Chibougamau Copper-Gold Project, Canada

HIGHLIGHTS:

- Cygnus sets up value drivers for 2026 with exploration and resource growth a high priority

- At Cedar Bay, Downhole Electromagnetics (‘DHEM’) is in progress to identify follow-up targets from recent intersections1 such as:

- 28.9m at 2.5g/t AuEq (1.0g/t Au, 1.0% Cu & 12.0g/t Ag) (CDR-25-16)

- 10.6m at 4.1g/t AuEq (3.6g/t Au, 0.3% Cu & 2.8g/t Ag) (CDR-25-11W1)

- This is the first time DHEM is being used at Cedar Bay in over 20 years

- Drilling has started at Golden Eye to test extensions below the current resource, which stands at 0.5Mt at 5.6g/t AuEq for 91koz AuEq (Indicated) and 1.2Mt at 4.6g/t AuEq for 182koz AuEq (Inferred)2

- At Joe Mann, a detailed Induced Polarisation (‘IP’) survey is underway to identify walk-up drill targets analogous to IAMGOLD’s Nelligan Complex deposits which contain 4.3Moz Au (M&I) and 7.5Moz Au (Inferred)3 located just 10km west of Joe Mann

- Permits are being submitted for the Gwillim prospect for drilling in the coming quarter; This will co-funded by 50% JV partner Alamos Gold, which has a market capitalisation of ~C$25B. Initial targets will follow up historic intersections4 of:

- 7.6m @ 38.1g/t Au from 314.9m (87-KOD-18);

- 15.2m @ 9.4g/t Au from 155.1m (87-KOD-1); and

- 16.4m @ 8.3g/t Au from 168.3m (87-KOD-10).

- Cygnus believes there is significant potential to continue growing the Chibougamau resource, which stands at 6.4Mt at 3% CuEq for 193kt CuEq (M&I) and 8.5Mt at 3.5% CuEq for 295kt CuEq (Inferred)2

| Cygnus Executive Chairman David Southam said: ‘There is overwhelming evidence which points to the potential for substantial resource growth at Chibougamau. The resources remain open in many places and we have a pipeline of compelling targets to test.

‘We have devised an extensive program of drilling and geophysics to unlock this upside. This will include brownfields drilling as well as testing new targets. After growing the resource by 29 per cent last year, we are confident that our exploration strategy will deliver more strong results and create more value for shareholders.

‘We are now drilling at Golden Eye and Cedar Bay, which provide substantial resource upside.

‘Joe Mann and Gwillim have excellent discovery potential and have been materially overlooked for the last 20 years. With this potential and the current gold price we are excited to commence exploration on these targets’. |

Cygnus Metals Limited (ASX: CY5; TSXV: CYG,OTC:CYGGF; OTCQB: CYGGF) (‘Cygnus’ or the ‘Company’) is pleased to announce the start of extensive exploration programs aimed at growing the resources at its Chibougamau Copper-Gold Project in Quebec.

