As Social Security reaches its ninety-first anniversary this August, it’s running out of room for evasion. The 2026 Trustees Report projects Old-Age and Survivors Insurance (OASI) trust fund will be depleted by the fourth quarter of 2032, after which dedicated revenue would only cover 78 percent of scheduled benefits. On a combined basis with Disability Insurance, reserves would run out in late 2034, with 83 percent payable then and 65 percent by 2100.

The current schedule and financing cannot survive under existing law. That is the setting for Romina Boccia and Ivane Nachkebia’s Reimagining Social Security. Nearly a year after its release, the book is more relevant than ever.

The authors argue that Social Security should return to the program’s original purpose: old-age poverty protection. As President Roosevelt warned, “We can never insure one hundred percent of the population against one hundred percent of the hazards and vicissitudes of life.” Yet the program has become both a redistribution and a public pension promise for nearly everyone, making it politically untouchable.

The book draws lessons from Canada, Germany, New Zealand, and Sweden. Its reform menu includes a higher retirement age, a flatter benefit, automatic balancing mechanisms, and expanded private saving. Cato’s reform hub frames the problem clearly: promises exceed dedicated financing, and delay makes the eventual adjustment larger.

The book’s strongest point is that solvency and purpose are separate questions. Congress could close the gap through higher payroll taxes, benefit cuts, borrowing, heavier taxation of benefits, a higher retirement age, or some combination. None of those prescriptions answers what Social Security is for. If the goal is old-age poverty prevention, a flat benefit makes sense. If the goal is an earnings-related federal pension, higher taxes become harder to avoid.

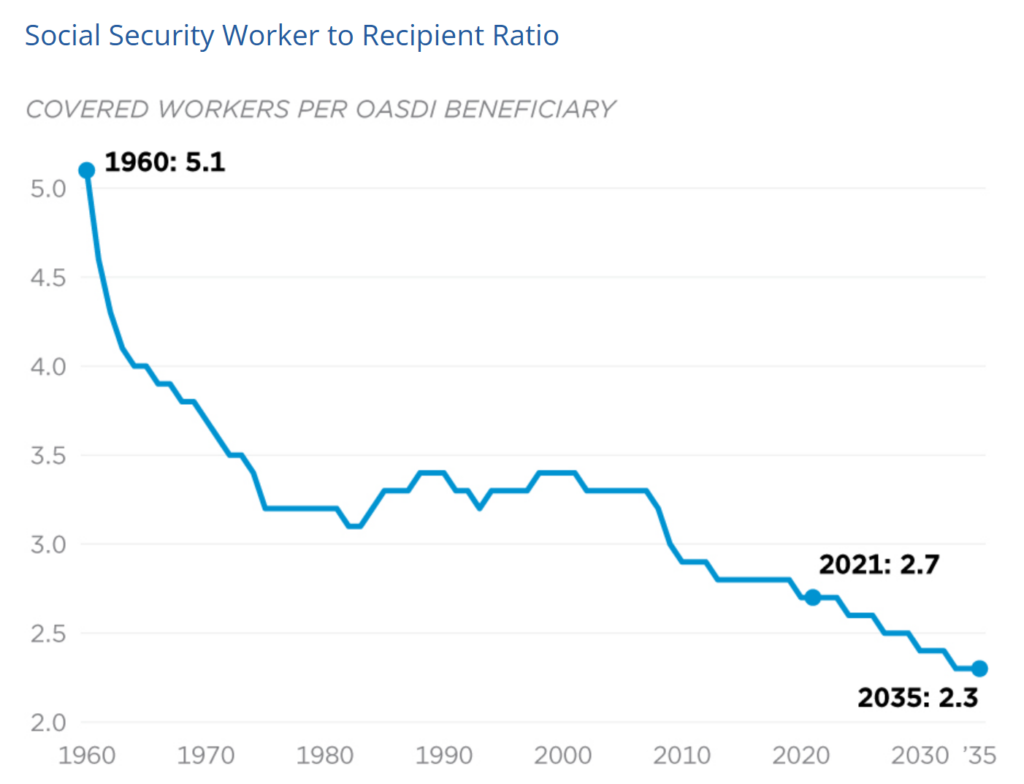

Recent work sharpens the case. Boccia and Krit Chanwong argue that the low fertility assumptions used by the Trustees report raise the long-term shortfall from roughly $33 trillion to $35 trillion or $36 trillion. The warning is clear: pay-as-you-go systems are hostage to demography.

