The Social Security Trustees’ annual report delivered another warning last week: the program’s finances have deteriorated further, insolvency is approaching sooner, and demographic changes are mostly to blame.

That’s only part of the story.

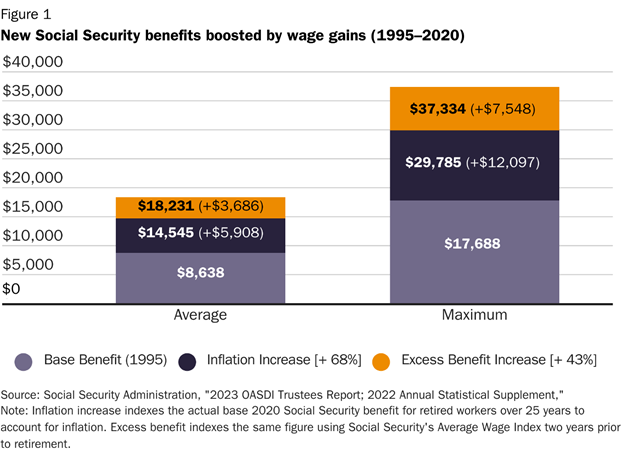

Social Security contains two automatic benefit expansions. First, initial benefits rise with wages, meaning each new generation receives higher inflation-adjusted benefits than the last. Second, retirement ages have not kept pace with increases in longevity, allowing retirees to collect those larger benefits for more years. Together, these policies consistently increase lifetime benefits.

Two workers with equivalent earnings histories and payroll tax contributions can receive very different benefits simply because one retired later. The graphic below illustrates how workers’ initial benefit amounts have grown over 25 years due to wage growth indexing, compared with inflation.

It is one thing to maintain a constant standard of living in retirement while people live longer. It is another to simultaneously increase the number of years benefits are paid and the generosity of those benefits. But that is effectively what Social Security has done for decades.

John Cogan and Daniel Heil, writing in 2023, examine a counterfactual scenario in which Congress adopted price indexing of initial benefits (i.e., holding initial benefits constant in inflation-adjusted terms) instead of wage indexing. They find that such an approach would have generated consistent cash-flow surpluses from the mid-1980s onward, thereby avoiding the deficits that emerged after 2010 and are now depleting trust fund reserves.

Contrary to the common narrative, Social Security’s looming insolvency is not merely the product of bad demographic luck. It is also the predictable consequence of policy choices that automatically increase both benefit levels and benefit duration.

Changing to price indexing, beginning in 2032, when the program runs out of IOUs, would close 74 percent of the program’s long-term funding gap and lead to a surplus after 2078.

The good news is that Congress could eliminate most of Social Security’s long-term financing gap without cutting anyone’s benefit and without reducing the purchasing power of benefits. Legislators just need to get comfortable with slowing the growth of benefits.

Wage indexing of initial benefits also helps explain why economic growth alone cannot rescue Social Security. Economic growth means more revenue, but it also means larger benefit promises, as both payroll taxes and new benefits would grow with wage gains.

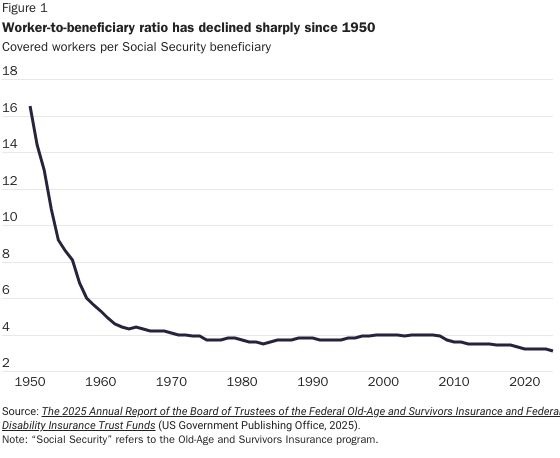

Ever-rising benefits might have looked affordable when Social Security was supported by a large and growing workforce. In 1950, there were roughly 16 covered workers for every beneficiary. Today there are about three (see chart below). Yet the program still operates as if every generation will be larger than the one before it — even as the population pyramid steadily inverts.

Many advanced economies faced similar demographic pressures decades ago. Aging populations, lower fertility rates, and rising pension costs forced governments to rethink retirement policy globally.

Most did not simply raise taxes to preserve existing promises. Doing so undermines the very economic growth that enables younger workers to support an aging society. Instead, they modernized their retirement systems, slowing the growth of benefits and adopting automatic adjustment policies.

Based on analysis in my book with Ivane Nachkebia, Reimagining Social Security, successful retirement systems are designed to adapt automatically to changing economic and demographic realities, rather than relying on political action in the face of a financing crisis.

Perhaps the best example is automatically increasing eligibility ages with improvements in longevity.

When Social Security was created in 1935, life expectancy was far lower than it is today. Life expectancy at age 65 has increased by more than six years for men and more than seven years for women. Yet the program’s full retirement age has risen by only two years, from 65 to 67. Seniors can now expect to spend nearly two decades collecting benefits.

Sweden now links retirement ages to life expectancy, and roughly one-quarter of OECD countries have adopted similar mechanisms. Such policies recognize that as people live longer, retirement systems cannot indefinitely increase both monthly benefits and years in retirement without imposing growing burdens on workers.

The increasingly favored alternative in Washington is to rely primarily on higher taxes, especially raising or eliminating the payroll tax cap ($184,500 in 2026). This is the threshold above which higher earners no longer face Social Security’s 12.4 percent burden, which also caps their ultimate benefits.

It’s a popular proposal, easily summed up as: make someone else pay. But it’s often oversold.

Even eliminating the cap would close only about half of the program’s long-term financing gap while massively increasing marginal tax rates for highly productive professionals. Affected wage earners would include physicians, surgeons, pilots, and small-business owners, potentially accelerating early retirements and worsening labor shortages in key industries.

Before asking Americans to pay more, Congress should consider whether a benefit formula that automatically increases benefits from one generation to the next still makes sense in a country where retirees are on average wealthier than the younger households whose payroll taxes finance their benefits.

The lesson from this year’s Trustees report is not merely that Social Security is running short of money. It is that the program automatically promises larger benefits to successive generations and pays those benefits for increasingly longer retirements, even as the number of workers supporting each beneficiary shrinks.

That is not simply a demographic challenge. It is a policy choice.

And until Congress confronts that mismatch, younger generations will be asked to pay ever more to sustain an untenable status quo that much of the developed world has already left behind.