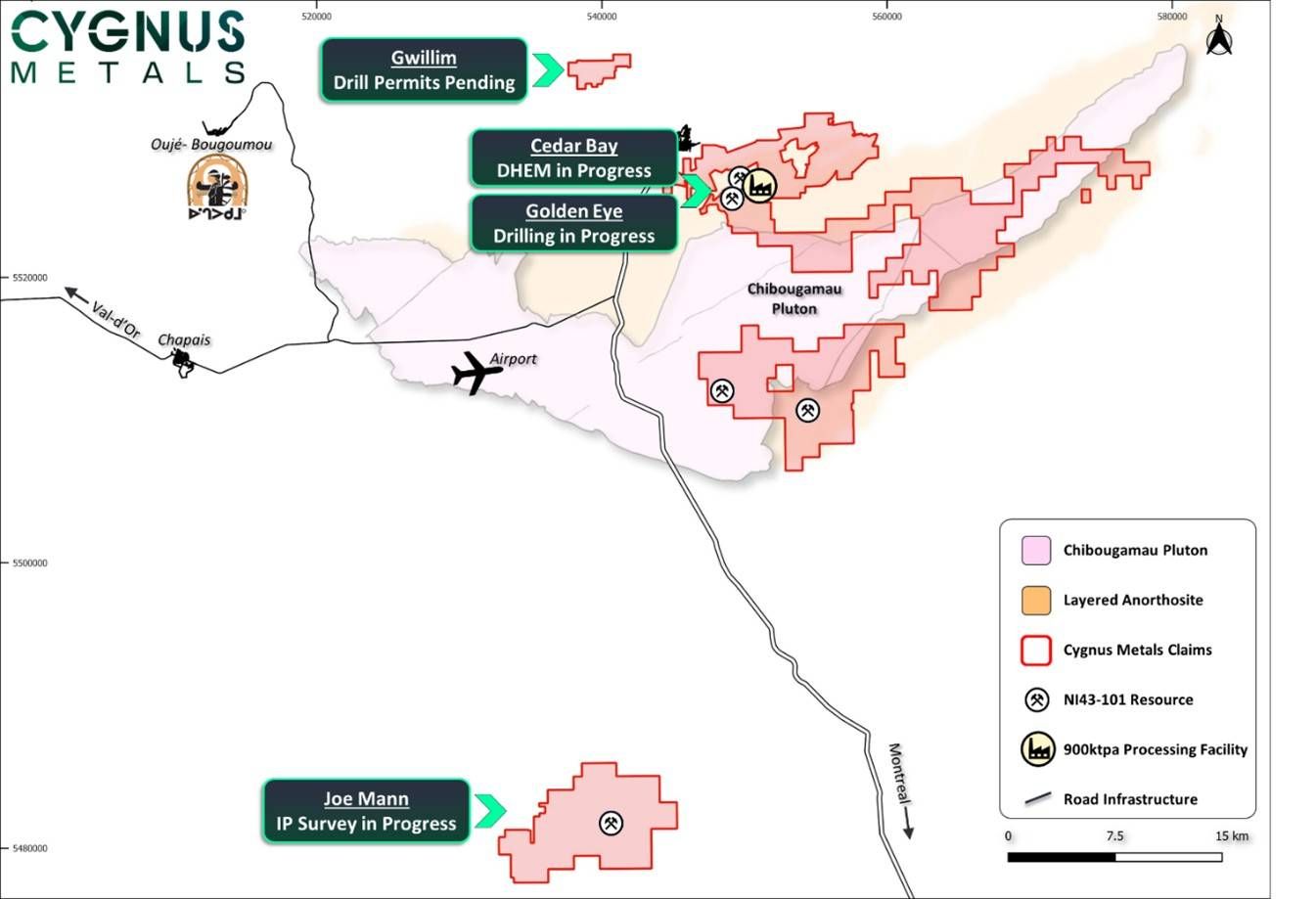

Resource growth and discovery remain a key pillar of Cygnus’ growth strategy as the Company continues to unlock the Chibougamau district. A key focus is brownfields exploration, including extensions to deposits such as Cedar Bay and Golden Eye.

At Cedar Bay, Downhole Electromagnetics (‘DHEM’) is in progress to define follow up drill targets from recent exploration drilling1 which returned:

- 28.9m at 2.5g/t AuEq (1.0g/t Au, 1.0% Cu & 12.0g/t Ag) (CDR-25-16)

- 10.6m at 4.1g/t AuEq (3.6g/t Au, 0.3% Cu & 2.8g/t Ag) (CDR-25-11W1)

Recent drilling successfully demonstrated extensions to the current resource at Cedar Bay of 0.3Mt at 8.1g/t AuEq for 67koz (M&I) and 0.8Mt at 7.8g/t AuEq for 205koz (Inferred).2 DHEM aims to define resource extensions as well as identifying high grade shoots which are typically associated with semi massive sulphides. This will be the first time DHEM is being used at Cedar Bay in over 20 years, presenting a huge opportunity for Cygnus.

