When will the Federal Reserve finally stop losing money? The Fed has been effectively bankrupt (operating at a loss) since 2023 because the interest it pays to banks each month exceeds the returns on its assets. But these losses are a policy decision that the Fed can end at any time.

Since October 2008, the Fed has been paying interest to private commercial banks. Banks currently earn 3.65 percent interest on reserves (IOR) that they hold at the Fed. According to their 2025 financial statements, the Fed paid almost $167 billion in interest to US depository institutions and overnight reverse repurchase agreements (ON RRPs), but it earned less than $155 billion on its assets. This resulted in a net loss of more than $12 billion in 2025. The cumulative total losses since 2023 stand at $243 billion. If the Federal Open Market Committee (FOMC) raises its interest rate targets this year, as financial markets are predicting, future losses could be even greater.

Why is a government institution like the Fed paying interest to private banks? What role does IOR play in the Fed’s monetary policy, and what problems might it cause?

The Start of IOR

In early 2008, many banks and nonbank financial institutions experienced huge losses as market values of mortgage loans and mortgage-backed securities (MBSs) collapsed. The Fed initially opened several major lending programs to provide liquidity to the banking and financial systems. To prevent general liquidity from increasing (and driving up prices), the Fed sold Treasury securities. By sterilizing its lending programs with Treasury sales, the Fed was able to provide liquidity to the banking system without increasing inflation.

By late summer, the scale of the lending facilities caused the Fed’s Treasury holdings to dwindle. This created a problem for Fed officials, who were worried about the “upside risks to inflation.” They thought additional lending and large-scale asset purchases would be necessary to prevent the banking system from failing. But they no longer had enough Treasurys to sell to prevent that lending from driving up prices. How could the Fed continue to provide liquidity to the banking system without increasing inflation?

The Fed’s solution to this problem was to pay banks interest to hold their reserves at the Fed. By paying interest on reserves (IOR), the Fed could create the reserves necessary to extend loans to and purchase risky MBSs from banks, thereby strengthening those banks’ balance sheets, while giving banks a strong incentive to hold the newly created reserves rather than lending them out. So long as banks increased their reserve-to-deposit ratios sufficiently, the newly created reserves would not increase broader monetary aggregates, spending in the economy, or inflation.

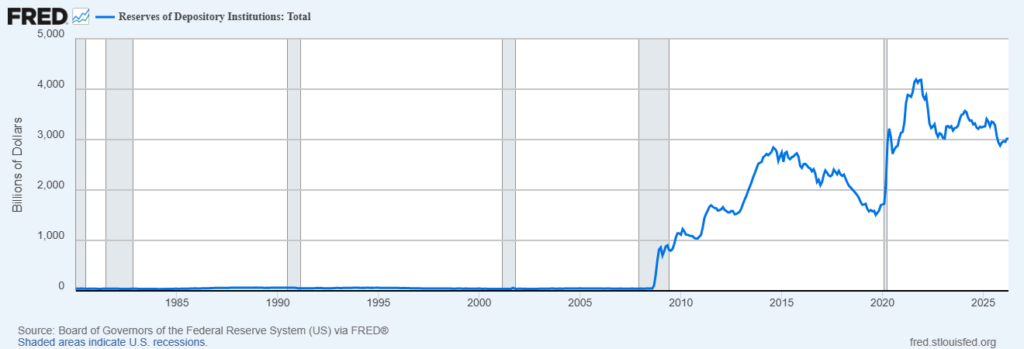

The plan worked. Paying banks to hold reserves caused the reserve-to-deposit ratio to rise. Total reserves in the banking system increased from $45 billion at the start of 2008 to $1.2 trillion by 2010 and $2.8 trillion in 2014. Banks’ asset and deposit growth, however, slowed over this period, causing their reserve ratios to jump.

The Fed’s Floor System

The introduction of IOR moved the Fed from a corridor system of monetary policy, in which the Fed targets short-term interest rates within some range, to a floor system in which IOR creates a lower bound, below which short-term rates cannot fall. The transition, however, was anything but smooth.

The Fed first paid IOR on October 9, 2008 at a rate of 1.4 percent. The following day, the federal funds rate, the market rate at which banks borrow from and lend to each other, fell to just 0.79 percent, and the rate on three-month US Treasury was just 0.25 percent. Short-term interest rates were trading below the supposed floor, and continued to do so for almost a decade.

Rather than admit that the floor system was not functioning as expected, the FOMC moved from a target rate to a target rate range. The rate of IOR was set as the top of the range, with zero being the bottom. In 2014, the FOMC introduced a facility for ON RRPs, which functions like IOR for nonbank financial institutions. The ON RRP rate is typically set at the bottom of the FOMC’s target range.

Under the floor system, the rate of IOR has become the primary tool of Fed policy. The Fed still buys and sells bonds, but these open market operations are intended to alter the quantity of reserves in the banking system and (in theory) do not affect short-term interest rates. Large-scale QE purchases do influence interest rates, but they are intended to target longer-term interest rates in the financial system rather than short-term rates and bank lending.

The move to a floor system is arguably the biggest change to monetary policy in the history of the Fed. It has led commercial banks to accumulate a massive quantity of reserves, which have increased bank liquidity while reducing bank lending. In a study published in the Journal of Macroeconomics in 2021, I found that IOR accounted for more than half of the decline in bank lending in the decade following the 2008 financial crisis. The floor system did not work as planned and has made monetary policy more complicated.

Fed officials argue that paying IOR is beneficial since it gives them more tools in the monetary policy toolkit. Given the Fed’s past failures, however, one might question whether more tools will lead to better policy.

Will Chair Warsh allow the Fed to continue to take losses? Reducing the rate of IOR (at least relative to its interest rate targets) could improve the Fed’s fiscal position so that it behaves more responsibly and finally stops losing money.