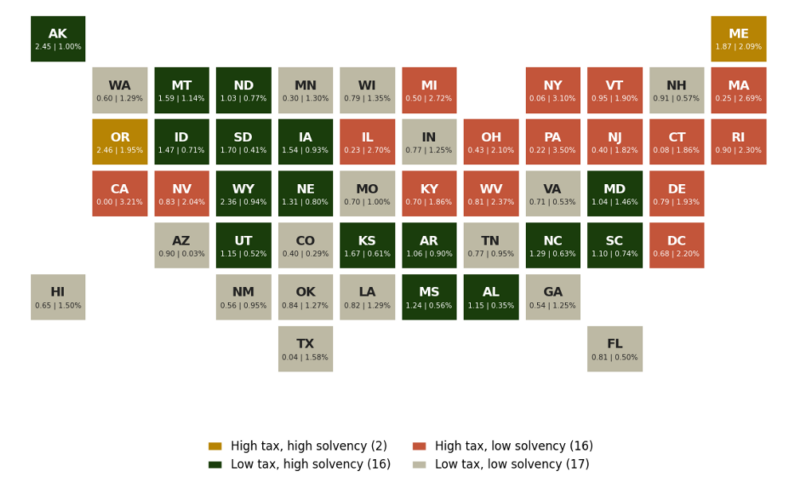

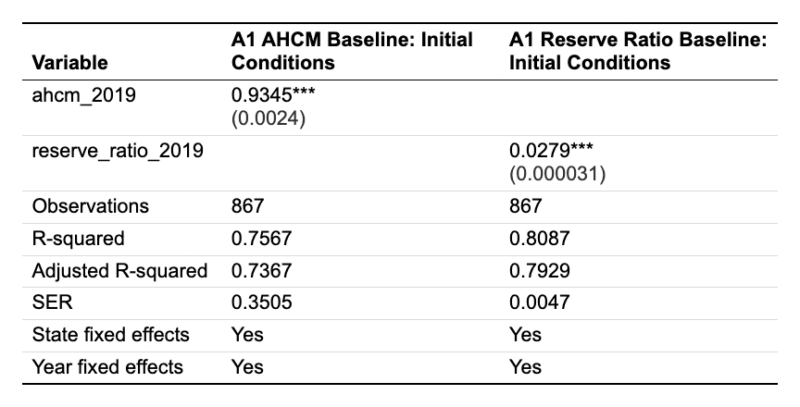

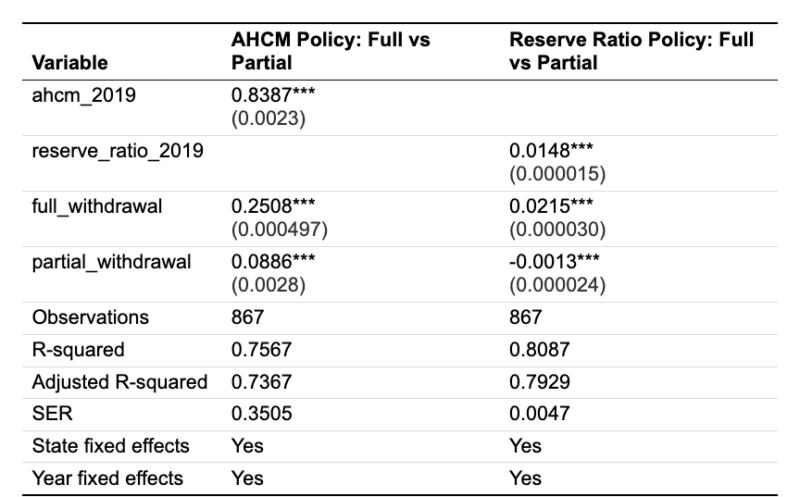

Figure 2 (below) groups states by two measures: trust fund solvency (2026) and estimated unemployment insurance tax burden (2025) using the latest data available at the time of writing this paper.[21],[22] Solvency is measured by the 2026 Average High Cost Multiple (AHCM), with states at or above 1.0 classified as high solvency. Tax burden is measured by the 2025 estimated employer contribution rate as a percentage of taxable wages, with states at or above the national average of 1.74 percent classified as high tax.

Figure 2: Taxation to Solvency Ratios

Notes: Each tile reports state abbreviation, 2026 AHCM, and 2025 estimated employer contribution rate as percent of taxable wages. High solvency = 2026 AHCM ≥ 1.0. Low solvency = 2026 AHCM < 1.0. High tax = 2025 estimated employer contribution rate (% of taxable wages) at or above the U.S. average of 1.74. Low tax = below 1.74. Includes DC; excludes Puerto Rico and the Virgin Islands. Image designed in Python with assistance from ChatGPT.

Sources: U.S. Department of Labor, State Unemployment Insurance Trust Fund Solvency Report 2026; U.S. Department of Labor, Estimated Employer Contribution Rates, Calendar Year 2025.

The most favorable category is low tax, high solvency, shown in dark green. Sixteen states fall into this group: Alabama, Alaska, Arkansas, Idaho, Iowa, Kansas, Maryland, Mississippi, Montana, Nebraska, North Carolina, North Dakota, South Carolina, South Dakota, Utah, and Wyoming. These states combine relatively stronger trust fund positions with below-average UI tax rates.

Only Maine and Oregon fall into the high tax, high solvency category. Sixteen states fall into the high tax, low solvency group, including California, Illinois, New York, Pennsylvania, and several northeastern states. These states face both below-benchmark solvency and above-average tax rates.

The low tax, low solvency category contains seventeen states, including Arizona, Colorado, Florida, Georgia, Indiana, Texas, Virginia, Washington, and Wisconsin. These states have below-average tax rates but a trust fund solvency rate below the 1.0 AHCM benchmark.

The next section explains the patterns shown in Figure 2 (previous page) by examining pre-2020 reserves, the 2020 economic downturn, policy choices, borrowing, and administrative capacity.

Section 2: UI Trust Fund Solvency Before and After 2020