At Golden Eye, drilling has commenced with three rigs to grow the Indicated Resource and extend the resource below the currently defined depth of just 450m. Golden Eye was a new resource defined by Cygnus last year of 0.5Mt at 5.6g/t AuEq for 91koz (Indicated) and of 1.2Mt at 4.6g/t AuEq for 182koz (Inferred)2 and remains open at depth with one of the deepest intersections5 from last year of:

- 2.9m @ 10.2g/t AuEq (8.3g/t Au, 1.4% Cu & 3.3g/t Ag) from 463.8m (LDR-25-08)

The Company also has a strong focus on defining new resources and making discoveries. Two key areas identified as high priority are gold targets Joe Mann and Gwillim.

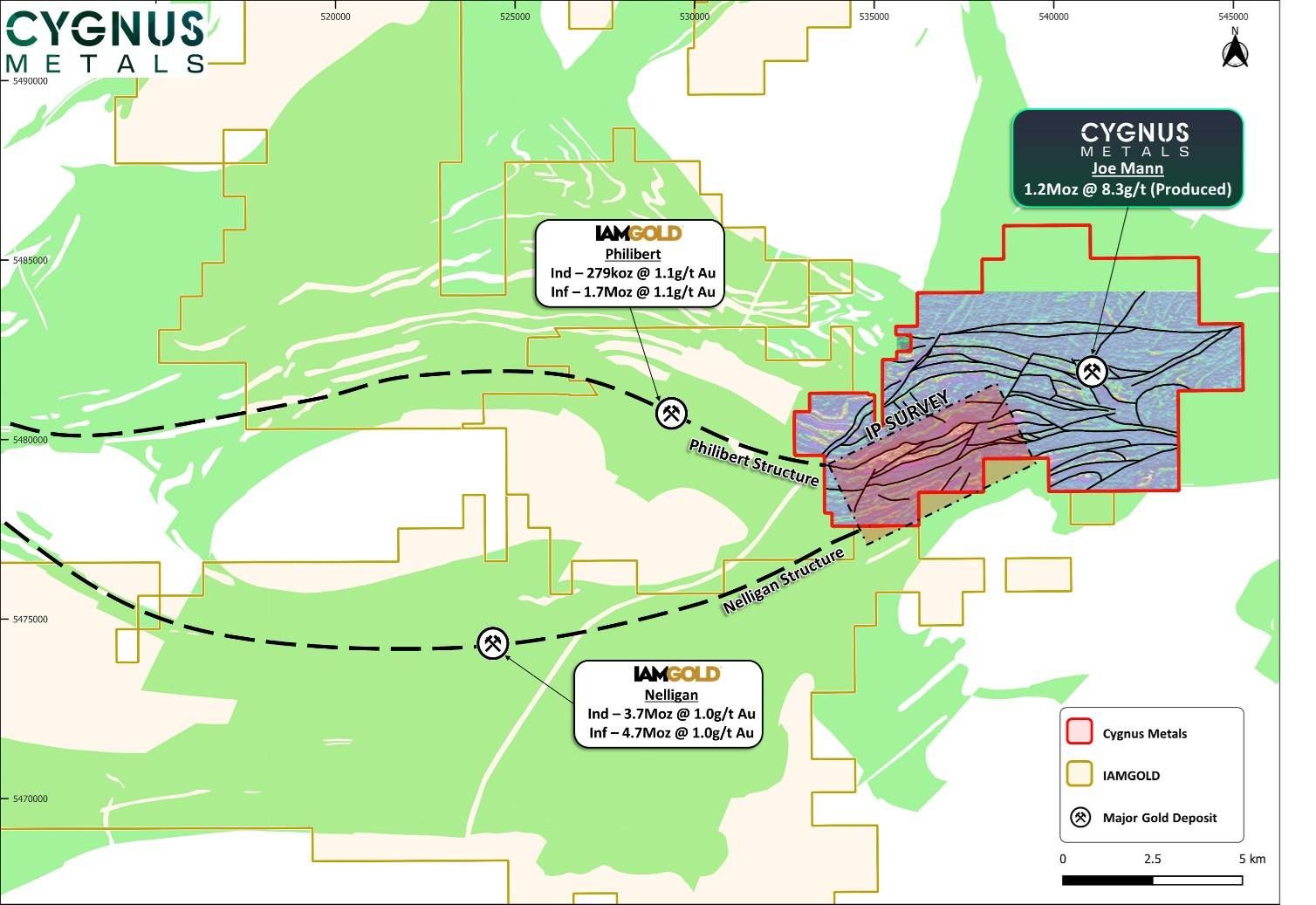

At Joe Mann, the Company has commenced a detailed Induced Polarisation (‘IP’) survey along major structures to identify walk-up drill targets for Q2 this year. Cygnus is targeting analogous mineralisation to IAMGOLD’s Nelligan Complex, which is located just 10km west of the project and contains 4.3Moz Au (M&I) and 7.5Moz Au (Inferred).3

This survey will help to generate further drill targets in addition to some of the high-grade historic intersections which also require follow up.4 These include:

- 0.7m @ 480.2g/t Au from 92.3m (H-118);

- 3.8m @ 20.8g/t Au from 287.2m (H-214); and

- 8.4m @ 6.3g/t Au from 175.6m (H-374).

At Gwillim, permits are underway for drilling to commence in the coming quarter. Drilling at Gwillim will be co-funded by 50% JV partner Alamos Gold, which has a market capitalisation of ~C$25B. Gwillim is just 12km from the Chibougamau processing facility and has high potential for defining new resources. Initial drilling will focus on following up high-grade historic intersections4 such as:

- 7.6m @ 38.1g/t Au from 314.9m (87-KOD-18);

- 15.2m @ 9.4g/t Au from 155.1m (87-KOD-1); and