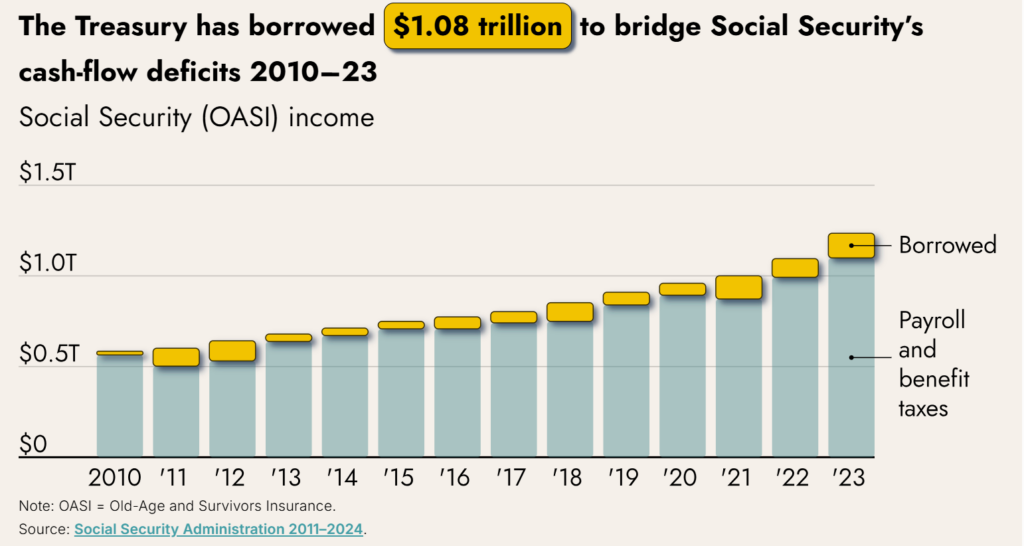

The trust-fund question receives similar care both in the book and on Cato’s visual feature on Social Security’s financial crisis, which rightly rejects the idea that the trust fund is a pile of saved payroll-tax contributions. Social Security is mostly pay-as-you-go. When costs exceed non-interest income, redeeming trust-fund securities requires Treasury financing. The bonds are legal obligations; the issue is who pays.

A flat benefit would bring Old-Age Insurance back to its original promise of “some measure of protection” against end-of-life poverty while making redistribution more explicit. Low earners would be protected. Middle- and high-income workers would rely more on private saving and receive less than scheduled benefits.

A higher retirement age has similar appeal and danger. Longer lifespans support later eligibility in the aggregate, but averages conceal workers with shorter life expectancy, manual jobs, disability risk, or weak late-career attachment. This is the greatest challenge for reformers.

Without a sustainable transition, political backlash can unravel any reform. The 2007 AIER Bulletin “What You Need to Know About Social Security” warned that current retirees and near-retirees have planned around specific benefits. Reducing them, especially for middle and high earners, will feel like a rug pull deserving of political punishment. Reformers should, therefore, keep cohort politics at the center of any proposal.

I hope the next phase of this project tackles cohort differentiation. Simply put, this involves separating citizens by age group and applying different changes to each cohort. Retirees and near-retirees could remain in the current system, while COLA adjustments, transitions to flat benefits, and switches to private savings accounts phased in for succeeding generations. Here I am a bit more hopeful than Boccia that Trump Accounts and Trump IRAs can help create the universal savings account off-ramps to Social Security’s crisis.

The book’s savings account proposal is attractive for younger workers, myself included, because it promises ownership, portability, and flexibility. Yet voluntary accounts may suffer from low take-up, while automatic enrollment moves toward compulsion. That tension is unavoidable. Retirement policy operates amid inertia, liquidity constraints, and imperfect foresight.

Reimagining Social Security asks whether Social Security should remain an expansive public pension promise or become a clear floor against old-age poverty. The latest Trustees Report makes that question urgent. Boccia and Nachkebia’s answer is a smaller, more candid system: protect seniors at the bottom, honor reliance interests among current retirees, and stop pretending payroll taxes can finance promises demographic change has already undermined.

As Social Security rapidly approaches the fiscal cliff, Reimagining serves as an important starting point for a national conversation about the program’s future — one that can no longer be deferred.