- 16.4m @ 8.3g/t Au from 168.3m (87-KOD-10).

The Chibougamau area has well-established infrastructure, giving the Project a significant headstart as a copper-gold development opportunity. This infrastructure includes a 900,000tpa processing facility, local mining town, sealed highway, airport, regional rail infrastructure and 25kV hydro power to the processing site. Significantly, the Chibougamau processing facility is the only processing facility within a 250km radius.

Figure 1: Exploration progressing across mutiple fronts with a focus on both resource extensions and discovery

Figure 2: Joe Mann IP survey covering key structures from IAMGOLD’s major deposits Nelligan and Phillibert3

This announcement has been authorised for release by the Board of Directors of Cygnus.

David Southam

Executive Chair

T: +61 8 6118 1627

E: info@cygnusmetals.com |

Nicholas Kwong

President & CEO

T: +1 647 921 0501

E: info@cygnusmetals.com |

Media:

Paul Armstrong

Read Corporate

T: +61 8 9388 1474 |

About Cygnus Metals

Cygnus Metals Limited (ASX: CY5, TSXV: CYG,OTC:CYGGF, OTCQB: CYGGF) is a diversified critical minerals exploration and development company with projects in Quebec, Canada and Western Australia. The Company is dedicated to advancing its Chibougamau Copper-Gold Project in Quebec with an aggressive exploration program to drive resource growth and develop a hub-and-spoke operation model with its centralised processing facility. In addition, Cygnus has quality lithium assets with significant exploration upside in the world-class James Bay district in Quebec, and REE and base metal projects in Western Australia. The Cygnus team has a proven track record of turning exploration success into production enterprises and creating shareholder value.

Forward Looking Statements

This release may contain certain forward-looking statements and projections regarding estimates, resources and reserves; planned production and operating costs profiles; planned capital requirements; and planned strategies and corporate objectives. Such forward looking statements/projections are estimates for discussion purposes only and should not be relied upon. They are not guarantees of future performance and involve known and unknown risks, uncertainties and other factors, many of which are beyond Cygnus’ control. Cygnus makes no representations and provides no warranties concerning the accuracy of the projections and disclaims any obligation to update or revise any forward-looking statements/projections based on new information, future events or otherwise except to the extent required by applicable laws. While the information contained in this release has been prepared in good faith, neither Cygnus or any of its directors, officers, agents, employees or advisors give any representation or warranty, express or implied, as to the fairness, accuracy, completeness or correctness of the information, opinions and conclusions contained in this release. Accordingly, to the maximum extent permitted by law, none of Cygnus, its directors, employees or agents, advisers, nor any other person accepts any liability whether direct or indirect, express or limited, contractual, tortuous, statutory or otherwise, in respect of the accuracy or completeness of the information or for any of the opinions contained in this release or for any errors, omissions or misstatements or for any loss, howsoever arising, from the use of this release.

End Notes

- Refer to Cygnus’ ASX announcements dated 30 October 2025 and 8 December 2025.

- Refer to Cygnus’ ASX announcement dated 17 September 2025 and subsequent technical report dated 31 October 2025 titled ‘NI 43-101 Technical Report Chibougamau Hub and Spoke Complex, Québec, Canada’ prepared in accordance with National Instrument 43-101 Standards of Disclosure for Mineral Projects (‘NI 43-101’) and the Joint Ore Reserves Committee (JORC) Code (2012 Edition).

- Refer to IAMGOLD’s news release dated 17 February 2026.

- Refer to Cygnus’ ASX announcement dated 20 January 2026.

- Refer to Cygnus’ ASX announcement dated 8 May 2025.

Qualified Persons and Compliance Statements

The scientific and technical information in this announcement has been reviewed and approved by Mr Louis Beaupre, the Quebec Exploration Manager of Cygnus, a ‘qualified person’ as defined in National Instrument 43-101 – Standards of Disclosure for Mineral Projects.

The information in this release that relates to the Mineral Resource Estimate for the Chibougamau Project reported in accordance with the JORC Code (2012 Edition) and NI 43-101 was released by Cygnus in an announcement titled ‘Major Resource Update’ released to the ASX on 17 September 2025 and subsequent technical report dated 31 October 2025 titled ‘NI 43-101 Technical Report Chibougamau Hub and Spoke Complex, Québec, Canada’ prepared in accordance with National Instrument 43-101 Standards of Disclosure for Mineral Projects (‘NI 43-101’) and the JORC Code (2012 Edition). Details of the Mineral Resource Estimate are included in Appendix A.

The information in this announcement that relates to previously reported Exploration Results at the Company’s projects has been previously released by Cygnus in ASX Announcements as noted in the End Notes.

Individual grades for the metals included in the metal equivalents calculations for the Mineral Resource Estimate, as well as the price assumptions, metallurgical recoveries and metal equivalent calculations themselves, are in Appendix A of this release. Individual grades for the metals included in the metal equivalents calculation for the exploration results are in the original market announcements. Metal equivalents for exploration results have been calculated at a copper price of US$8,750/t, gold price of US$2,350/oz and silver price of US$25/oz, with copper equivalents calculated based on the formula CuEq(%) = Cu(%) + (Au(g/t) x 0.77258)+(Ag(g/t) x 0.00822). Metallurgical recovery factors have been applied to the copper equivalents calculations for the exploration results, with copper metallurgical recovery assumed at 95% and gold metallurgical recovery assumed at 85% based upon historical production at the Chibougamau Processing Facility, and the metallurgical results contained in Cygnus’ announcement dated 28 January 2025. It is the Company’s view that all elements in the copper and gold equivalent calculations have a reasonable potential to be recovered and sold.

Cygnus is not aware of any new information or data that materially affects the information in these announcements, and in the case of estimates of Mineral Resources, that all material assumptions and technical parameters underpinning the estimates in the relevant market announcement continue to apply and have not materially changed. The Company confirms that the form and context in which the Competent Persons’ findings are presented have not been materially modified from the original market announcements.

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

APPENDIX A – Mineral Resource Estimate for the Chibougamau Project as at 17 September 2025

Cu

Project |

Classification |

COG

CuEq |

Tonnage |

Average Grade |

Contained Metal |

| Cu |

Au |

Ag |

CuEq |

AuEq |

Cu |

Au |

Ag |

CuEq |

AuEq |

| % |

Mt |

% |

g/t |

g/t |

% |

g/t |

kt |

koz |

koz |

kt |

koz |

| Corner Bay |

Indicated |

1.2 |

4.9 |

2.5 |

0.3 |

8.4 |

2.8 |

4.1 |

124 |

43 |

1,316 |

137 |

638 |

| Inferred |

5.4 |

2.7 |

0.2 |

8.9 |

3.0 |

4.3 |

146 |

41 |

1,543 |

159 |

744 |

| Devlin |

Measured |

1.5 |

0.1 |

2.7 |

0.3 |

0.5 |

2.9 |

4.7 |

4 |

1 |

2 |

4 |

19 |

| Indicated |

0.6 |

2.0 |

0.2 |

0.2 |

2.1 |

3.4 |

13 |

4 |

5 |

13 |

69 |

| M&I |

0.8 |

2.1 |

0.2 |

0.3 |

2.3 |

3.6 |

16 |

5 |

7 |

17 |

88 |

| Inferred |

0.3 |

2.0 |

0.2 |

0.3 |

2.1 |

3.4 |

7 |

2 |

3 |

7 |

36 |

| Joe Mann |

Inferred |

2.0 |

0.7 |

0.2 |

6.0 |

– |

4.6 |

6.3 |

2 |

143 |

– |

34 |

151 |

| Cedar Bay |

Indicated |

1.8 |

0.3 |

1.6 |

6.0 |

9.9 |

6.4 |

8.1 |

4 |

50 |

82 |

16 |

67 |

| Inferred |

0.8 |

2.0 |

5.1 |

11.8 |

6.1 |

7.8 |

17 |

134 |

309 |

50 |

205 |

| Golden Eye |

Indicated |

0.5 |

1.0 |

4.3 |

9.9 |

4.4 |

5.6 |

5 |

69 |

161 |

22 |

91 |

| Inferred |

1.2 |

0.9 |

3.4 |

7.9 |

3.6 |

4.6 |

11 |

134 |

313 |

45 |

182 |

| Project |

Classification |

Tonnage |

Average Grade |

Contained Metal |

| Cu |

Au |

Ag |

CuEq |

AuEq |

Cu |

Au |

Ag |

CuEq |

AuEq |

| Mt |

% |

g/t |

g/t |

% |

g/t |

kt |

koz |

koz |

kt |

koz |

| Hub and Spoke |

Measured |

0.1 |

2.7 |

0.3 |

0.5 |

2.9 |

4.7 |

4 |

1 |

2 |

4 |

19 |

| Indicated |

6.3 |

2.3 |

0.8 |

7.8 |

3.0 |

4.3 |

146 |

166 |

1,563 |

189 |

865 |

| M&I |

6.4 |

2.3 |

0.8 |

7.6 |

3.0 |

4.3 |

149 |

167 |

1,565 |

193 |

884 |

| Inferred |

8.5 |

2.1 |

1.7 |

7.9 |

3.5 |

4.8 |

182 |

454 |

2,168 |

295 |

1,318 |

Notes:

- Cygnus’ Mineral Resource Estimate for the Chibougamau Copper-Gold project, incorporating the Corner Bay, Devlin, Joe Mann, Cedar Bay, and Golden Eye deposits, is reported in accordance with the JORC Code and the Canadian Institute of Mining, Metallurgy and Petroleum (‘CIM’) (2014) definitions in NI 43-101.

- Mineral Resources are estimated using a long-term copper price of US$9,370/t, gold price of US$2,400/oz, and silver price of US$30/oz, and a US$/C$ exchange rate of 1:1.35.

- Mineral Resources are estimated at a CuEq cut-off grade of 1.2% for Corner Bay and 1.5% CuEq for Devlin. A cut-off grade of 1.8 g/t AuEq was used for Cedar Bay and Golden Eye; and 2.0 g/t AuEq for Joe Mann.

- Corner Bay bulk density varies from 2.85 tonnes per cubic metre (t/m3) to 3.02t/m3 for the estimation domains and 2.0 t/m3 for the overburden. At Devlin, bulk density varies from 2.85 t/m3 to 2.90 t/m3. Cedar Bay, Golden Eye, and Joe Mann use a bulk density of 2.90 t/m³ for the estimation domains.

- Assumed metallurgical recoveries are as follows: Corner Bay copper is 93%, gold is 78%, and silver is 80%; Devlin copper is 96%, gold is 73%, and silver is 80%; Joe Mann copper is 95%, gold is 84%, and silver is 80%; and Cedar Bay and Golden Eye copper is 91%, gold is 87%, and silver is 80%.

- Assumptions for CuEq and AuEq calculations (set out below) are as follows: Individual metal grades are set out in the table. Commodity prices used: copper price of US$9,370/t, gold price of US$2,400/oz and silver price of US$30/oz. Assumed metallurgical recovery factors: set out above. It is the Company’s view that all elements in the metal equivalent calculations have a reasonable potential to be recovered and sold.

- CuEq Calculations are as follows: (A) Corner Bay = grade Cu (%) + 0.68919 * grade Au (g/t) + 0.00884 * grade Ag (g/t) ; (B) Devlin = grade Cu (%) + 0.62517 * grade Au (g/t) + 0.00862 * grade Ag (g/t); (C) Joe Mann = grade Cu (%) + 0.72774* grade Au (g/t); and (D) Golden Eye and Cedar Bay = grade Cu (%) + 0.78730* grade Au (g/t) + 0.00905 * grade Ag (g/t).

- AuEq Calculations are as follows: (A) Corner Bay = grade Au (g/t) + 1.45097* grade Cu(%)+0.01282* grade Ag (g/t); (B) Devlin = grade Au (g/t) + 1.59957* grade Cu(%)+0.01379* grade Ag (g/t); (C) Joe Mann = grade Au (g/t) + 1.37411* grade Cu (%); and (D) Cedar Bay and Golden Eye = grade Au (g/t) + 1.27016 * grade Cu (%) + 0.01149 * grade Ag (g/t).

- Wireframes were built using an approximate minimum thickness of 2 m at Corner Bay, 1.8 m at Devlin, 1.2 m at Joe Mann, and 1.5 m at Cedar Bay and Golden Eye.

- Mineral Resources are constrained by underground reporting shapes.

- Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability.

- Totals may vary due to rounding.

Photos accompanying this announcement are available at:

https://www.globenewswire.com/NewsRoom/AttachmentNg/9f3d9271-0c1d-4946-b6b7-907187bb4f3a

https://www.globenewswire.com/NewsRoom/AttachmentNg/bf51280f-9701-4436-8255-c21949f90dfe

Locksley Resources (LKY:AU) has announced LKY Commences Diamond Drilling at Desert Antimony Mine

Locksley Resources (LKY:AU) has announced LKY Commences Diamond Drilling at Desert Antimony Mine

Aurum Resources (AUE:AU) has announced Boundiali Resource Grows to 3Moz – Indicated Up 49%

Aurum Resources (AUE:AU) has announced Boundiali Resource Grows to 3Moz – Indicated Up 49%

Brightstar Resources (BTR:AU) has announced High-grade assays incl 4m @ 26.7g/t Au in Sandstone drilling

Brightstar Resources (BTR:AU) has announced High-grade assays incl 4m @ 26.7g/t Au in Sandstone drilling